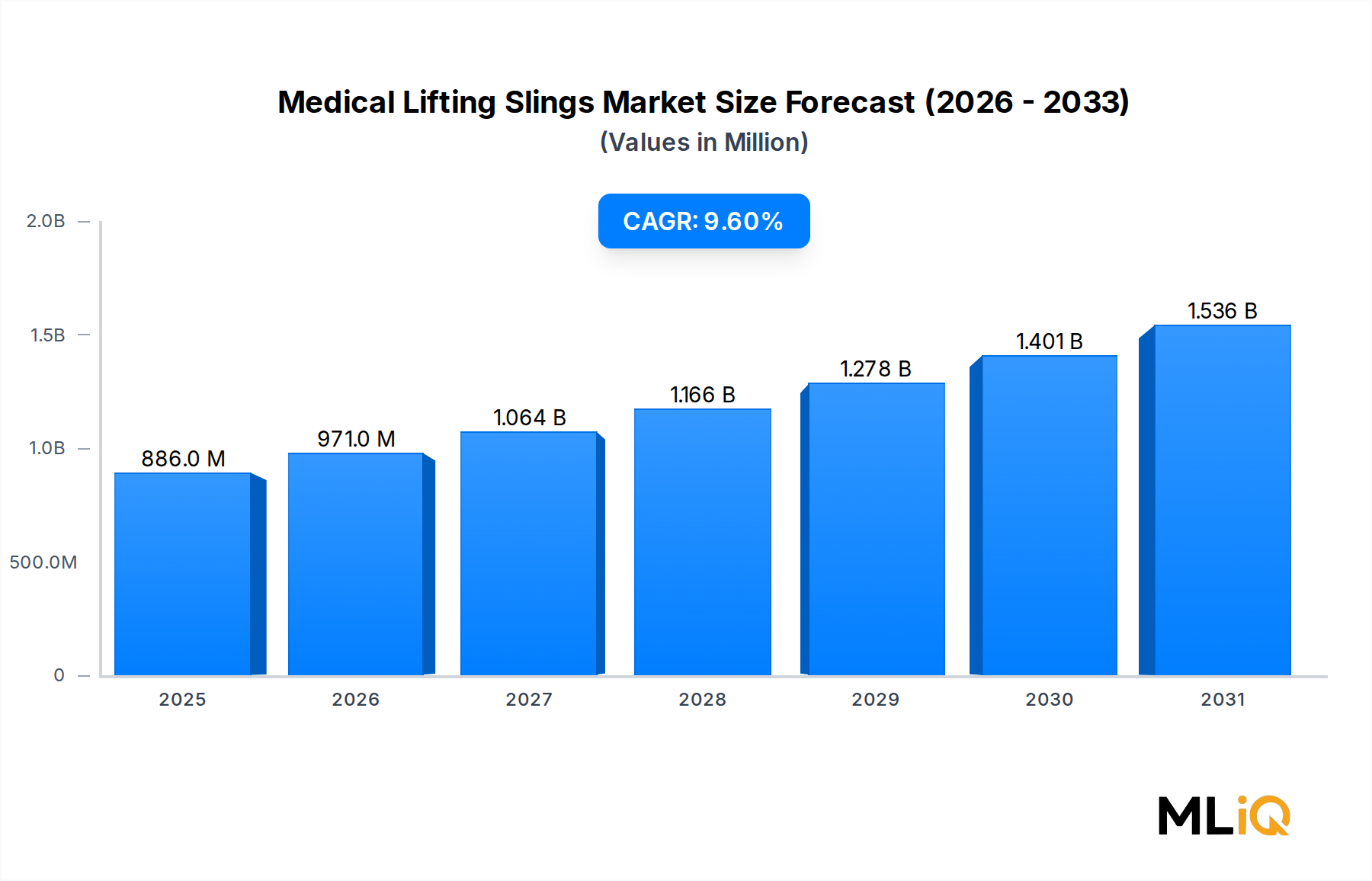

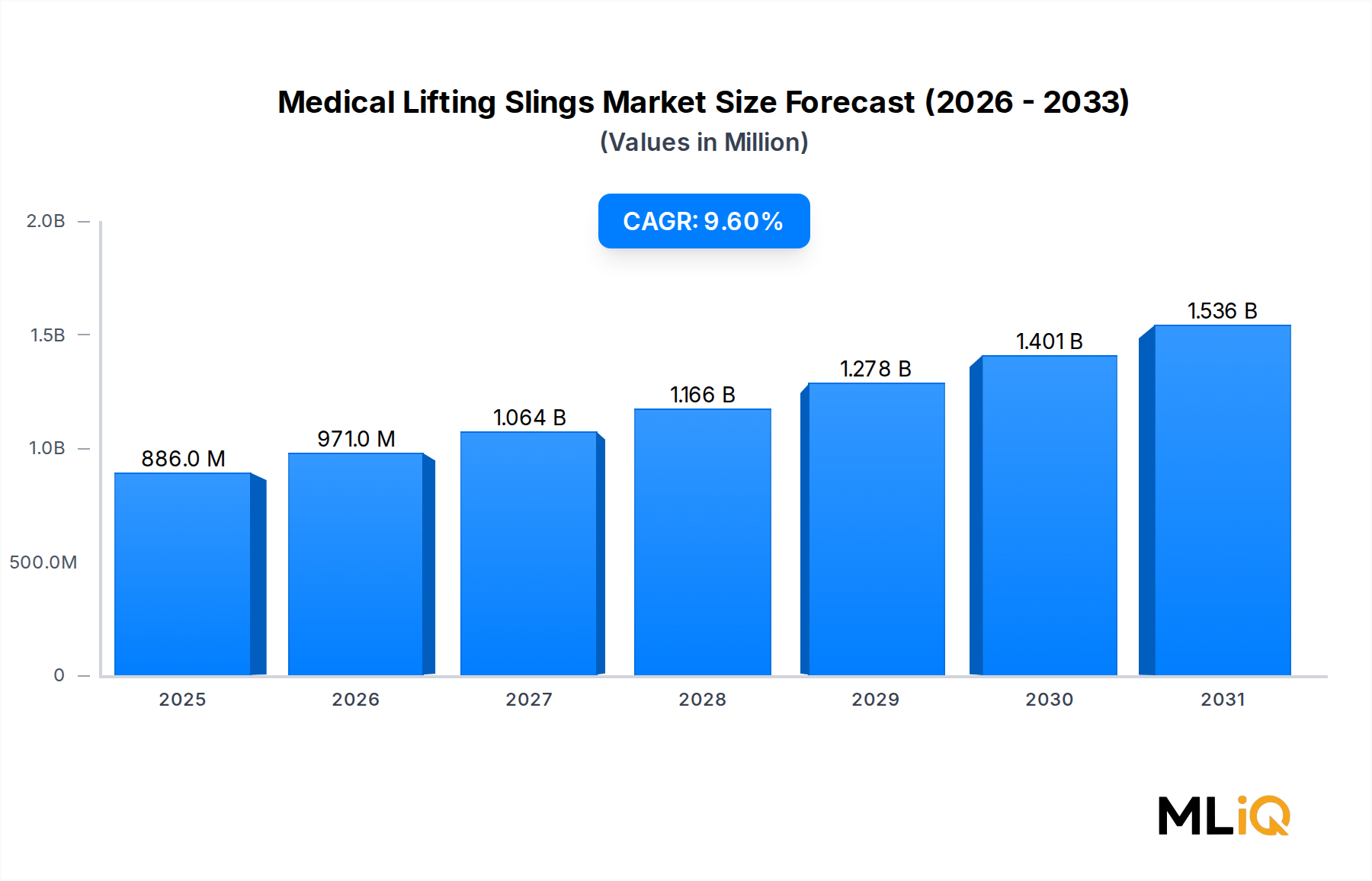

The Medical Lifting Slings Market operates within a complex cross-border trade architecture shaped by concentration of manufacturing capability, regulatory market access requirements, and evolving tariff regimes.

Leading exporting nations include China, which has emerged as the dominant volume manufacturer of mid-range and value-tier slings leveraging cost-efficient textile production infrastructure concentrated in Guangdong and Zhejiang provinces. European nations — particularly the United Kingdom, Sweden, Denmark, and Germany — serve as premium-segment exporters, with brand equity, clinical certification, and MDR compliance as competitive moats. The United States exports limited volumes but is a net importer of sling products, primarily sourcing from China and Southeast Asian manufacturers for value-tier distribution.

