Open Loop Prepaid Cards: The Dominant Segment in the Prepaid Card Market

Among the various card type segments within the Prepaid Card Market, open loop prepaid cards—those operating on major payment network rails such as Visa, Mastercard, and American Express—command the largest revenue share and are consolidating their dominance as the preferred format for both consumer and institutional use cases.

Open loop cards derive their supremacy from universal merchant acceptance. Unlike closed loop variants restricted to specific retailer ecosystems, open loop cards function wherever the underlying payment network is accepted, which today encompasses virtually every point-of-sale terminal, e-commerce checkout, and ATM globally. This frictionless interoperability makes them the default choice for government disbursement programs, corporate payroll applications, and general-purpose consumer spending.

The government benefit and disbursement segment is a particularly powerful engine for open loop growth. Federal and state agencies in the United States, Canada, the United Kingdom, and across the European Union have migrated a substantial portion of benefit payments—including unemployment insurance, child support, tax refunds, and social welfare disbursements—onto open loop prepaid platforms. This transition eliminates paper check processing costs, accelerates fund delivery, and provides recipients with immediate access to funds through a universally accepted card, even without a traditional bank account.

Corporate adoption further reinforces open loop dominance. Payroll cards issued on open loop networks allow employers to deposit wages directly onto cards, enabling employees to access funds at ATMs, spend at retail locations, and conduct online transactions. For industries with large proportions of hourly and gig workers—retail, food service, construction, and healthcare—open loop payroll cards represent a cost-effective alternative to paper checks while improving financial wellness outcomes for workers.

Key players driving open loop growth include Visa Inc., which leverages its global acceptance network to power a significant portion of prepaid programs worldwide; Mastercard, which partners with banks and fintechs to deliver white-label prepaid solutions; and Green Dot Corporation, a dominant non-bank issuer in the United States operating primarily on open loop rails. NetSpend Corporation, a subsidiary of Global Payments, is another major open loop issuer with deep penetration in the underbanked consumer segment.

American Express Company also maintains a notable open loop prepaid presence, particularly within the travel, corporate expense, and gifting verticals, where its premium brand positioning commands higher average load values. PayPal Holdings, Inc. has extended its digital payments dominance into the physical prepaid space through its PayPal Prepaid Mastercard product, bridging digital wallet users with brick-and-mortar acceptance.

The competitive intensity within the open loop segment is high but not commoditized. Differentiation is increasingly achieved through mobile app integration, real-time transaction alerts, overdraft protection features, direct deposit incentives, and rewards programs. Issuers that successfully embed prepaid cards within broader financial wellness ecosystems—offering budgeting tools, savings vaults, and credit-building features—are achieving superior customer retention and higher average monthly load volumes.

