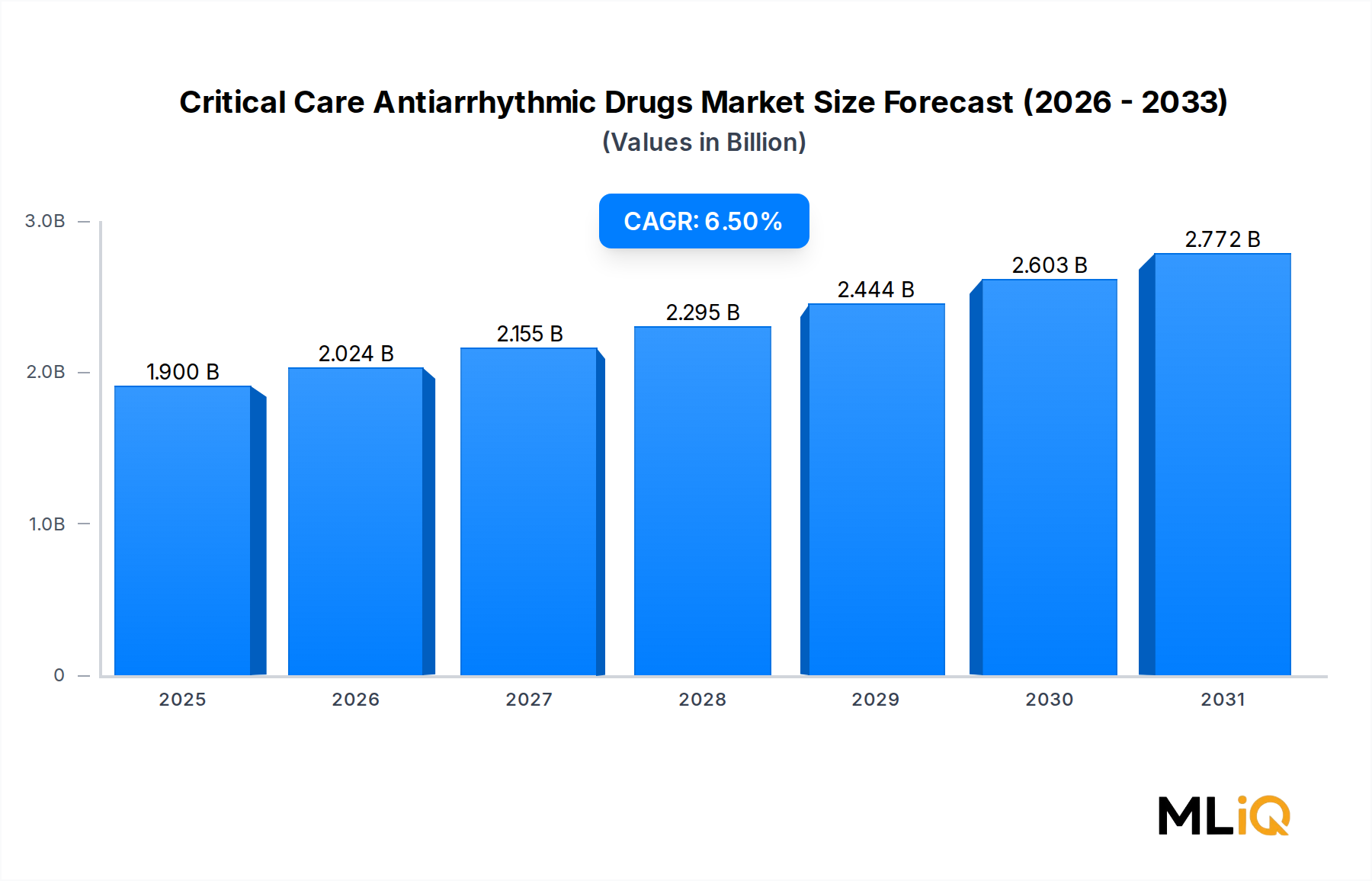

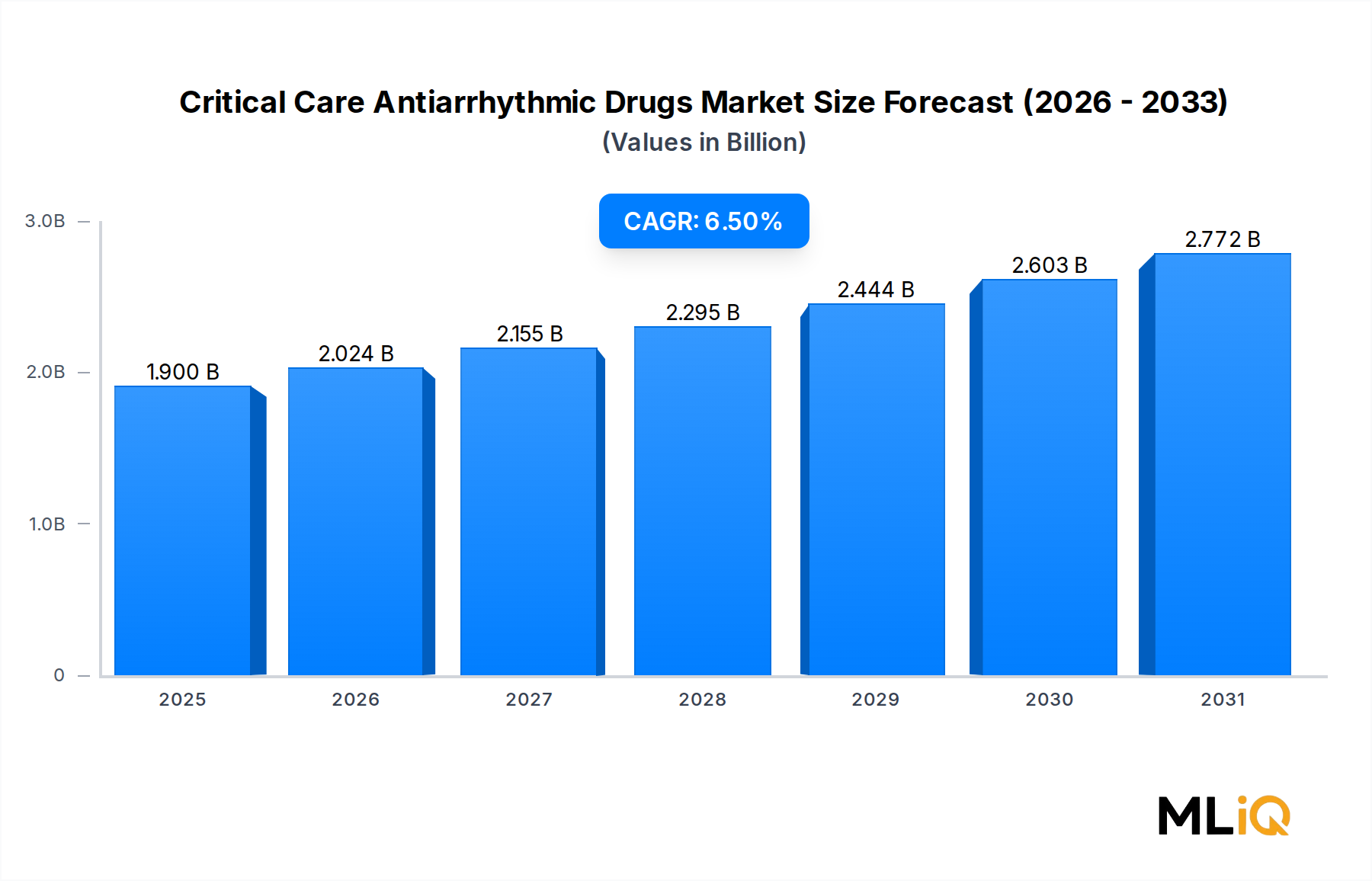

Hospital Segment Dominance in the Critical Care Antiarrhythmic Drugs Market

Hospitals represent the dominant application segment within the Critical Care Antiarrhythmic Drugs Market, commanding a disproportionately large revenue share relative to clinics, ambulatory centers, and other care settings. This dominance is structural, clinical, and logistical in nature, rooted in the concentration of high-acuity cardiac patients within hospital environments and the regulatory and safety requirements governing the administration of parenteral antiarrhythmic agents.

Critical care antiarrhythmic therapy — particularly intravenous formulations of amiodarone, lidocaine hydrochloride, procainamide, and adenosine — requires continuous hemodynamic monitoring, defibrillation readiness, and the expertise of trained intensivists, cardiologists, or emergency medicine physicians. These clinical prerequisites effectively confine the bulk of antiarrhythmic drug consumption to hospital ICUs, cardiac care units (CCUs), emergency departments, and surgical suites. The resource intensity of administration means that the shift toward outpatient settings, while occurring for chronic oral antiarrhythmic therapy, has not meaningfully eroded the hospital segment's dominance in the critical care subcategory.

Within hospitals, ICUs account for the single largest share of antiarrhythmic drug procurement. Post-operative atrial fibrillation (POAF) — affecting up to 30–50% of patients following cardiac surgery and 10–20% after thoracic or major non-cardiac procedures — is a primary driver of intravenous antiarrhythmic demand inside hospital settings. Sepsis-associated arrhythmias and arrhythmias arising from electrolyte imbalances in critically ill patients further amplify ICU-based consumption.

From a market structure perspective, hospitals purchase antiarrhythmic agents through a combination of group purchasing organizations (GPOs), direct manufacturer contracts, and hospital pharmacy procurement channels. The Hospital Pharmacy Market plays a pivotal gating role, as formulary committee decisions determine which agents receive institutional approval. Formulary inclusion is intensely competitive, with manufacturers offering volume-based rebates, clinical education programs, and nursing support tools to secure and maintain preferred formulary status.

