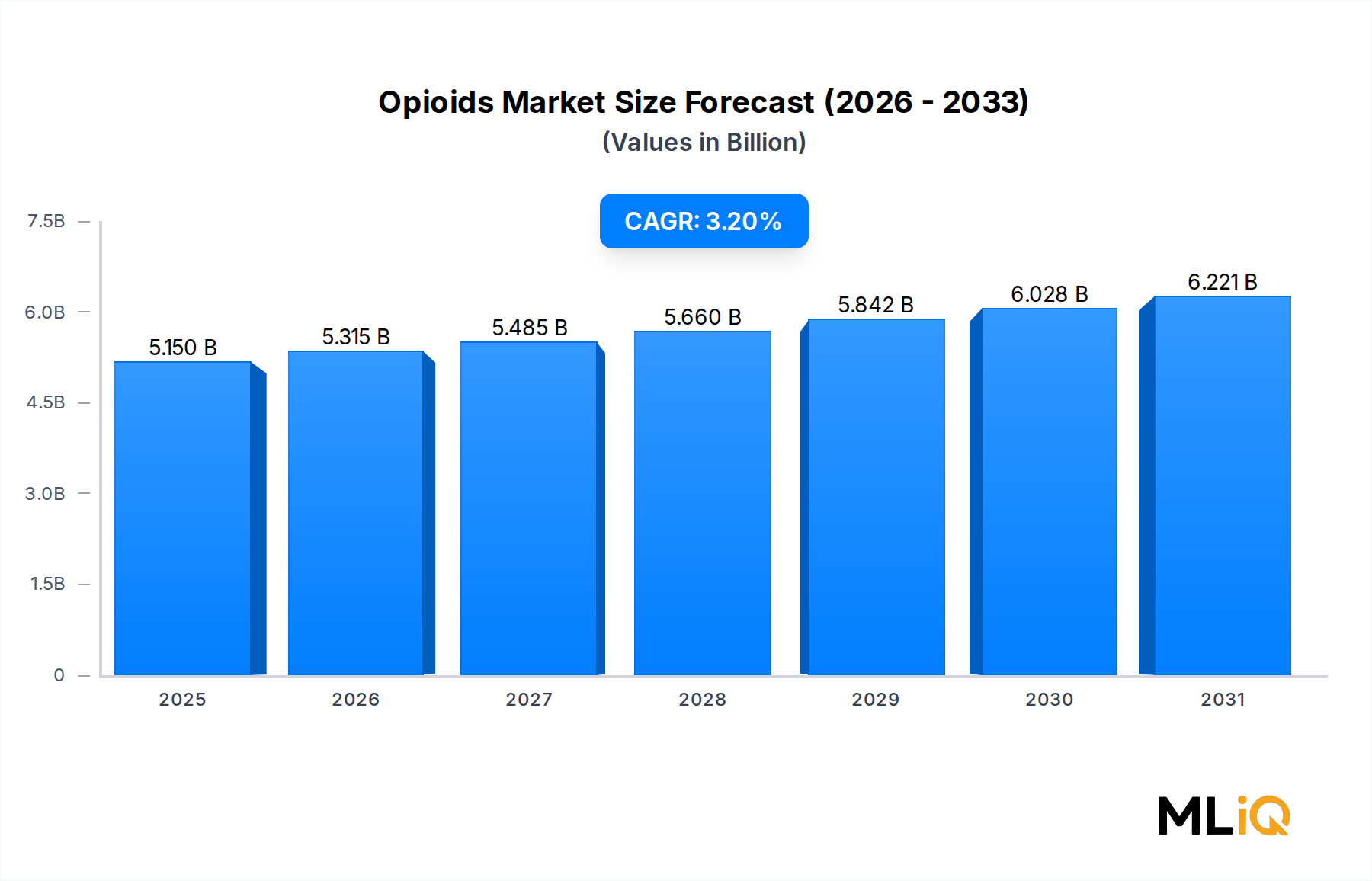

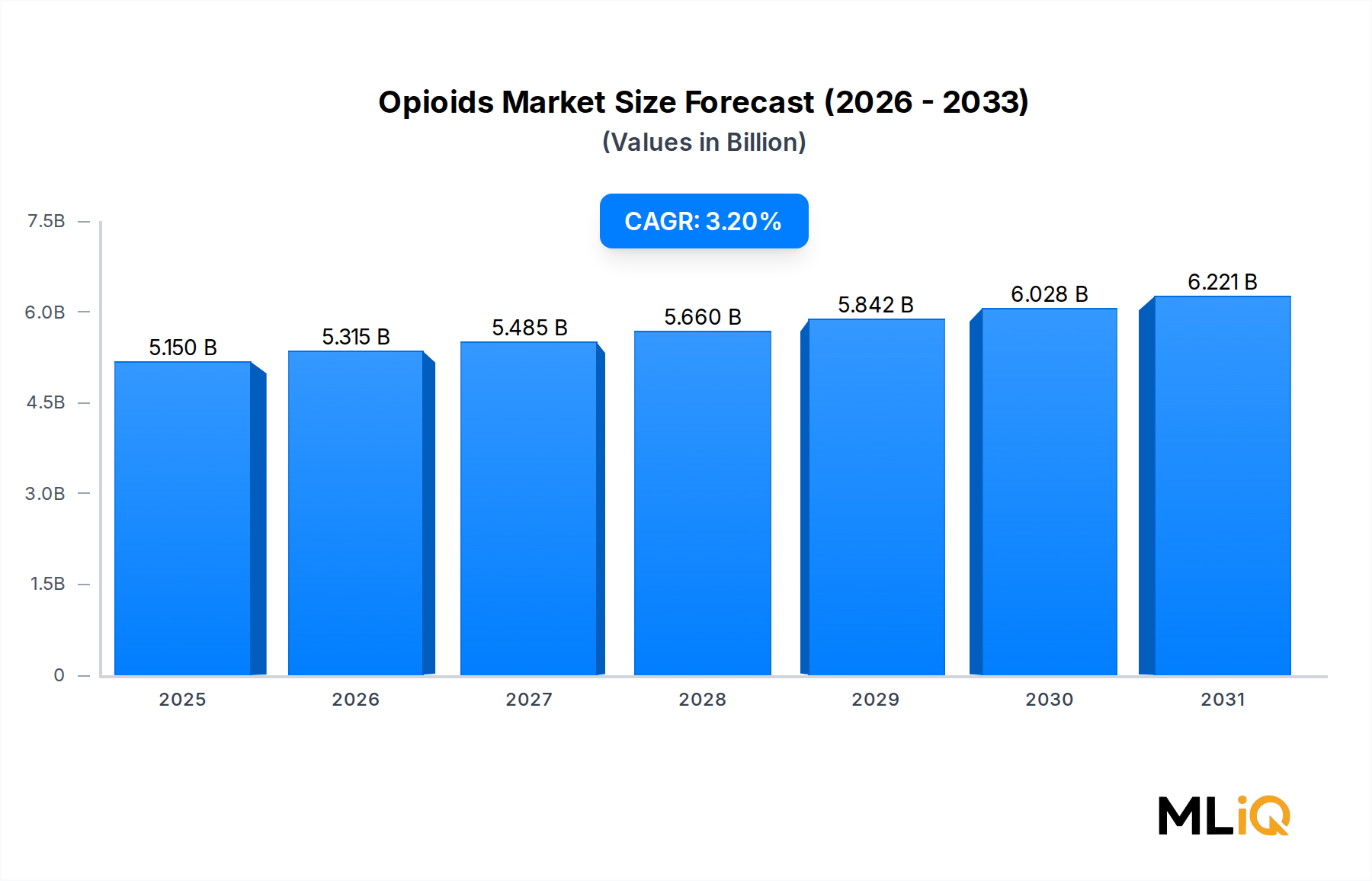

The Opioids Market is shaped by a set of quantifiable drivers and material constraints that together define its 3.2% CAGR trajectory.

Driver 1 — Aging Population and Chronic Disease Burden: Globally, the population aged 65 and older is projected to reach 1.6 billion by 2050, up from approximately 771 million in 2022 (UN World Population Prospects). Older adults exhibit higher prevalence of musculoskeletal disorders, neuropathic conditions, and oncological disease — all pain states with significant opioid prescribing overlap. This demographic expansion directly sustains baseline demand.

Driver 2 — Rising Cancer Incidence: The International Agency for Research on Cancer (IARC) reported 20 million new cancer cases in 2022, with the figure projected to climb to 35 million by 2050. Given that 55–95% of advanced cancer patients experience moderate-to-severe pain requiring opioid analgesics, oncology remains a volume-stable indication irrespective of broader prescribing restrictions.

