Structural Unemployment Segment Dominance in the Unemployment Insurance Market

Within the Unemployment Insurance Market segmented by type, the Structural Unemployment sub-segment commands the largest revenue share, driven by the sustained displacement of workers resulting from technological automation, industry-wide transitions, and the secular decline of traditional manufacturing and clerical employment categories. Unlike cyclical unemployment, which contracts during economic recoveries, structural unemployment persists across business cycles, generating longer claim durations, higher per-beneficiary costs, and a sustained administrative burden that underpins consistent revenue generation for insurers and program administrators.

Structural unemployment has been amplified by the accelerating adoption of robotics and AI-driven automation across manufacturing, logistics, retail, and financial services sectors. Workers displaced by these forces frequently face extended benefit periods, skill retraining requirements, and geographic relocation challenges, all of which increase the actuarial complexity and total cost of insurance coverage. This persistent claim longevity makes the structural unemployment segment inherently high-value from a premium and program expenditure standpoint.

Key players operating prominently within this segment include Unemployment Insurance Services, which provides end-to-end unemployment claims management for self-insured employers navigating structural displacement events. Equifax Workforce Solutions leverages its extensive employer data networks to assist clients in verification and unemployment cost management, particularly in industries undergoing workforce restructuring. UC Alternative and Employers Edge both specialize in managing the financial liability exposure of employers facing elevated structural unemployment claims, offering cost containment strategies, appeals management, and compliance advisory services.

The structural unemployment segment also intersects meaningfully with adjacent markets. The HR Technology Solutions Market and the Workforce Management Software Market have both seen increased demand from enterprises seeking to proactively model and manage potential structural displacement before claims materialize, creating upstream revenue opportunities for integrated solution providers.

G&A Partners and Flex HR operate in the professional employer organization (PEO) space, where co-employment arrangements expose them directly to structural unemployment liabilities across diverse client industries. Their strategic positioning involves pooling employer risk across sectors, which partially offsets exposure concentration in industries with high automation displacement rates such as transportation and retail.

The share of structural unemployment within the overall market is consolidating rather than growing as a percentage of total claims volume, but its absolute revenue contribution continues to expand given rising displacement events tied to generative AI adoption and supply chain reconfigurations. Insurers and program administrators are responding by developing predictive risk scoring models that identify high-displacement-probability employers in advance, allowing for proactive reserve allocation and intervention programs.

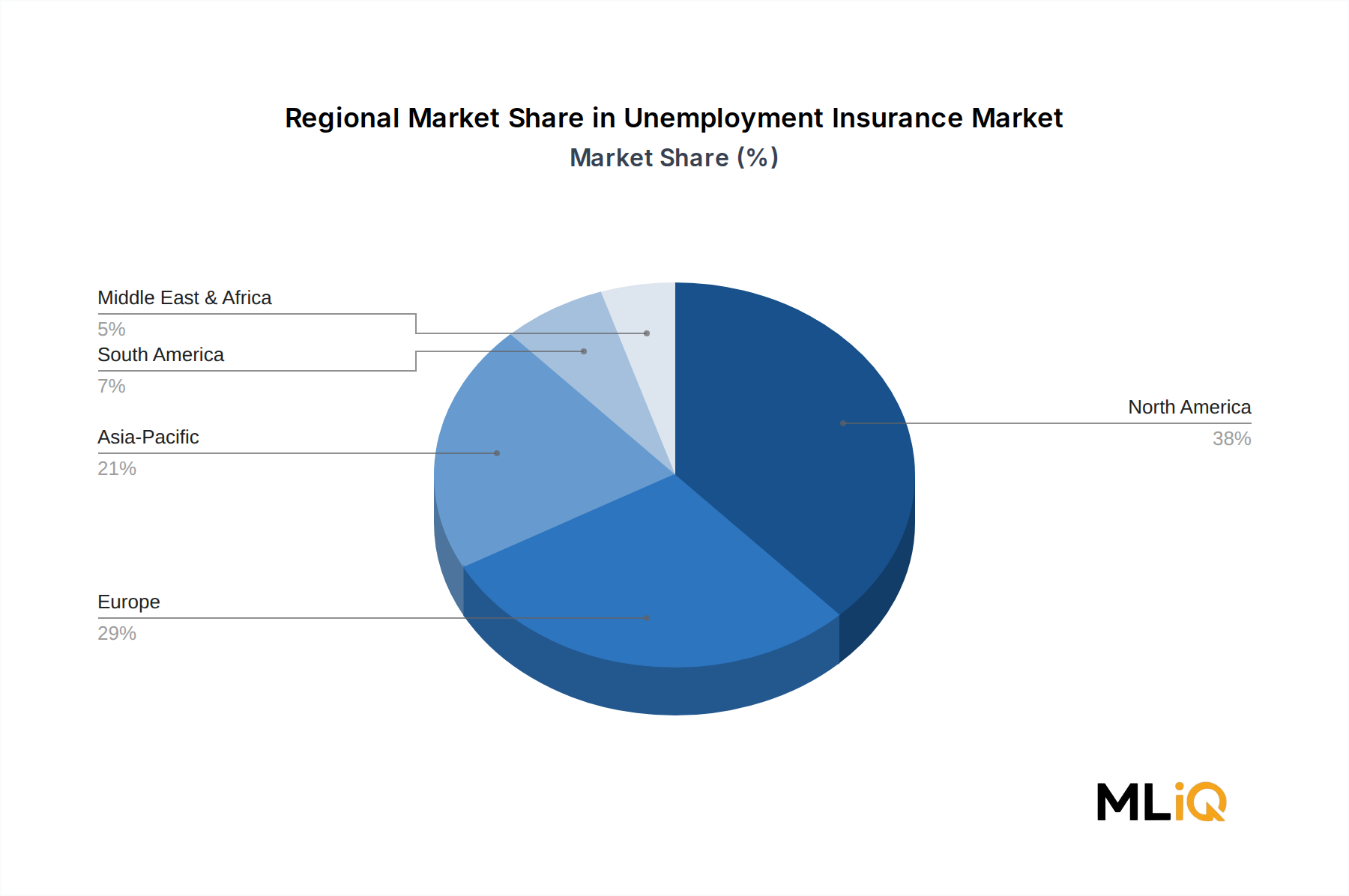

Globally, the structural unemployment segment is most pronounced in economies undergoing industrial transition, including Germany, Japan, and the United States, where legacy manufacturing employment has declined sharply. In these markets, extended benefit duration windows and retraining program mandates embedded within unemployment insurance frameworks further increase per-claim expenditure, reinforcing the segment's dominance in total market revenue contribution.