Smartphone and Wearable Device Dominance in the Contactless Payment Market

Within the Contactless Payment Market, the smartphones and wearables segment occupies the most strategically significant position by revenue share and growth velocity. This dominance is not incidental — it is the product of decades of ecosystem investment by platform incumbents, the mass commoditization of NFC chipsets, and the deep behavioral entrenchment of mobile-first commerce among younger demographic cohorts globally.

Smartphones serve as the primary consumer-facing interface for contactless transactions in mature markets. The integration of secure element (SE) technology and host card emulation (HCE) protocols has enabled smartphones to emulate traditional payment cards at merchant terminals without requiring physical card issuance. Apple Pay, Google Pay, and Samsung Pay have each built multi-hundred-million-user bases by leveraging their respective device ecosystems, biometric authentication frameworks (Face ID, fingerprint), and tokenization standards developed in partnership with Visa Inc. and Mastercard.

The wearables sub-segment — encompassing smartwatches, fitness bands, and NFC-enabled rings — is growing at a rate disproportionate to its current share, reflecting premium device penetration and the "convenience premium" consumers associate with wrist-based payments. Apple Inc. has been instrumental in normalizing wearable payments through Apple Watch, which now supports transit integration in over 50 metropolitan areas worldwide. Fitbit Pay (under Google's umbrella), Garmin Pay, and emerging players in the smart ring space — such as McLear — are broadening the addressable consumer base.

Key players dominating this segment include Apple Inc., which commands an outsized share of wearable payment transaction volume in North America and Western Europe; PayPal, Inc., whose integration with mobile commerce ecosystems positions it as a dominant digital payment intermediary; and Square, Inc. (now Block), which bridges merchant-side acceptance with consumer-side mobile payment tools. Amazon.com, Inc. has also entered the physical retail contactless space through its Amazon One palm-recognition payment system, signaling the next frontier of biometric-linked contactless commerce.

The segment's dominance is reinforced by network effects: as more merchants upgrade to NFC-capable PoS terminals, the utility of smartphone and wearable payments increases, which in turn drives consumer adoption. This virtuous cycle is self-reinforcing and has been particularly potent in urban retail, quick-service restaurants, and transit systems.

The segment's share is not merely holding — it is actively consolidating. Feature phones with NFC capability are declining in relevance, and card-not-present (CNP) transactions that previously required app-based checkout flows are being increasingly replaced by tap-to-pay interactions facilitated by tokenized credentials stored on mobile devices. The global rollout of 5G networks is augmenting this further by reducing latency in authentication and transaction confirmation.

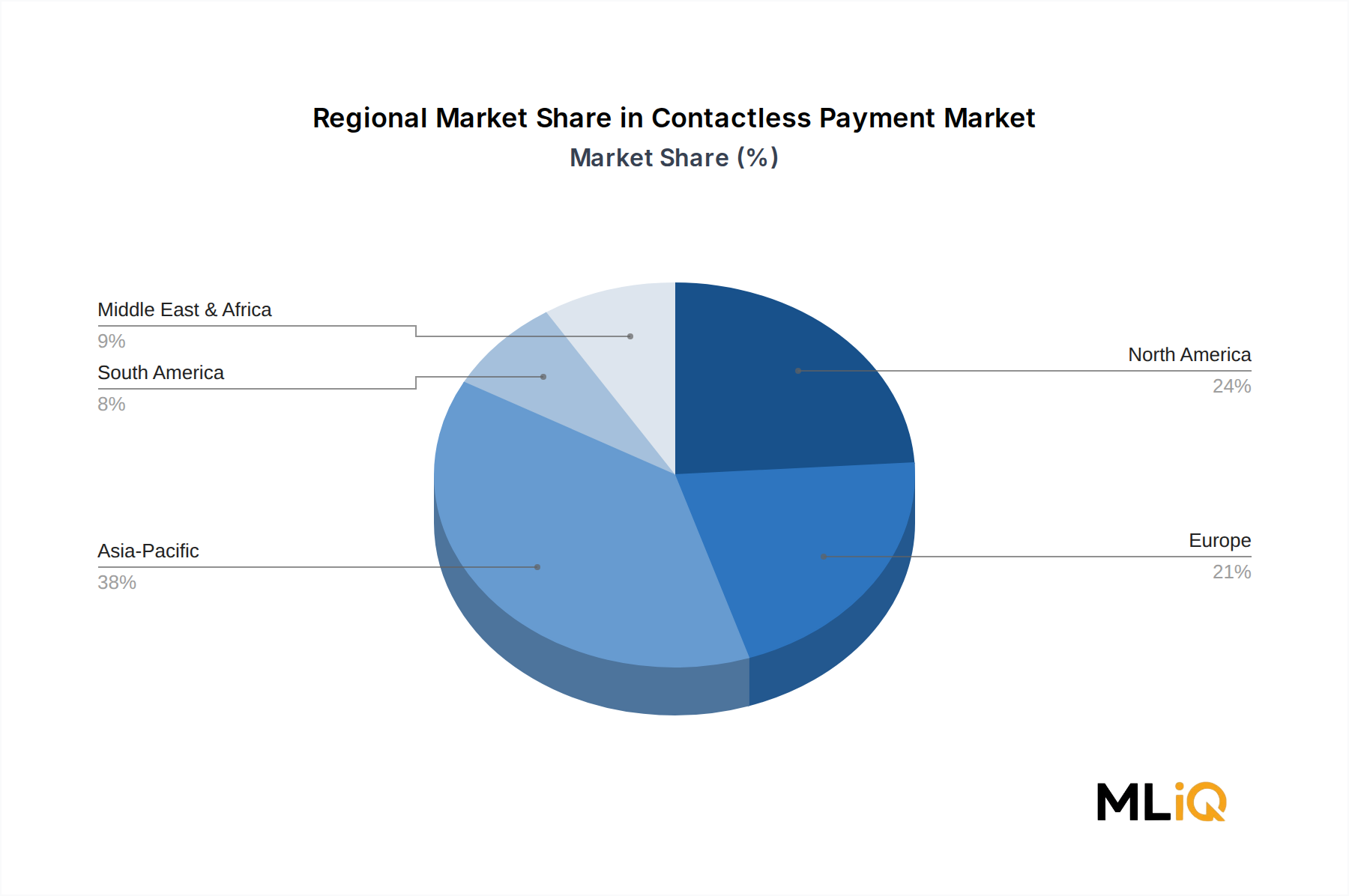

From a geographic standpoint, China leads absolute transaction volume through Alipay and WeChat Pay ecosystems — both of which operate primarily via QR code but are increasingly integrating NFC rails for international interoperability. In contrast, North America and Europe favor NFC-based tap-to-pay over QR code infrastructure, reinforcing the structural primacy of smartphone and wearable device types in those regions.

The segment's competitive moat lies in platform lock-in, biometric trust architectures, and the compounding value of transaction data for downstream credit scoring, rewards optimization, and merchant analytics — all of which competitors in the smart card or standalone PoS terminal segments cannot easily replicate.