NFC Segment Dominance in the Payment Processing Rings Market

Within the technology segmentation of the Payment Processing Rings Market, Near Field Communication (NFC) stands out as the overwhelmingly dominant sub-segment by revenue share, accounting for the majority of transactional volume processed through ring-form-factor wearables globally. The primacy of NFC in this context is not accidental — it is the product of decades of standardization efforts, merchant terminal compatibility investments, and regulatory backing across major payment jurisdictions.

NFC technology enables short-range, high-frequency wireless data exchange between devices positioned within approximately four centimeters of one another. In the context of payment processing rings, this translates to a tap-and-go transaction experience that mirrors the user behavior already normalized through contactless credit and debit cards. This behavioral continuity is a critical adoption accelerator: consumers do not need to learn an entirely new interaction paradigm, reducing friction at the point of onboarding.

The NFC Technology Market has itself undergone significant maturation, with chip miniaturization allowing increasingly powerful NFC modules to be embedded within the constrained physical geometry of a ring. Leading semiconductor suppliers have responded to demand from wearable OEMs by producing ultra-thin, low-power NFC chipsets optimized for continuous wearability, including resistance to moisture, temperature variation, and physical stress — all conditions that ring-form-factor devices must endure in everyday consumer use.

From a competitive standpoint, the NFC segment within the Payment Processing Rings Market is anchored by major payment network operators. Visa's payWave and Mastercard's PayPass technologies provide the transaction frameworks that most NFC-enabled payment rings rely upon, with device manufacturers licensing these protocols to ensure universal merchant acceptance. This creates a symbiotic relationship between hardware innovators and financial infrastructure providers, where the former benefit from network ubiquity and the latter from expanded transaction volume across novel device categories.

The NFC segment's share is not merely large — it is consolidating further. As RFID-based payment rings face growing questions around security (specifically the vulnerability of passive RFID to unauthorized scanning), the active and semi-passive NFC architecture — which incorporates mutual authentication protocols — is gaining preference among both enterprise deployers and security-conscious consumers. This dynamic is reinforcing NFC's structural advantage within the broader Radio-frequency Identification and NFC technology landscape.

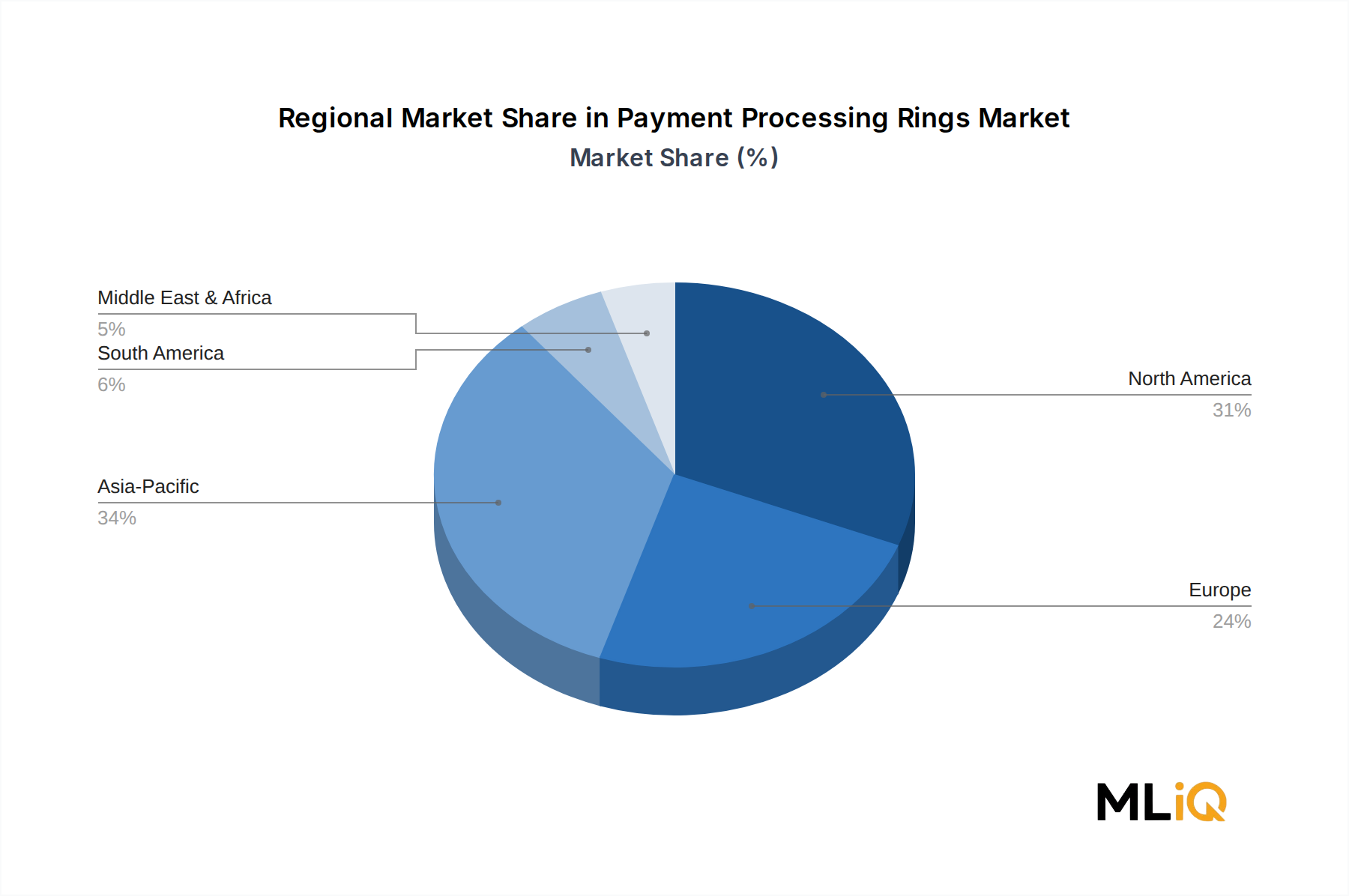

Geographically, NFC-dominant payment ring adoption is concentrated in North America, Western Europe, and advanced Asia Pacific markets such as Japan, South Korea, and Australia, where merchant terminal NFC acceptance rates exceed 85% in urban commercial environments. Emerging markets are following, though the pace is moderated by terminal infrastructure investment timelines.

Key players operating predominantly within the NFC sub-segment include Mastercard, Visa, and technology-enabling partners such as NXP Semiconductors and STMicroelectronics at the chip layer, alongside device-level manufacturers that brand and distribute the finished ring products to consumers through bank partnerships, direct-to-consumer e-commerce, and telecommunications retail channels. The segment's revenue share is expected to remain above 70% of total Payment Processing Rings Market revenue throughout the forecast period to 2033, reflecting the entrenched nature of NFC as the default standard for contactless, short-range financial transactions in wearable form factors.