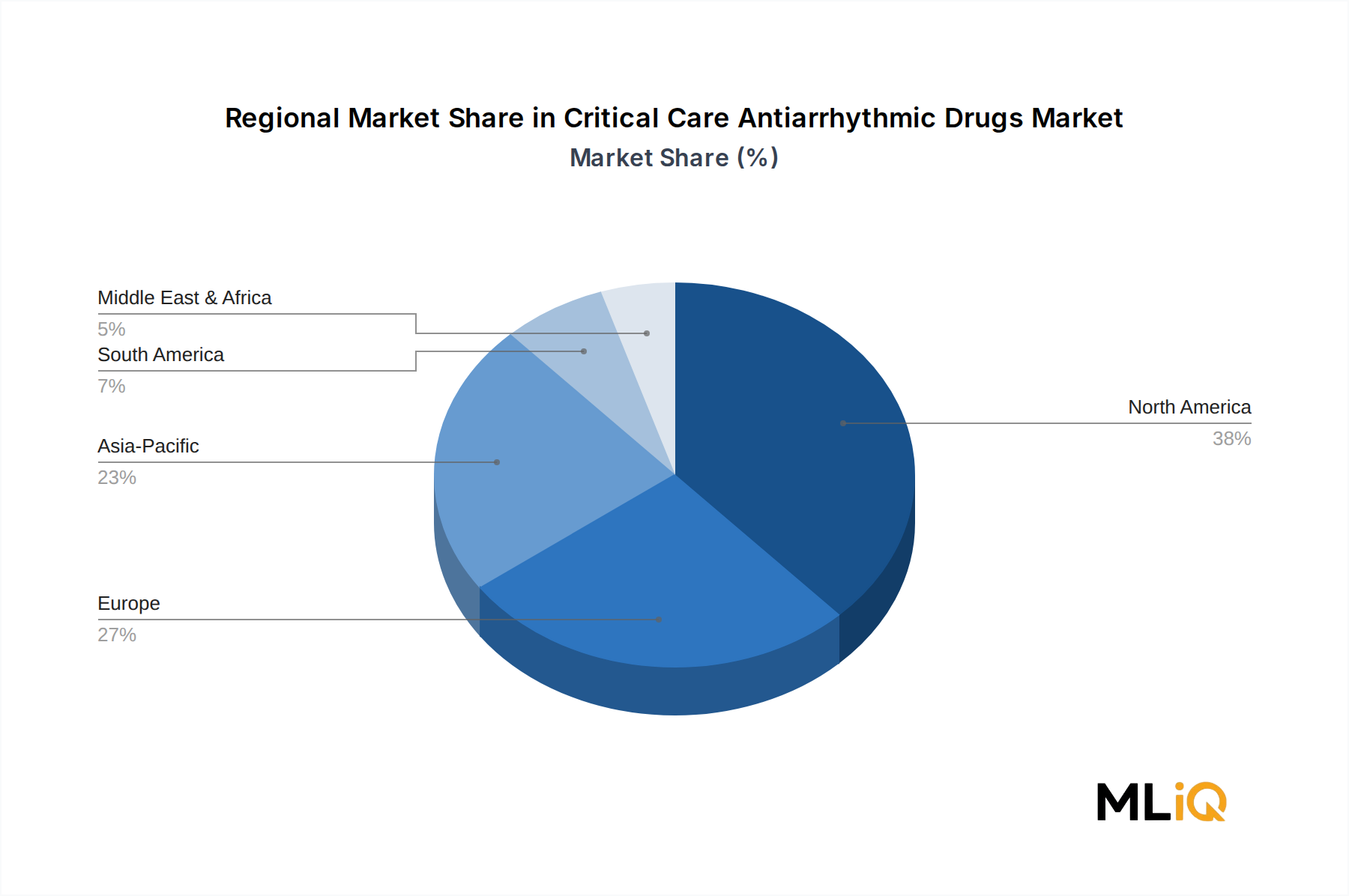

Key players maintaining significant hospital segment penetration include Pfizer Inc., Baxter International Inc., and Sanofi, each of which maintains established relationships with major hospital networks and GPOs across North America and Europe. Pfizer's Cordarone (amiodarone) franchise and Baxter's parenteral portfolio have historically anchored institutional purchasing decisions, while Sanofi leverages its broader hospital product suite to cross-sell within formulary negotiations.

The hospital segment's share is consolidating rather than growing proportionally, as ambulatory and clinic-based segments expand modestly with the increasing use of oral antiarrhythmic maintenance therapy following acute stabilization. However, the absolute dollar value flowing through the hospital channel continues to rise, driven by higher volumes, premium pricing for ready-to-use formulations, and increased procedural complexity. Specialty hospitals — particularly those with electrophysiology programs, cardiac transplant services, and advanced heart failure centers — represent high-value micro-segments within the broader hospital category, consuming disproportionately large quantities of advanced antiarrhythmic agents and newer investigational compounds under compassionate-use or early-access programs.

The integration of electronic health records (EHR) with pharmacy dispensing systems is also enhancing drug utilization tracking and reducing waste within hospital pharmacies, indirectly supporting cost-justification for higher-priced antiarrhythmic formulations by demonstrating outcome improvements.