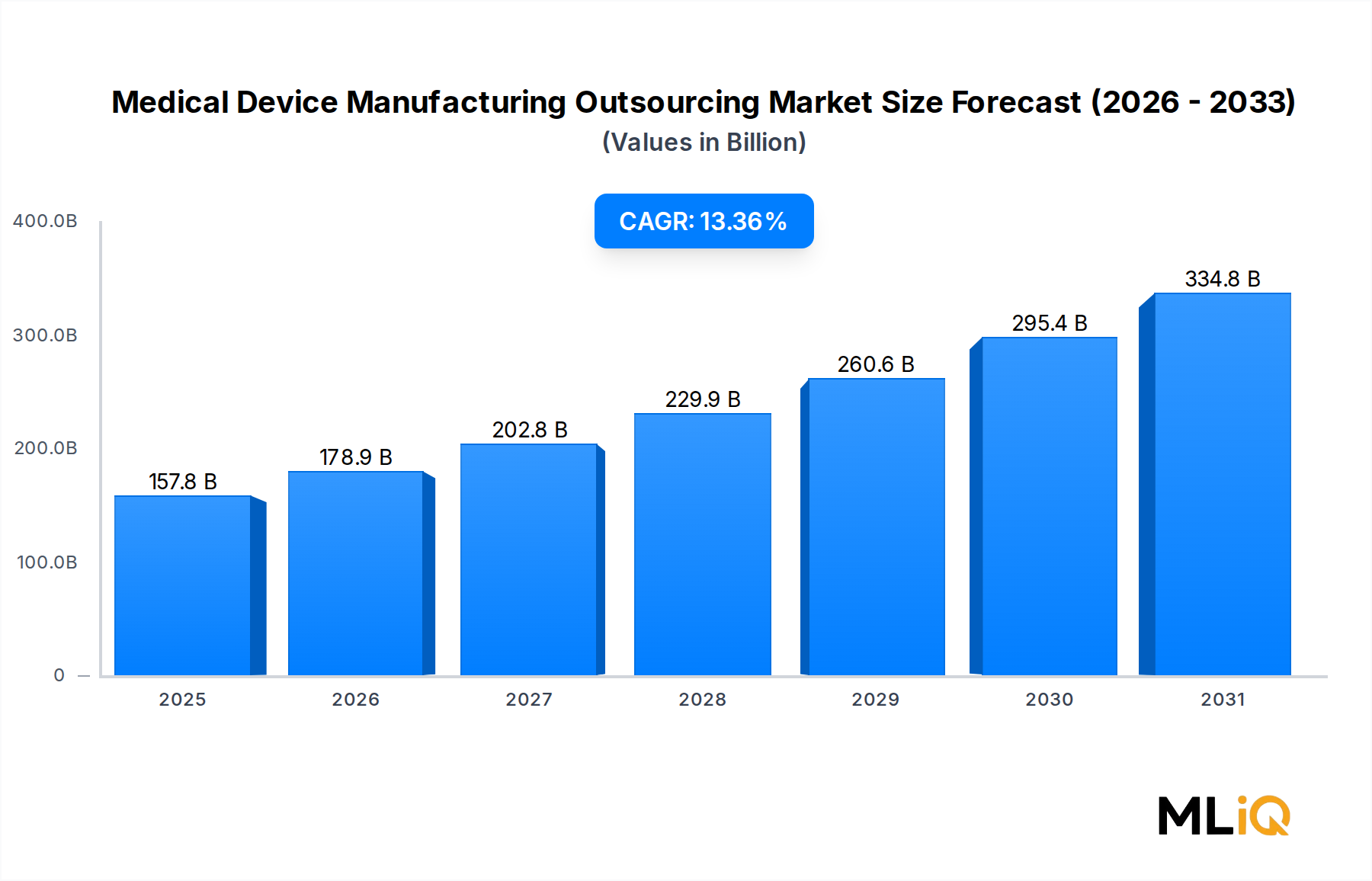

The global Medical Device Manufacturing Outsourcing Market is valued at $157.79 billion in 2025 and is projected to expand at a compound annual growth rate of 13.36% through 2033, positioning it among the fastest-growing outsourcing segments within the broader life sciences industry. This robust trajectory is underpinned by a convergence of structural cost pressures, accelerating technological complexity, regulatory tightening, and evolving global supply chain architectures.

Original equipment manufacturers (OEMs) across the medical technology value chain are increasingly offloading non-core manufacturing functions to contract partners capable of delivering economies of scale, specialized engineering expertise, and regulatory compliance infrastructure. The shift from captive manufacturing toward outsourced models is no longer a cost-optimization tactic alone — it has become a strategic imperative for companies competing in markets defined by compressed product development cycles and tightening reimbursement environments.

Several macro-level forces are amplifying this transition. Aging demographics across North America, Europe, and Asia Pacific are driving chronic disease prevalence, fueling demand for orthopedic, cardiovascular, and diagnostic devices at rates that internal manufacturing networks are ill-equipped to absorb. Simultaneously, the proliferation of connected, software-enabled medical devices is increasing engineering complexity, making vertical integration prohibitively expensive for mid-tier OEMs.