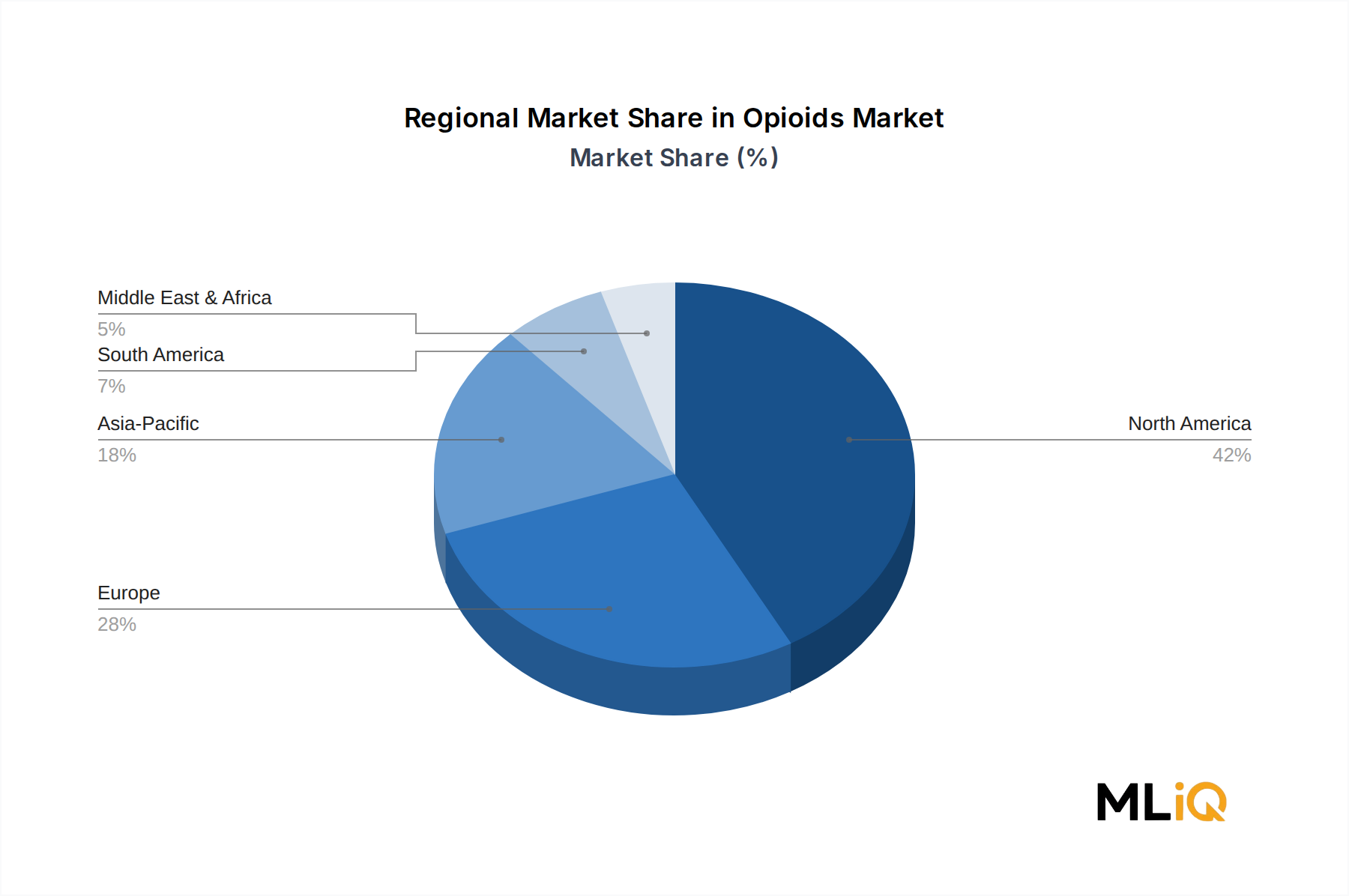

Driver 3 — Expanding Surgical Volumes in Emerging Markets: Healthcare infrastructure investment across Asia Pacific, Southeast Asia, and Sub-Saharan Africa is driving surgical volume growth at rates exceeding 6% annually in some markets, expanding the perioperative opioid consumption base. This growth partially offsets volume declines in mature North American and European markets.

Constraint 1 — Regulatory and Litigation Overhang: The opioid epidemic in North America has generated unprecedented legal and regulatory pressure. Purdue Pharma LP's $6 billion settlement and Johnson & Johnson's $5 billion multi-state resolution have reshaped industry risk calculus, increasing compliance costs and depressing commercial aggressiveness in new market development.

Constraint 2 — Generic Price Compression: The expiration of key branded opioid patents has accelerated generic penetration, compressing average selling prices and reducing revenue per unit. Teva Pharmaceutical Industries Limited and Sun Pharmaceuticals benefit from this dynamic as low-cost producers, but it constrains total market value growth.

Constraint 3 — Prescribing Restriction Mandates: Updated CDC guidelines (2022) recommending opioid dose tapering for chronic non-cancer pain, combined with state-level prescribing caps, have measurably reduced opioid prescription volumes in the United States. Dispensed opioid prescriptions declined by approximately 44% between 2012 and 2022, constraining the North American market's contribution to global revenue growth.