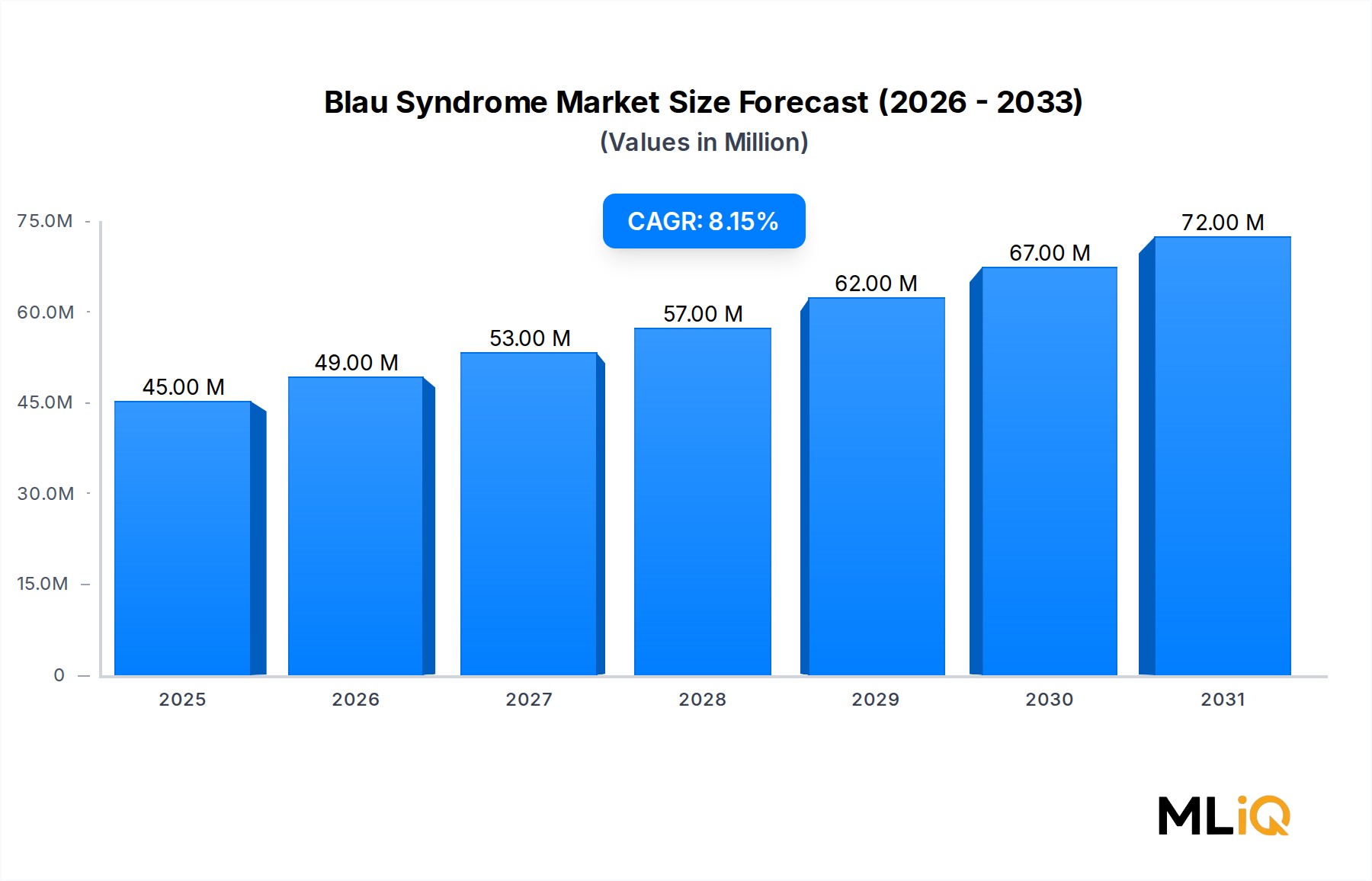

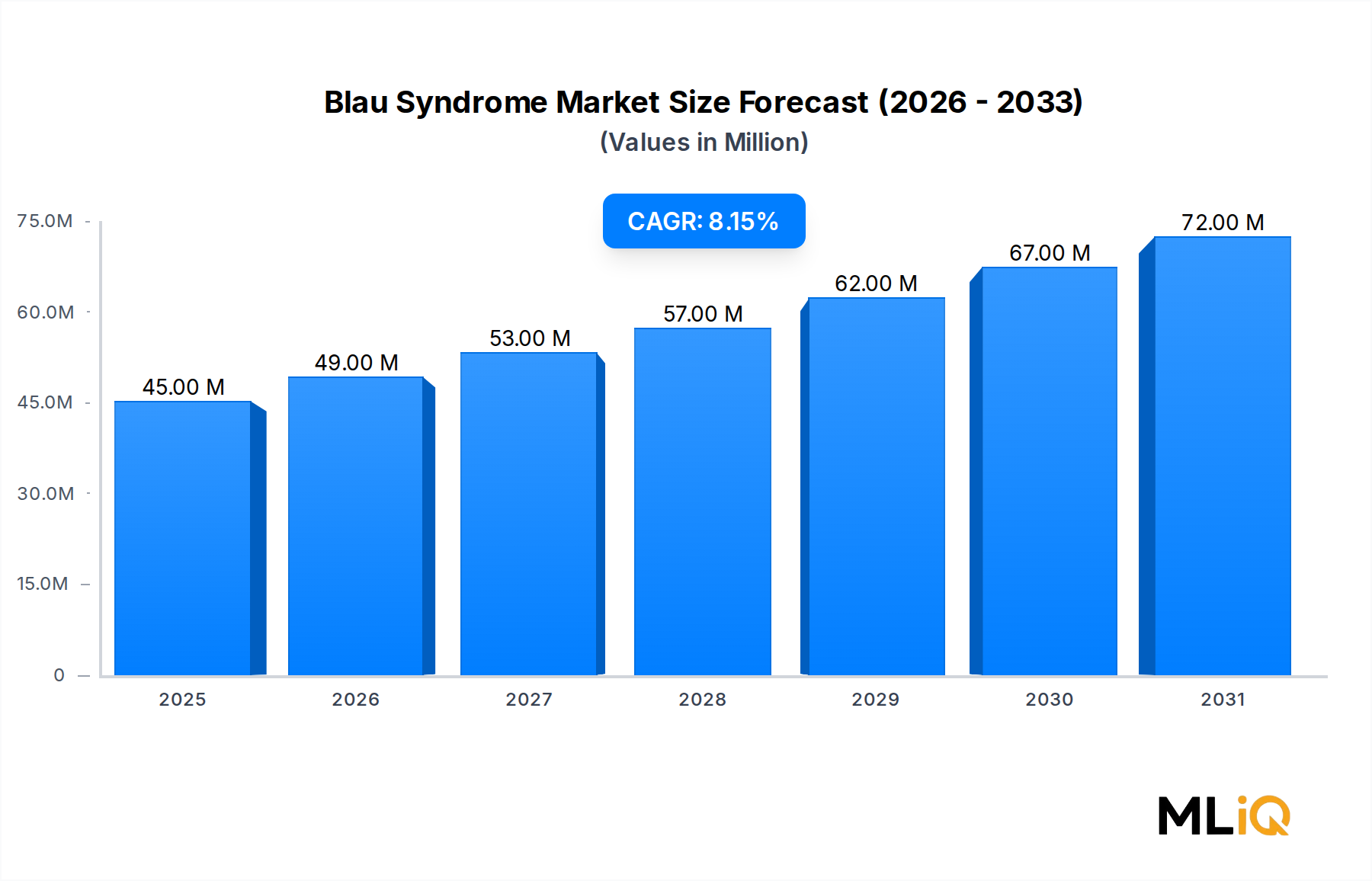

The Blau Syndrome Market is shaped by a clearly delineated set of growth drivers and structural restraints, each with quantifiable dimensions.

Driver: Rising Genetic Testing Adoption. The global Genetic Testing Market has expanded at a CAGR exceeding 12% in recent years, reflecting the broad deployment of next-generation sequencing panels in pediatric rheumatology and immunology departments. As NOD2 gene mutation testing becomes incorporated into standard diagnostic workups for juvenile-onset granulomatous diseases, the confirmed Blau syndrome patient pool is growing. This diagnostic expansion directly expands the addressable treatment market.

Driver: Orphan Drug Regulatory Incentives. In the United States, orphan drug designation provides 7 years of market exclusivity, 50% tax credits on clinical trial costs, and expedited review pathways. European Union orphan designation similarly confers 10 years of market exclusivity. These frameworks have incentivized at least four companies currently active in the Blau syndrome pipeline to accelerate IND filings and phase II trial initiation between 2022 and 2025.

Driver: Pediatric Rheumatology Specialization. The Pediatric Rheumatology Market is expanding globally, with a 15% increase in board-certified pediatric rheumatologists documented between 2018 and 2023 in North America alone. Increased specialist density correlates with higher diagnosis rates and more aggressive, protocol-driven treatment approaches, both favorable for market growth.