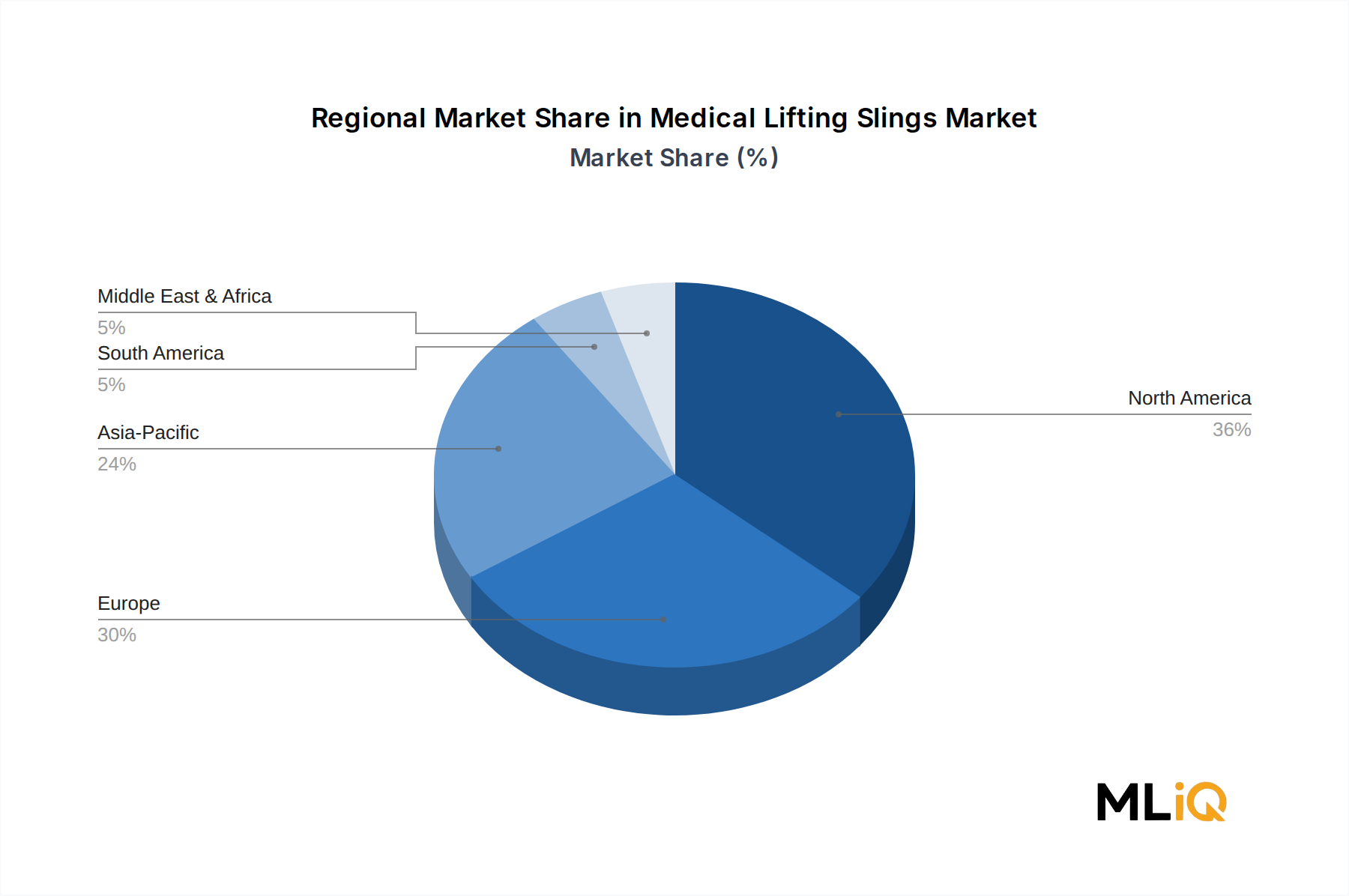

Key importing regions include North America, which relies heavily on Chinese and Southeast Asian supply chains for mid-market and disposable sling categories, and Middle East & Africa, which sources primarily from European and Indian manufacturers for institutional procurement under tender agreements.

Tariff dynamics have introduced material supply chain complexity. The United States Section 301 tariff regime imposed on Chinese medical textile imports — with effective rates ranging from 7.5% to 25% depending on product classification — has elevated landed costs for importers reliant on Chinese manufacturing, incentivizing supply chain diversification toward Vietnam, Bangladesh, and India. This shift aligns with broader trends observed in the Technical Textiles Market and the Disposable Medical Textiles Market, where nearshoring and friendshoring strategies are reshaping sourcing geography.

Non-tariff barriers, including MDR certification requirements in the EU, FDA 510(k) clearance pathways in the U.S., and Therapeutic Goods Administration registration in Australia, create regulatory moats that limit rapid market entry by low-cost manufacturers lacking clinical documentation infrastructure. These requirements disproportionately benefit established European and North American brands in institutional procurement tenders.

Post-Brexit trade adjustments between the UK and EU have introduced