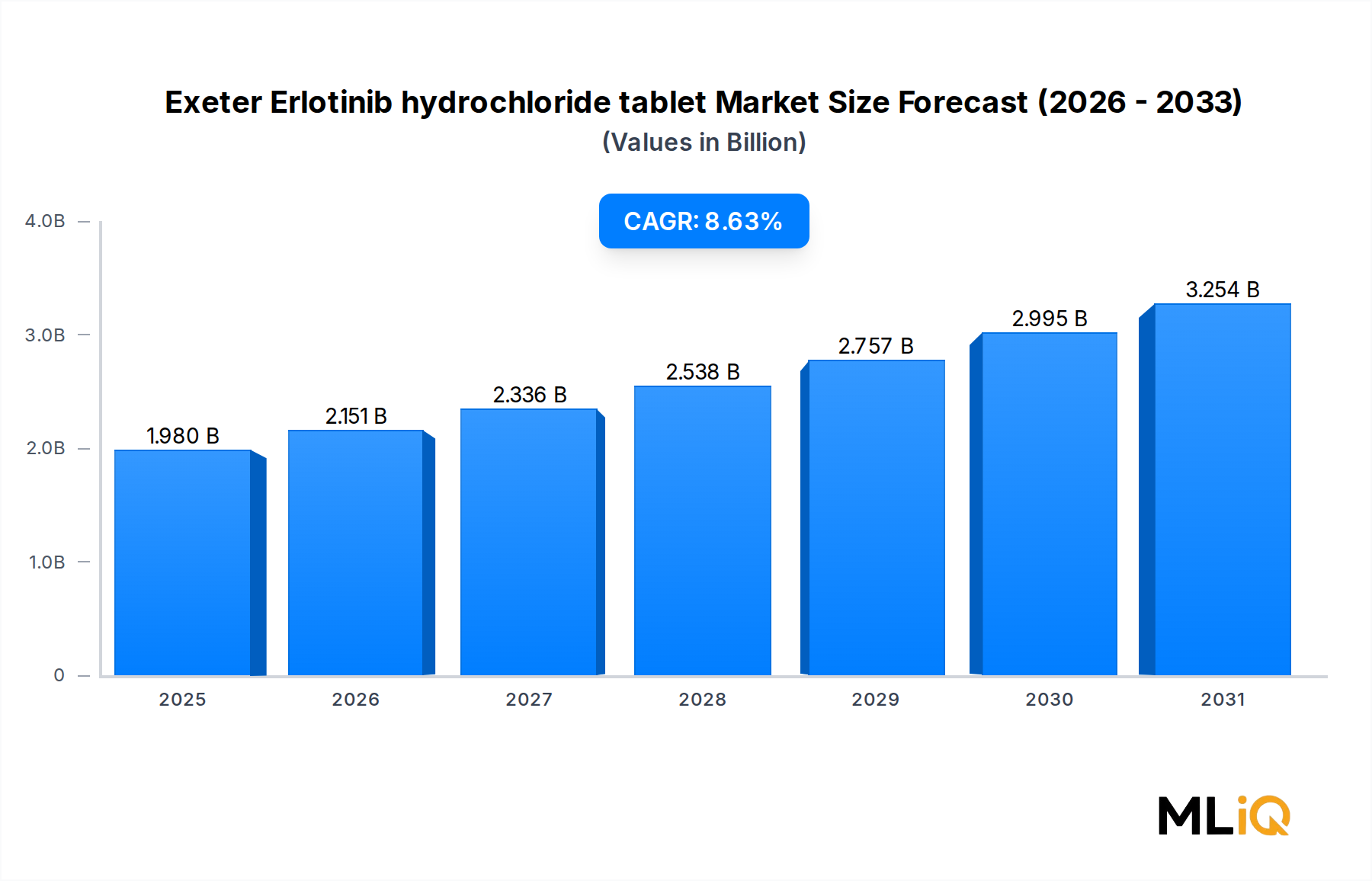

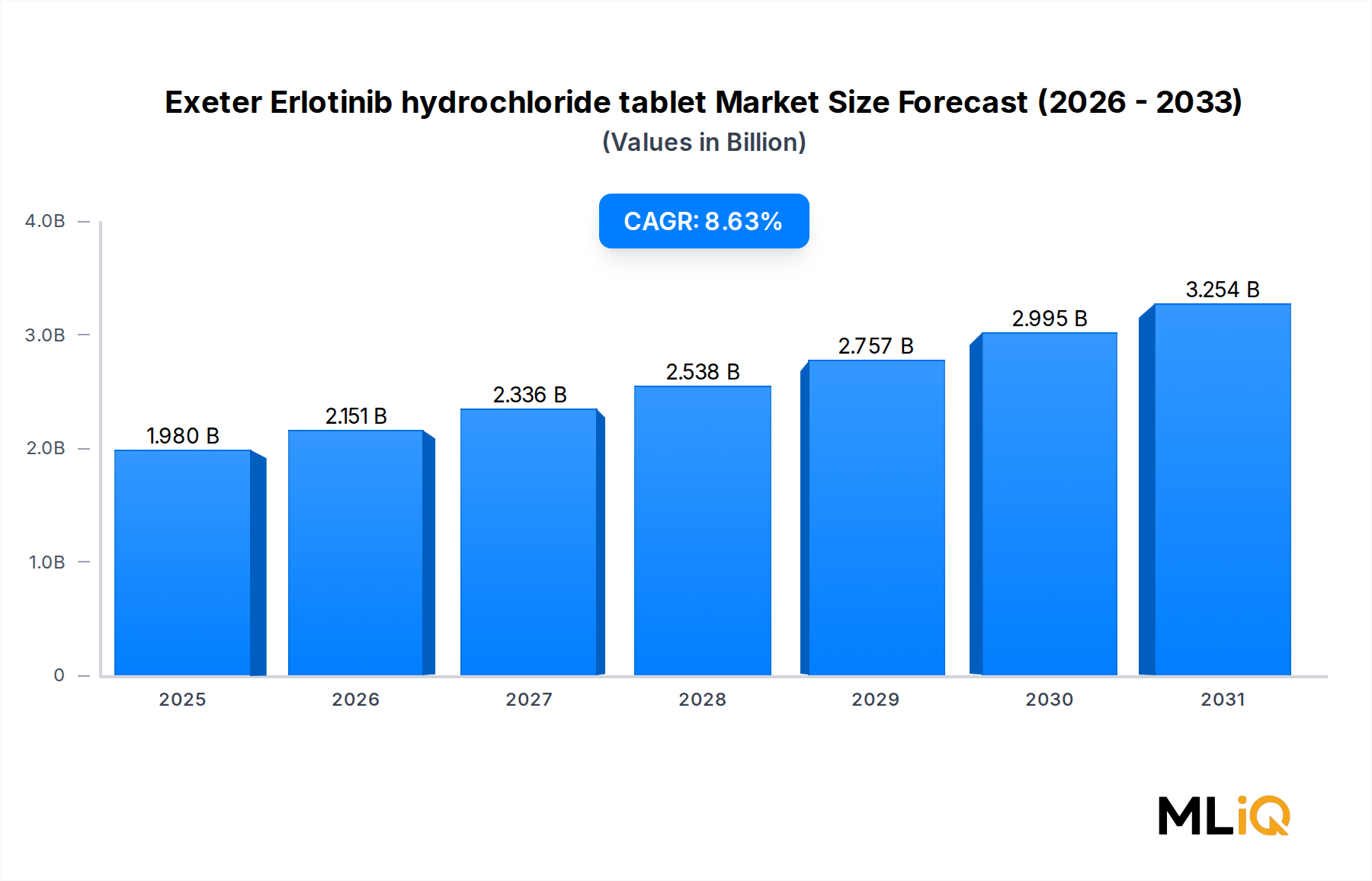

Several structural drivers underpin the 8.63% CAGR projected for the Exeter Erlotinib hydrochloride tablet Market through 2033, while a set of meaningful constraints tempers the pace of expansion.

Driver 1 — Rising Global Cancer Incidence: The International Agency for Research on Cancer (IARC) projects global cancer incidence to reach 28.4 million cases annually by 2040, up from approximately 19.3 million in 2020. Lung cancer and pancreatic cancer, the two core indications for erlotinib, are among the fastest-growing in incidence in low- and middle-income countries, directly expanding the addressable patient base for erlotinib hydrochloride tablets.

Driver 2 — Patent Expiration and Generic Entry: The expiration of core erlotinib patents across major jurisdictions has catalyzed entry by over 15 generic manufacturers globally. This has expanded volume throughput substantially, with generic penetration in price-sensitive markets such as India and Brazil exceeding 80% of total erlotinib prescriptions by value. The Oral Oncology Drug Market has been a direct beneficiary of this generic democratization trend.

Driver 3 — Expanding EGFR Diagnostic Testing: EGFR mutation testing rates in newly diagnosed NSCLC patients have grown from approximately 40% globally in 2018 to over 65% in 2024, driven by guideline mandates and declining test costs. Higher testing rates translate directly into increased eligible prescription volumes.

Constraint 1 — Third-Generation EGFR Inhibitor Competition: Osimertinib (Tagrisso, AstraZeneca) has captured significant first-line NSCLC market share in high-income markets, reducing erlotinib's addressable patient pool in the United States and Western Europe. In markets where osimertinib is reimbursed at parity, erlotinib faces structural volume displacement.

Constraint 2 — Pricing Erosion in Generic Markets: Intense generic competition has compressed average selling prices by 25–35% over the 2019–2024 period in markets including India, China, and Eastern Europe. While this drives volume growth, it limits revenue growth in absolute terms for manufacturers without scale advantages.

Constraint 3 — Regulatory and Quality Compliance Costs: Increasingly stringent GMP requirements from the FDA, EMA, and other regulators impose significant compliance costs, particularly on smaller generic manufacturers, potentially limiting market participation and creating consolidation pressure.