The Digital Radiology Market is propelled by a set of quantifiable and structural drivers while facing specific constraints that modulate growth velocity across geographies and segments.

On the driver side, the global prevalence of chronic diseases constitutes the most significant demand catalyst. According to the World Health Organization, cardiovascular diseases account for approximately 17.9 million deaths annually, necessitating continuous imaging support for diagnosis and treatment guidance. Cancer incidence, projected to reach 35 million new cases globally by 2050 per IARC estimates, further amplifies procedural imaging volumes across chest, mammography, and orthopedic applications.

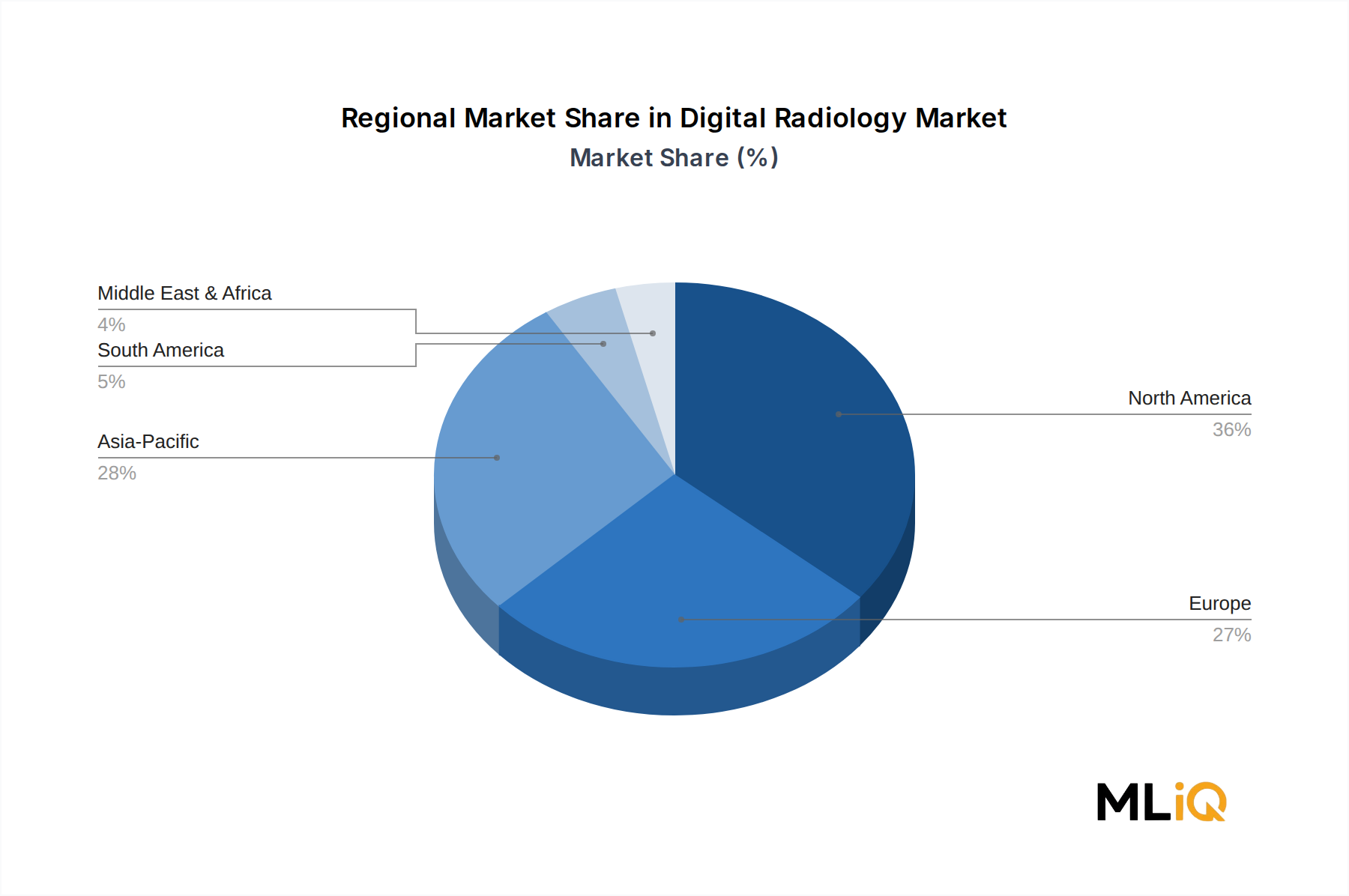

The rapid expansion of healthcare infrastructure in Asia Pacific markets is another quantifiable driver. China and India collectively account for over 2.8 billion people, with healthcare spending per capita growing at double-digit rates in several provincial and state-level health programs. Government initiatives such as China's Healthy China 2030 plan and India's Ayushman Bharat scheme are channeling capital into diagnostic equipment procurement for public hospitals, generating structured demand for digital radiology systems.

Technological advancement, particularly the integration of AI-assisted diagnostic algorithms with digital radiology platforms, is accelerating upgrade cycles among existing hospital users. Facilities that deployed first-generation digital radiology systems between 2010 and 2016 are entering refresh cycles, creating a substantial installed-base replacement opportunity estimated to represent a meaningful portion of annual unit shipments through 2028.

Constraints include the high upfront capital cost of stationary digital radiology systems, which can range between $150,000 and $1,000,000 per unit depending on configuration, creating procurement barriers in lower-income healthcare markets and smaller diagnostic clinics. Reimbursement rate compression in mature markets such as the United States and Western Europe also exerts margin pressure on end users, indirectly constraining system upgrade frequency.

Regulatory complexity represents an additional constraint. The divergence in medical device approval timelines across the FDA, CE, and regional regulatory frameworks introduces market entry delays for new product launches, particularly for AI-integrated radiology platforms that require software as a medical device classification under evolving regulatory guidance.

Cybersecurity vulnerabilities associated with networked digital radiology systems have also emerged as a procurement concern, particularly following high-profile ransomware incidents targeting hospital imaging infrastructure, which has begun to influence procurement criteria and delay purchasing decisions pending security validation.