Credit Card Dominance and Segment Leadership in the Personal Bank Card Market

Within the Personal Bank Card Market, the credit card sub-segment commands the largest share of total revenue, a position it has maintained across multiple economic cycles due to its superior monetization mechanics relative to other card types. Credit cards generate revenue through interchange fees, annual fees, interest income on revolving balances, penalty fees, and increasingly, through data monetization partnerships with merchants and analytics platforms. This multi-layered revenue architecture makes credit cards disproportionately profitable for issuing banks and card networks compared to debit or prepaid alternatives.

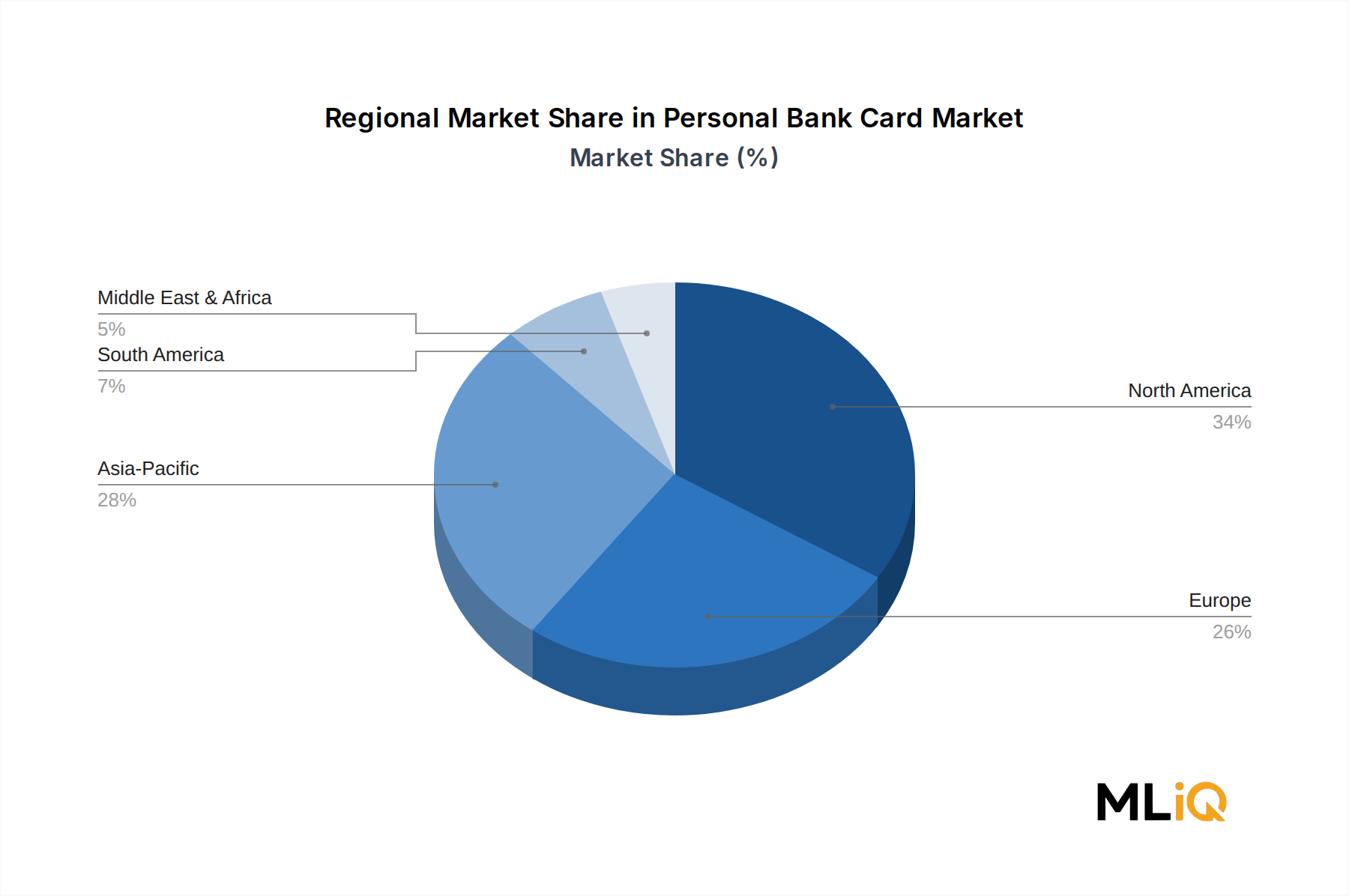

The dominance of credit cards is further reinforced by deeply entrenched consumer behavior in mature markets. In North America, for instance, credit card penetration among banked adults exceeds 70%, and total outstanding revolving credit associated with card products represents a significant share of household balance sheets. The rewards economy — encompassing cashback, airline miles, hotel points, and purchase protections — functions as a powerful switching cost mechanism, creating high cardholder retention rates for premium issuers such as American Express, JPMorgan Chase & Co, and Capital One.

The Credit Card Market itself is undergoing meaningful product stratification. Issuers are increasingly segmenting their portfolios into mass-market cards (targeting transactors and thin-file borrowers), premium travel cards (targeting high-income frequent flyers), and small business cards (targeting self-employed and micro-enterprise segments). This segmentation allows issuers to optimize risk-adjusted returns while expanding total addressable issuance volume.

Within the application breakdown of the Personal Bank Card Market, commercial banks constitute the single largest distribution channel, leveraging their existing deposit and loan customer relationships to cross-sell card products at scale. Private banks serve ultra-high-net-worth cardholders with bespoke metal card offerings featuring elevated credit limits and concierge services, while central banks increasingly mandate interoperable card standards that benefit all issuers operating in their jurisdictions.

Key players driving credit card segment leadership include Citigroup Inc., which operates one of the most geographically diversified credit card portfolios globally, spanning Asia Pacific, Latin America, and the United States; MasterCard, which functions as the network backbone for millions of credit card issuances worldwide; and Bank of America Corporation, which has leveraged its Preferred Rewards program to significantly reduce revolving credit attrition.

In terms of share trajectory, the credit card segment's dominance is consolidating rather than expanding, as the Debit Card Market and Prepaid Card Market are growing at faster rates in Asia Pacific and sub-Saharan Africa where first-time card users are entering the financial system via bank account-linked debit instruments. Nevertheless, in absolute revenue terms, credit cards will remain the market's highest-value segment through 2033 due to their superior per-card economics and the ongoing shift of consumer spending toward experiential categories — travel, dining, entertainment — that are disproportionately financed through credit rather than debit instruments.

Digital-native credit card issuers such as Synchrony and neobank-affiliated card programs are challenging traditional issuers by deploying instant card issuance, AI-driven credit limit management, and embedded card controls that appeal to younger, digitally fluent consumer segments. These competitive dynamics are compelling legacy issuers to accelerate technology investment cycles, further embedding credit card infrastructure within broader digital banking platforms.