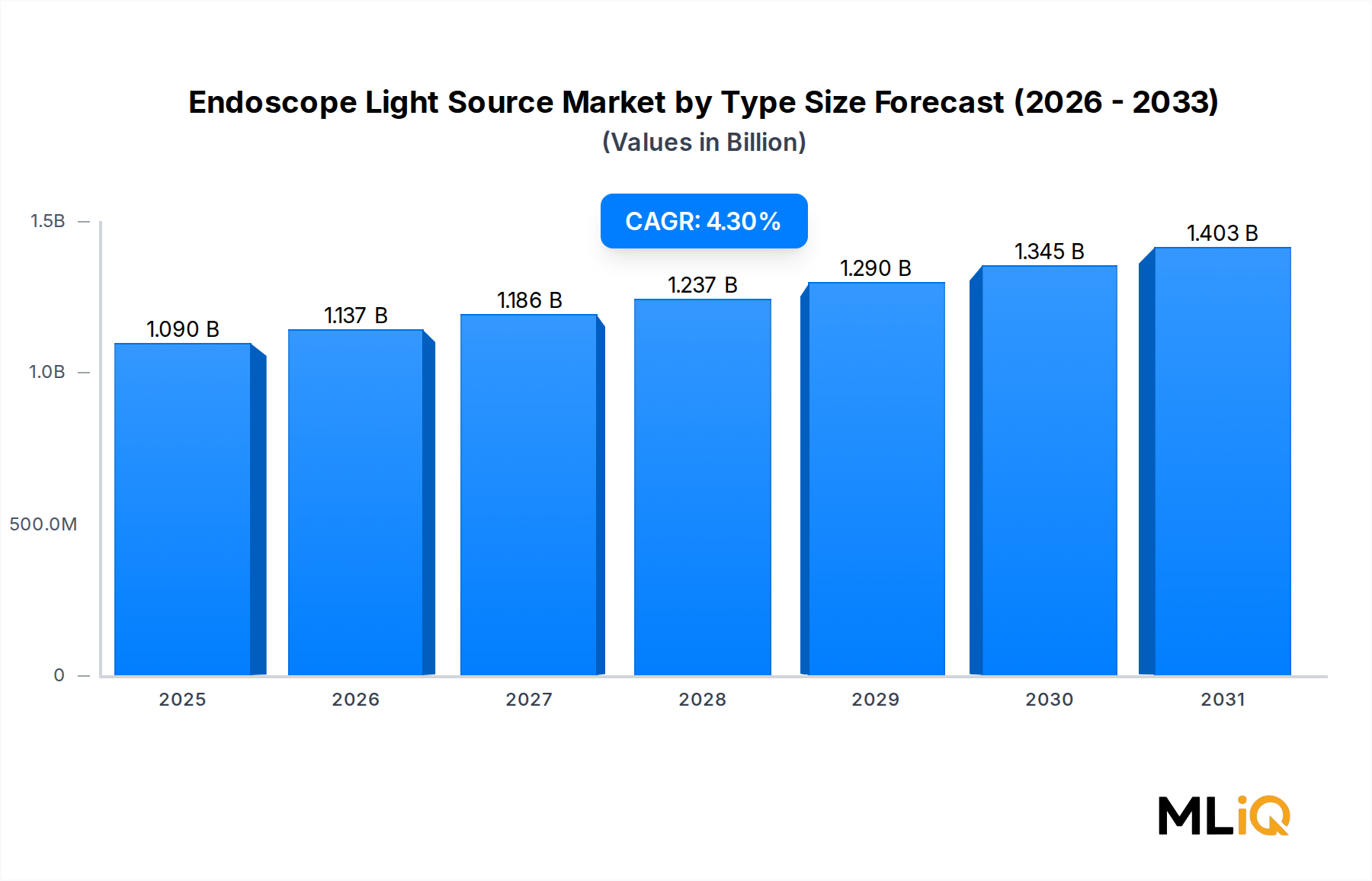

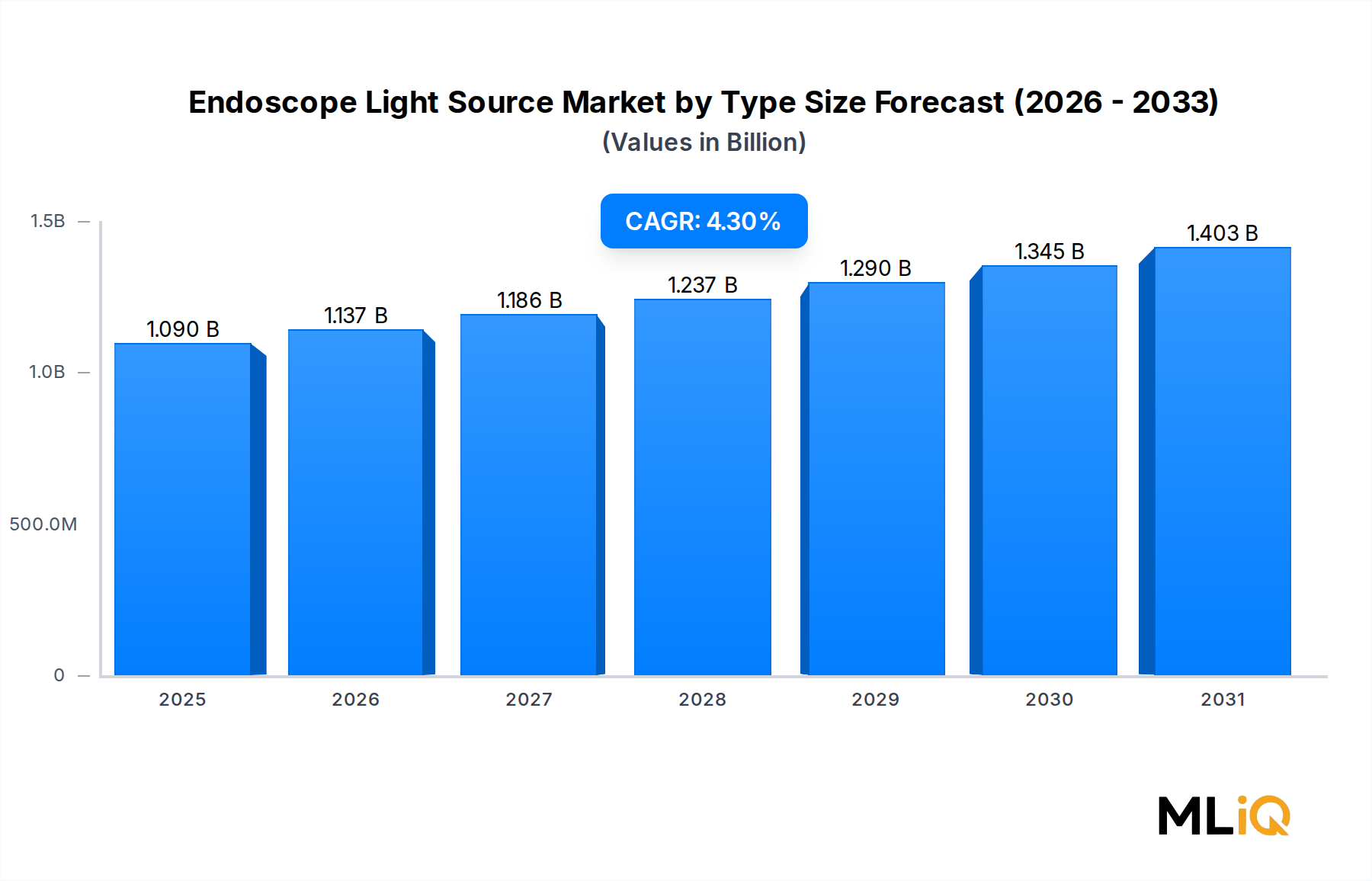

The global Endoscope Light Source Market by Type is valued at $1.09 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 4.3% over the forecast horizon. This steady upward trajectory reflects converging macro-level forces in healthcare infrastructure investment, an aging global population prone to gastrointestinal and respiratory disorders, and the accelerating transition from traditional xenon-based illumination to energy-efficient LED platforms.

The market is fundamentally driven by rising procedural volumes in diagnostic and therapeutic endoscopy worldwide. Gastrointestinal endoscopy alone accounts for the majority of endoscope utilization globally, as colorectal cancer screening mandates, gastric ulcer prevalence, and inflammatory bowel disease burden continue to mount. Respiratory endoscopy, another significant application, benefits from the growing incidence of chronic obstructive pulmonary disease (COPD) and lung cancer diagnostics that require bronchoscopic illumination solutions.

From a technology standpoint, LED light sources are displacing xenon systems as the dominant growth vector, owing to their superior energy efficiency, longer operational lifespans exceeding 20,000 hours, and reduced heat generation — all critical for both cost management and patient safety. This transition is analogous to broader shifts observed across the LED Surgical Lighting Market, where facilities are prioritizing total cost of ownership over upfront capital expenditure.