Constraint: Ultra-Rare Prevalence Ceiling. Blau syndrome has an estimated global prevalence of fewer than 1 in 1,000,000 individuals, constraining absolute patient volume and limiting commercial returns on therapy-specific clinical trials without substantial orphan incentives.

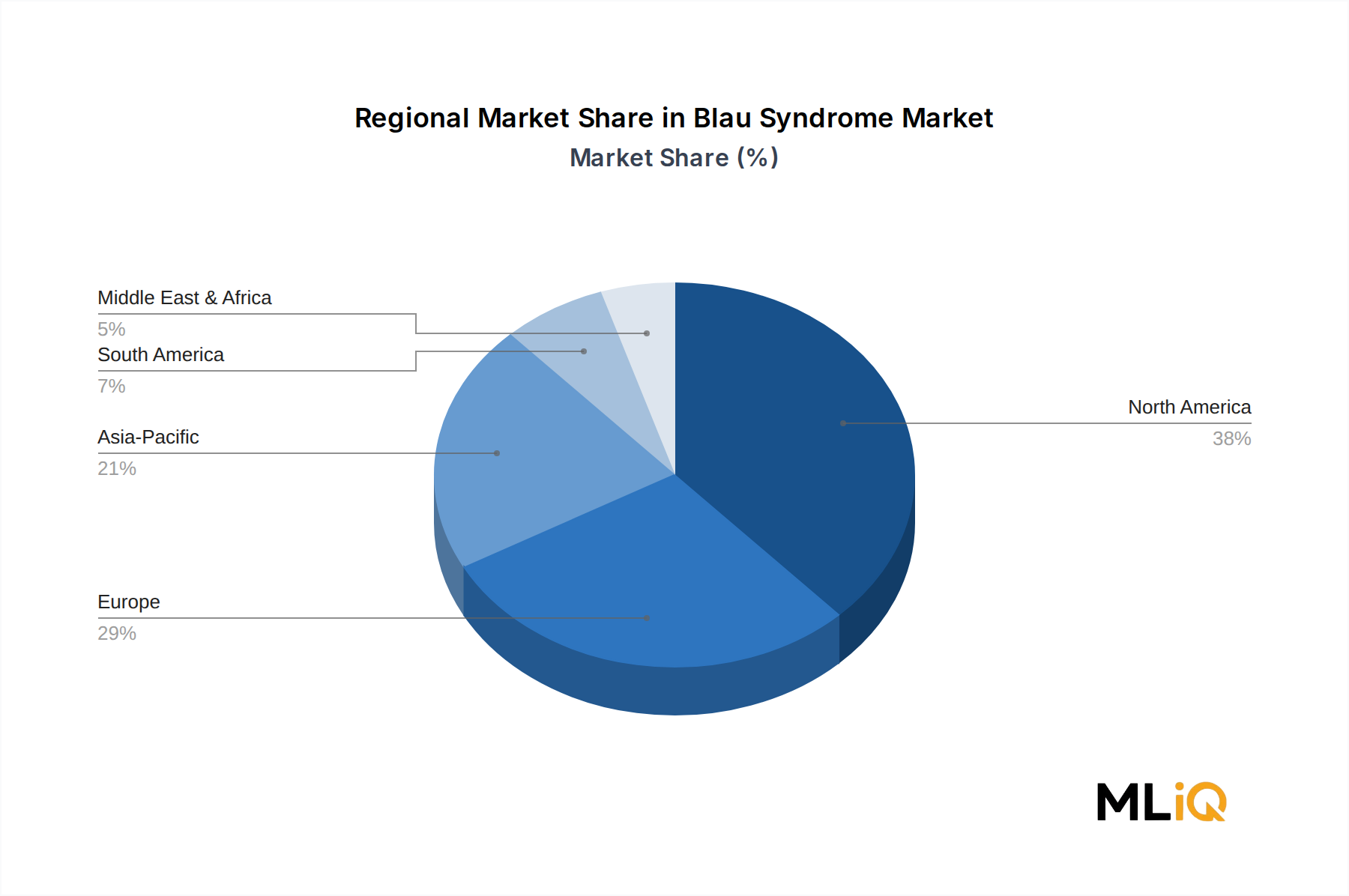

Constraint: Reimbursement Fragmentation. In many emerging markets, biologic agents used off-label for Blau syndrome receive inconsistent payer coverage, creating access barriers and compressing effective market size outside of North America and Western Europe.

Constraint: Diagnostic Latency. Average time from symptom onset to confirmed molecular diagnosis remains approximately 4–6 years in regions without integrated rare disease centers, delaying treatment initiation and patient enrollment in registry studies.