On the regulatory front, the implementation of the EU Medical Device Regulation (MDR) and In Vitro Diagnostic Regulation (IVDR), alongside the U.S. FDA's Quality Management System Regulation (QMSR) — which aligns 21 CFR Part 820 with ISO 13485:2016 — has introduced significant compliance costs. Contract manufacturers that maintain pre-certified quality systems offer OEMs a materially faster and less capital-intensive path to market authorization.

The forward-looking outlook through 2033 is characterized by increasing service sophistication among contract manufacturers. Leading contract partners are evolving from pure-play production providers to integrated solution providers offering end-to-end capabilities spanning product design, regulatory consulting, supply chain management, and post-market surveillance. This service expansion is expected to elevate average contract values and increase customer retention rates across the ecosystem.

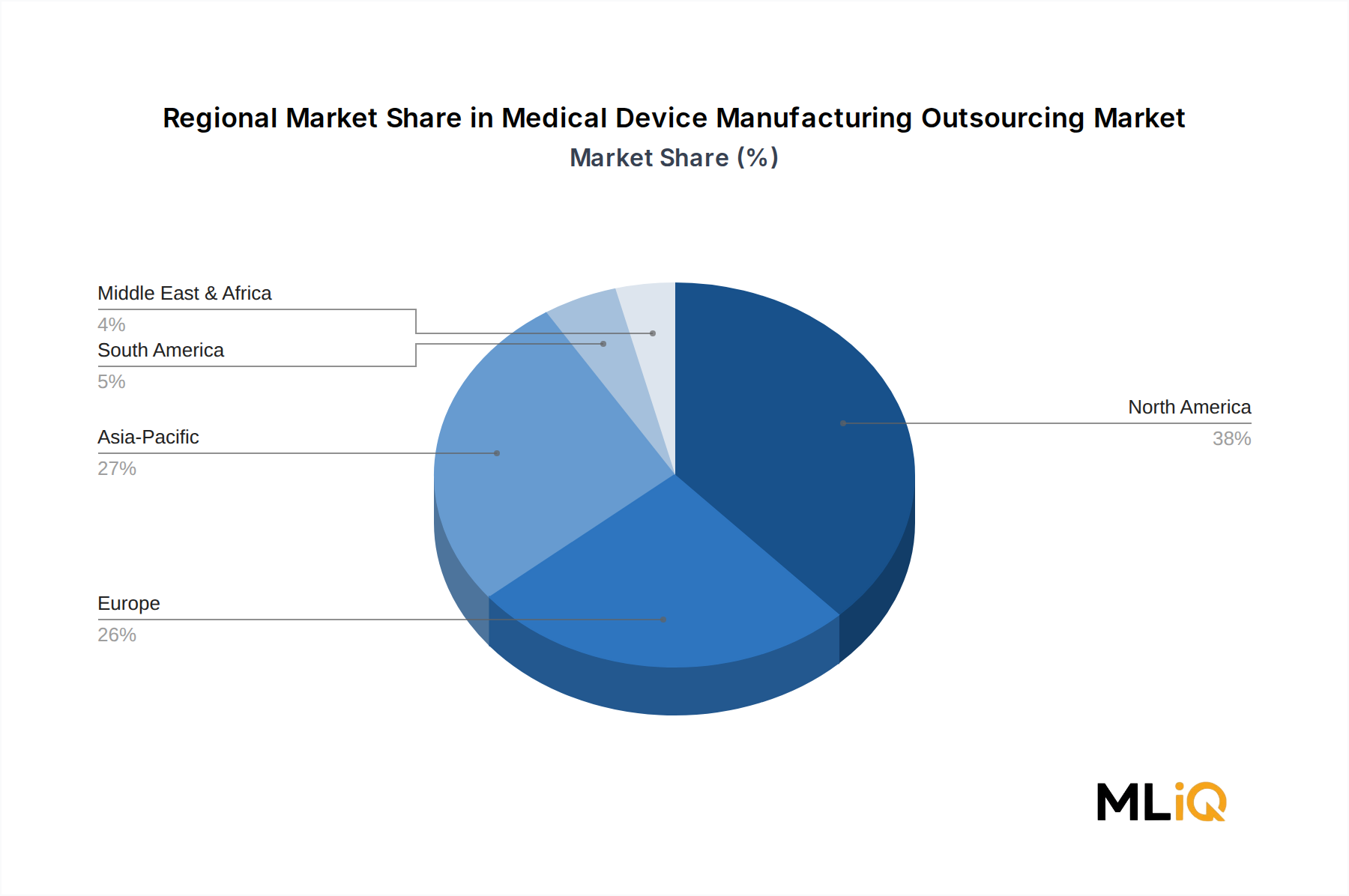

Geographically, North America retains the largest absolute revenue share, while Asia Pacific — particularly China, India, and South Korea — is emerging as the fastest-growing production hub, driven by cost arbitrage, government manufacturing incentives, and improving quality certifications among local contract manufacturers. The Latin American market, anchored by Brazil, is demonstrating above-average growth rates as domestic OEMs seek regional contract partners to navigate complex local regulatory frameworks.

Investor sentiment remains constructive, with private equity and strategic acquirers deploying capital into platform contract manufacturers capable of cross-modal device production. The sector's resilience to macroeconomic cyclicality — given the non-discretionary nature of healthcare spending — further supports premium valuation multiples for high-quality outsourcing assets.