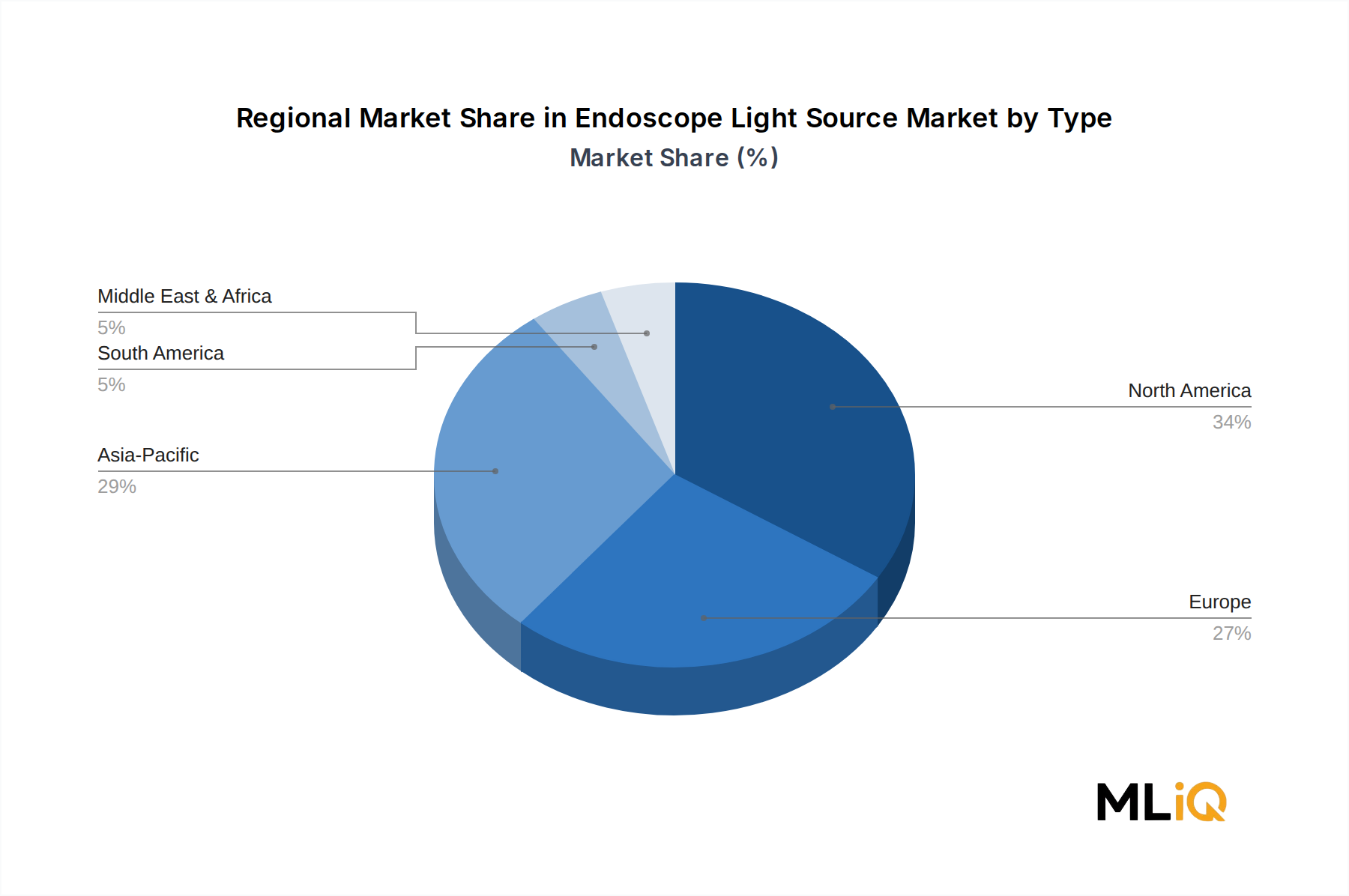

North America holds the largest revenue share, underpinned by well-established reimbursement frameworks, high procedural volumes, and early adoption of advanced endoscopic technologies. Asia Pacific is emerging as the fastest-growing region, fueled by expanding hospital infrastructure in China and India, rising medical tourism, and government-led health screening programs.

Key demand catalysts include the proliferation of outpatient endoscopy centers seeking compact, low-maintenance light source units, alongside the growing preference for single-use and hybrid endoscopy systems that integrate purpose-built illumination modules. Competitive intensity remains elevated, with established players such as Olympus Corporation, Karl Storz, and Stryker investing aggressively in product differentiation through smart connectivity features and modular system designs.

Forward-looking, the market is expected to benefit from regulatory tailwinds in the European Union and the United States that incentivize adoption of energy-efficient medical devices, alongside the post-pandemic rebound in elective procedure scheduling. The integration of artificial intelligence-assisted imaging, which demands superior and consistent illumination quality, further reinforces the long-term demand outlook for high-performance endoscope light sources across all type segments.