Recombinant Factor VII Dominance in the Human Coagulation Factor VII Market by Product

Within the Human Coagulation Factor VII Market by Product, the Recombinant Factor VII sub-segment consistently commands the largest revenue share and is the primary growth engine across the forecast horizon. This dominance is attributable to multiple reinforcing clinical, regulatory, and commercial factors that collectively insulate the recombinant segment from competitive erosion.

Recombinant Factor VIIa was first approved in the 1990s for the management of bleeding episodes in hemophilia A and B patients with inhibitors — a critically underserved population for whom standard Factor VIII or IX replacement is ineffective. The mechanism of action, involving direct activation of Factor X on the surface of activated platelets independent of Factors VIII and IX, renders it uniquely valuable as a bypassing agent. Subsequent label expansions to cover congenital Factor VII deficiency, Glanzmann's thrombasthenia, and perioperative bleeding management in various surgical contexts have progressively widened the addressable patient base.

Novo Nordisk's NovoSeven (eptacog alfa) remains the global market leader within this sub-segment, benefiting from decades of clinical evidence, established reimbursement frameworks in North America and Europe, and a deeply entrenched prescriber base. The company has invested substantially in clinical extension studies and post-marketing safety surveillance, reinforcing its regulatory standing across multiple jurisdictions. Competing recombinant offerings from other manufacturers remain limited in number due to the complex manufacturing requirements for recombinant serine proteases, the significant capital investment required for mammalian cell culture infrastructure, and the difficulty of establishing clinical non-inferiority against a well-validated reference product.

The preference for recombinant Factor VII over plasma-derived alternatives in developed markets is partly safety-driven: recombinant products eliminate the theoretical risk of pathogen transmission inherent in plasma-derived manufacturing, a concern that gained renewed regulatory attention following the hemophilia community's historical exposure to HIV and hepatitis C through contaminated plasma products in the 1980s. Regulatory agencies in the United States, European Union, and Japan have generally favored recombinant therapies in their reimbursement and guidance frameworks.

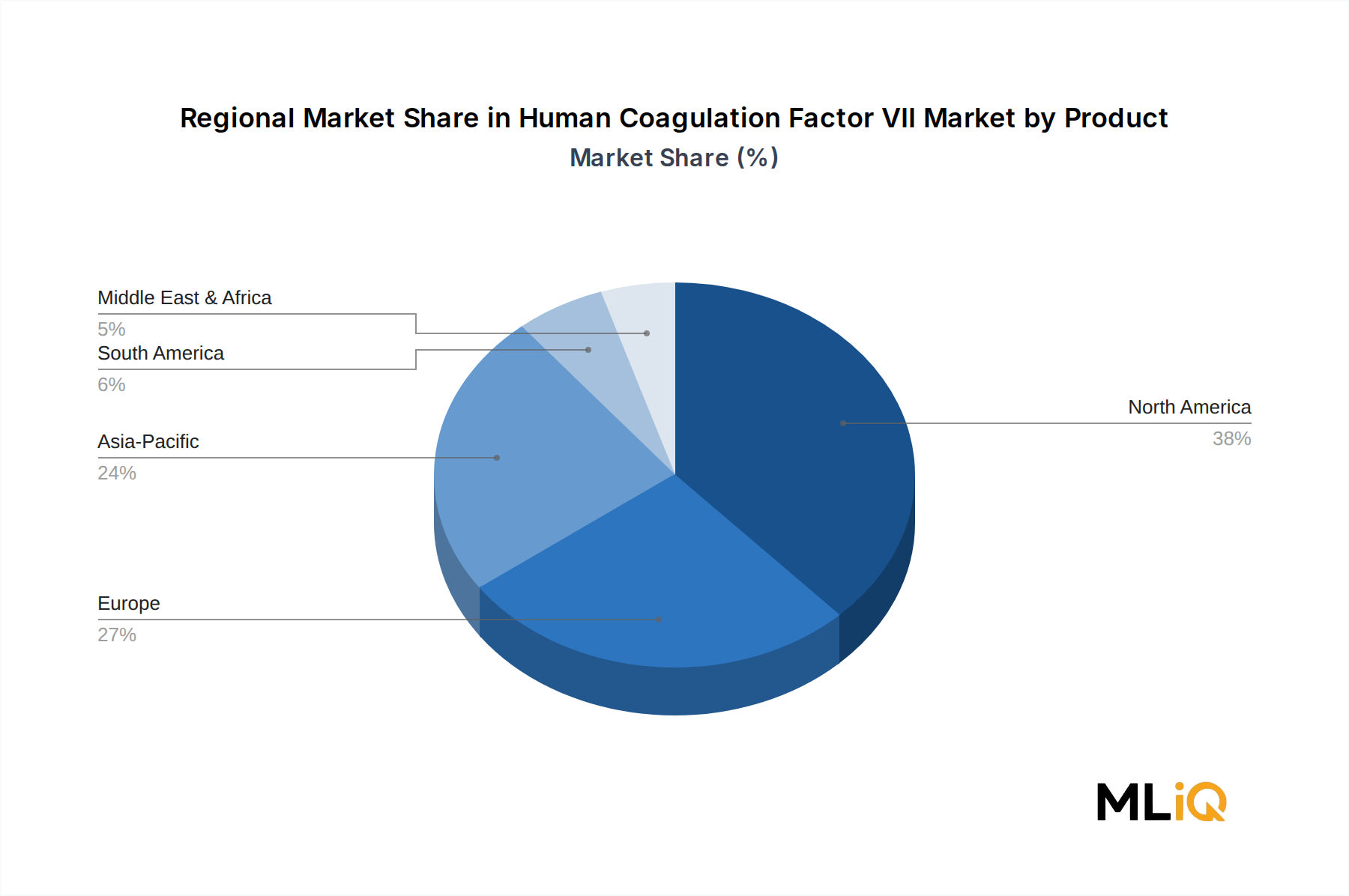

In terms of revenue concentration, North America and Europe together account for the majority of recombinant Factor VII revenues, driven by high per-patient treatment costs, comprehensive insurance coverage for rare bleeding disorders, and active hemophilia treatment center networks. The average annual cost of treatment for an inhibitor patient utilizing recombinant Factor VIIa can reach several hundred thousand USD, reflecting both the high dosing frequency and unit price of the product.

However, the recombinant sub-segment's dominance is not static. Biosimilar and follow-on recombinant Factor VIIa candidates are advancing through regulatory pipelines in multiple geographies, and several companies in Asia — particularly in China and India — are developing domestically manufactured recombinant alternatives to reduce import dependency and lower treatment costs. This biosimilar pressure is expected to introduce moderate pricing headwinds post-2027, though volume gains from expanded access are likely to offset per-unit revenue compression at the aggregate market level.

Extended half-life recombinant Factor VIIa variants, such as eptacog beta and albumin-fused constructs, represent the next phase of product evolution. These differentiated formulations offer less frequent dosing intervals and potentially improved trough factor activity, which may justify premium pricing and displace first-generation recombinant products over time. Companies including CSL Behring and Pfizer Inc. are positioned to participate in this next-generation recombinant landscape through their respective pipeline assets and manufacturing capabilities.

The recombinant segment's share is therefore consolidating at premium tiers while simultaneously broadening its volume base in emerging markets, creating a two-speed dynamic that will shape competitive strategy through the end of the forecast period.