Demand Modeling & Market Estimation

Market sizing and forecasting for the Mortgage Funds Market (2026–2034) were conducted using a dual-methodology framework integrating both top-down and bottom-up approaches, further reinforced through multi-level data triangulation.

Top-Down Approach:

The top-down model began with macro-level estimates of global Assets Under Management (AUM) in fixed-income and real asset fund categories, sourced from BIS, ICI, and central bank publications. These were subsequently filtered using sector-specific allocation ratios to mortgage fund vehicles, segmented by fund type (pooled vs. contributory) and end-user category (institutional investors, banks, insurance companies, and others).

Bottom-Up Approach:

The bottom-up model was constructed using the following specific metrics and variables:

- Total Mortgage Loan Origination Volume by Geography – Measured in USD billions per annum, segmented by residential and commercial property classes, sourced from MBA, EMF-ECBC, and national central banks; used as the primary addressable pool for mortgage fund participation

- Mortgage Fund Penetration Rate – The share of total mortgage origination volume intermediated through pooled or contributory fund structures rather than direct balance sheet lending; estimated through primary interviews and regulatory filings

- Weighted Average Management Fee & Fund Return Spread – Fund-level revenue proxies derived from SEC EDGAR and ASIC disclosures, used to estimate market revenue sizing from AUM figures and validate fund manager revenue pools

- Loan-to-Value (LTV) Ratio Thresholds & Credit Quality Distribution – Used to model risk-adjusted fund capacity, estimate investor demand elasticity across interest rate scenarios, and differentiate addressable market size between conservative (senior mortgage) and higher-yield (mezzanine) fund products

Multi-Level Data Triangulation:

All market estimates were triangulated across three independent validation layers: (1) primary interview consensus estimates from fund managers and institutional investors, (2) bottom-up aggregation of origination and fund penetration data, and (3) top-down macro-financial allocation modeling. Discrepancies exceeding ±10% between layers triggered additional primary validation rounds.

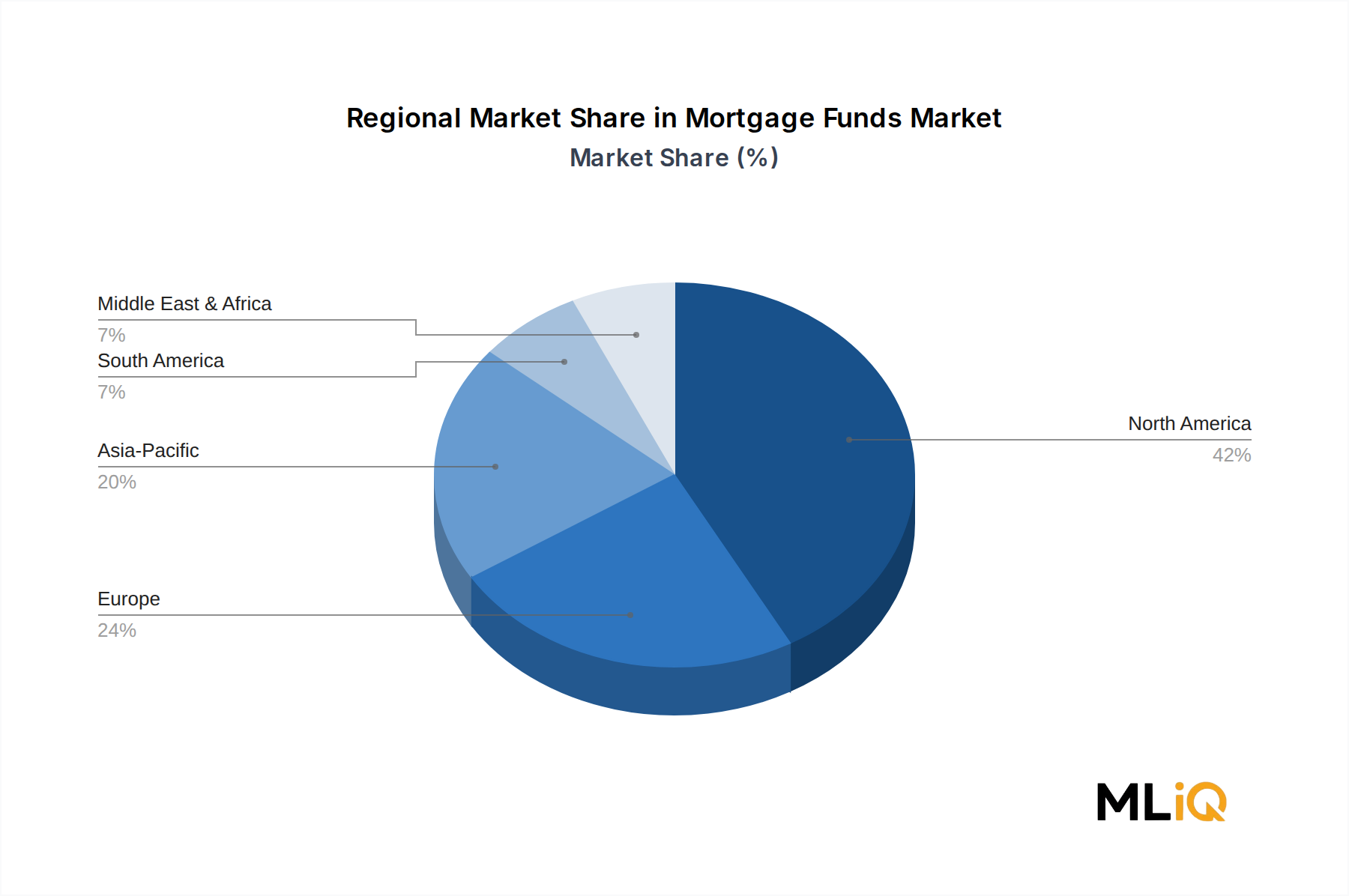

Regional forecasts were generated independently for North America, South America, Europe, Middle East & Africa, and Asia Pacific, then aggregated into global totals. Country-level estimates were modeled for key markets including the United States, Germany, United Kingdom, Australia, China, and India, with remaining geographies estimated using proxy coefficients derived from GDP per capita, mortgage market depth ratios, and regulatory maturity scores.