Marine Liability Insurance Dominance in the Marine Crew Insurance Market

Within the Marine Crew Insurance Market, Marine Liability Insurance Market products constitute the single largest revenue segment, commanding an estimated share of approximately 35–40% of total premiums as of 2024. This dominance is rooted in the structural requirements of global maritime law, the systemic role of Protection & Indemnity (P&I) clubs, and the broad scope of liabilities faced by shipowners, operators, and charterers when crew welfare is implicated.

Marine liability coverage for crew encompasses a wide spectrum of obligations: compensation for injury or death during service, repatriation expenses upon contract termination or medical disembarkation, sick pay continuation, and legal defense costs arising from crew-related litigation. The MLC 2006 mandates that every vessel flagged under a ratifying state must carry documentary proof of financial security for crew claims, effectively creating a captive demand base for liability insurance products. With over 96 countries having ratified the convention—covering more than 91% of global gross tonnage—the regulatory net is nearly universal in scope.

P&I clubs, which collectively insure approximately 90% of the world's ocean-going tonnage, are the dominant institutional mechanism through which Marine Liability Insurance Market coverage is distributed. The International Group of P&I Clubs, comprising 13 principal members including the UK P&I Club, the Britannia P&I Club, and the Standard Club, operates a pooling arrangement that redistributes large losses above individual club retention thresholds, providing systemic resilience against catastrophic crew liability events. However, commercial insurers including Chubb, AXA, and Allianz are increasingly capturing market share in the fixed-premium segment by offering more flexible coverage structures and faster claims settlement timelines than traditional club arrangements.

The segment's dominance is reinforcing rather than consolidating. Several structural factors are expanding the liability exposure universe. Crew mental health claims—now formally recognized under MLC amendments—are generating a new category of long-tail liabilities. Incidents involving seafarers abandoned in foreign ports, a phenomenon that spiked during 2020–2022, have increased regulatory scrutiny on financial security adequacy and prompted several flag states to raise minimum coverage thresholds. Additionally, the criminalization of seafarers in incidents involving pollution or vessel grounding continues to generate substantial legal defense cost claims, a coverage area where commercial insurers have developed specialized products beyond P&I club scope.

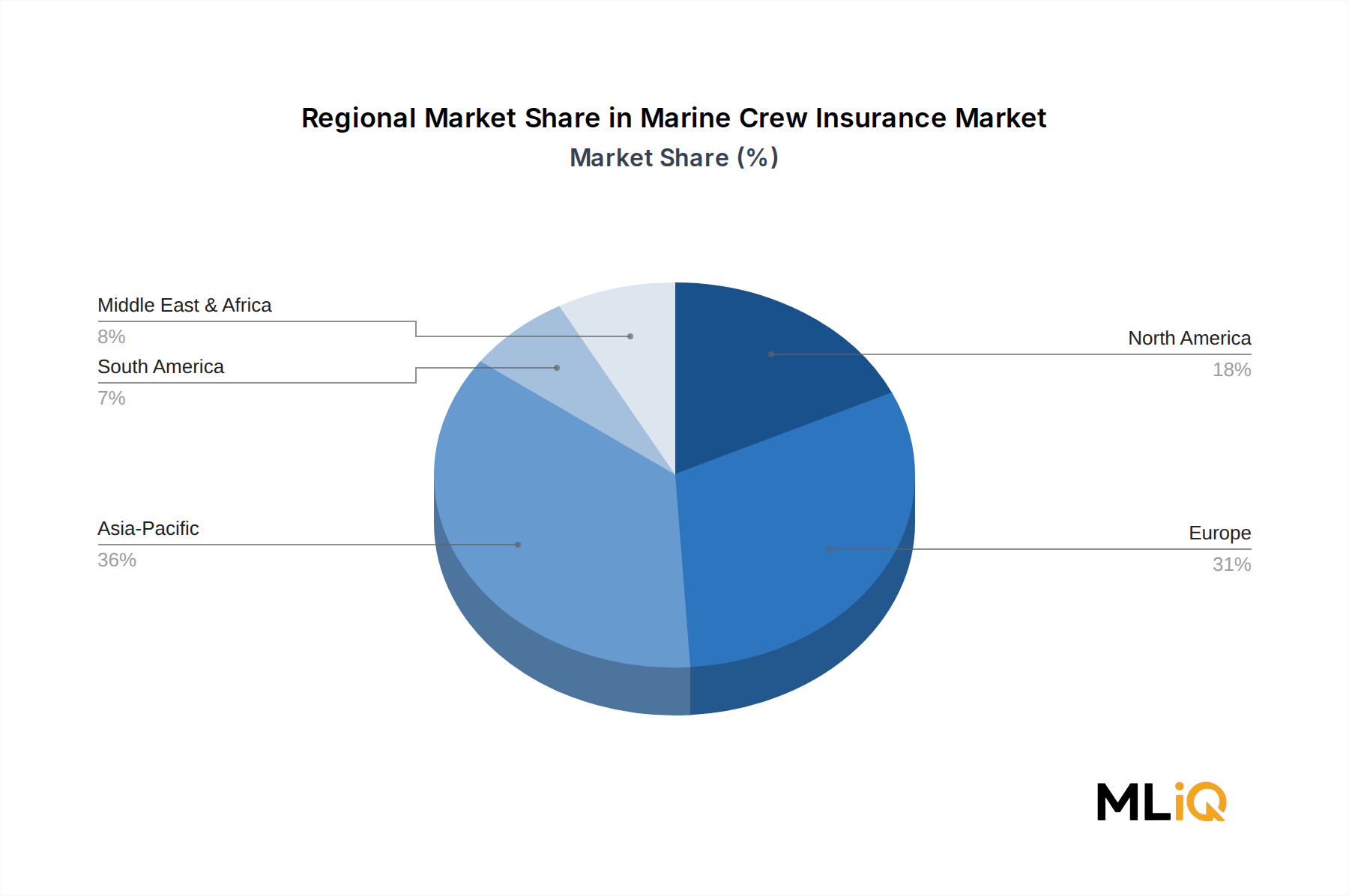

Geographically, Europe—particularly the United Kingdom and Scandinavia—remains the underwriting epicenter for marine liability, given the historical concentration of P&I club headquarters and maritime legal expertise in these regions. However, Asia Pacific is emerging as a fast-growing liability insurance market, propelled by fleet growth in China, South Korea, and Japan and the increasing sophistication of local underwriting capacity.

Key players actively competing in the marine liability sub-segment include Tokio Marine Holdings Inc., Mitsui Sumitomo Insurance Co Ltd, Atrium, and the broader Lloyds of London syndicate market. Their strategies increasingly focus on parametric trigger mechanisms for crew repatriation events, embedded telemedicine services within liability policies, and data-driven underwriting platforms that assess vessel safety records, crew certification histories, and route-specific risk profiles at policy origination.