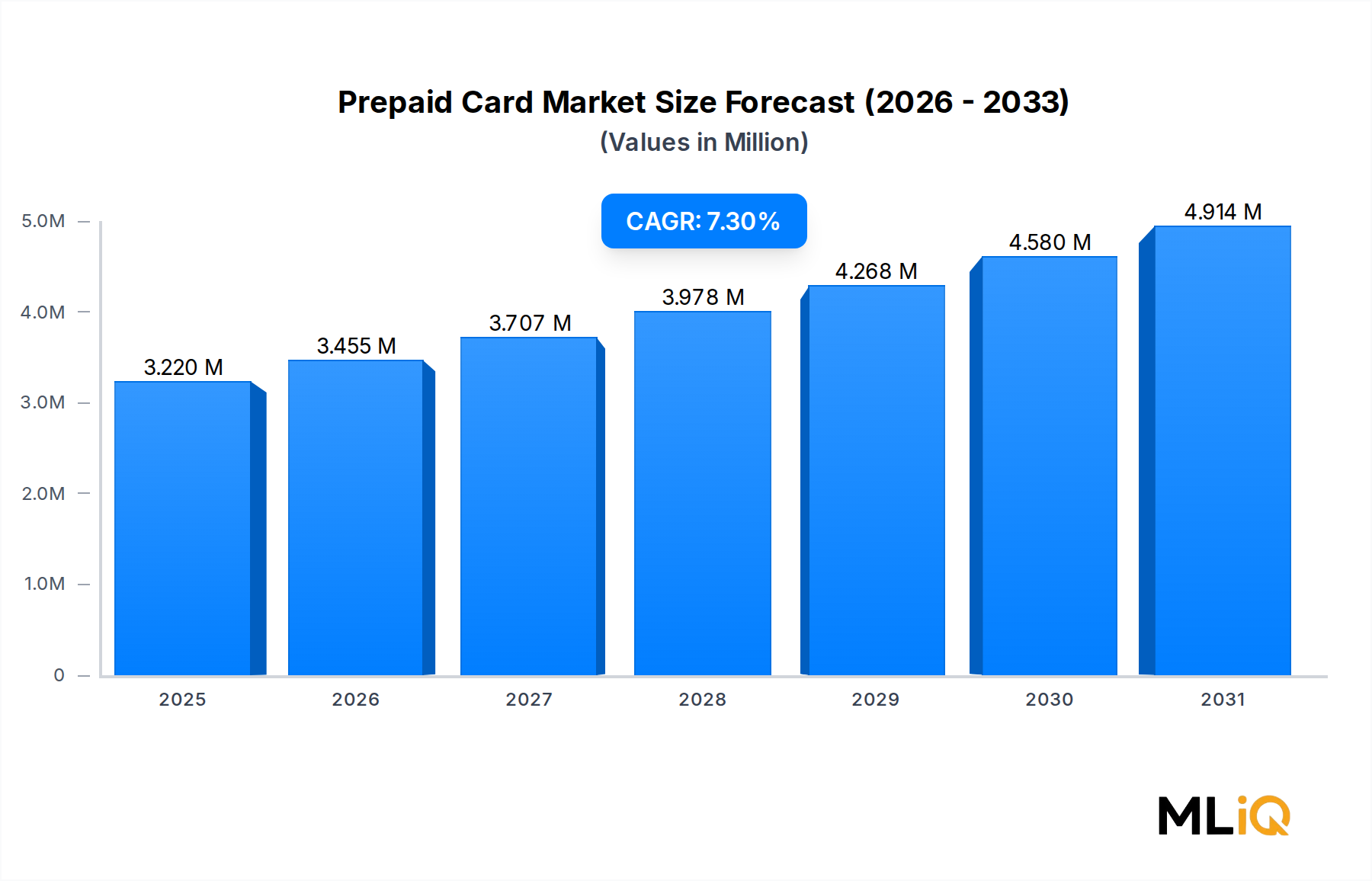

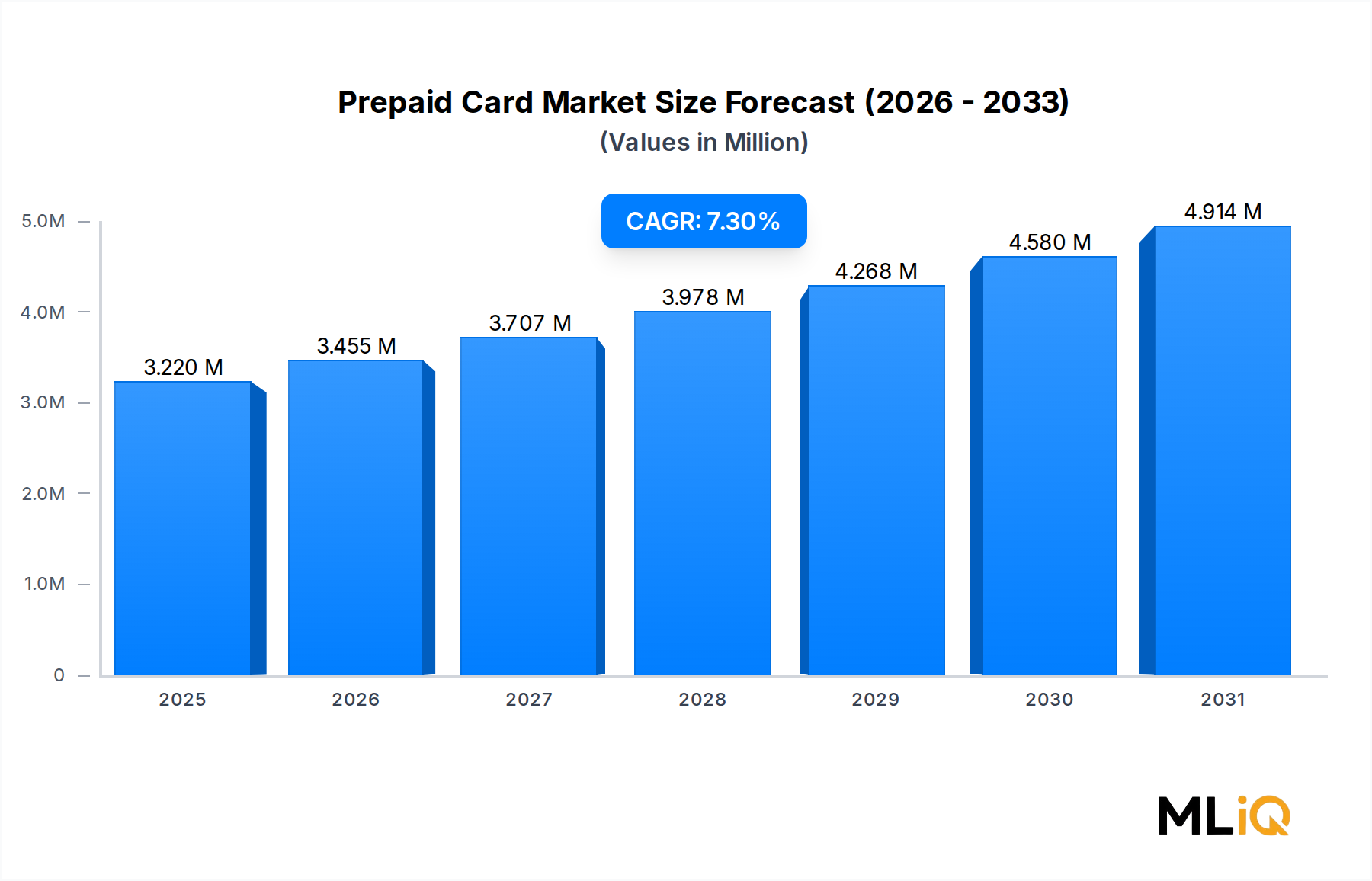

Open loop's share within the overall card type segmentation is growing, driven by the secular decline of cash as a disbursement medium and the regulatory push in multiple geographies to move public benefit payments off paper. The segment's growth trajectory is expected to remain above the overall market CAGR of 7.3% through the forecast period, as new government program mandates and fintech partnerships continue to expand the addressable use case universe.

Closed loop prepaid cards, while retaining significance within the Gift Card Market context—particularly for retail gifting and loyalty programs—are gradually ceding structural share to open loop alternatives as consumers and institutions prioritize flexibility and interoperability over retailer-specific utility.