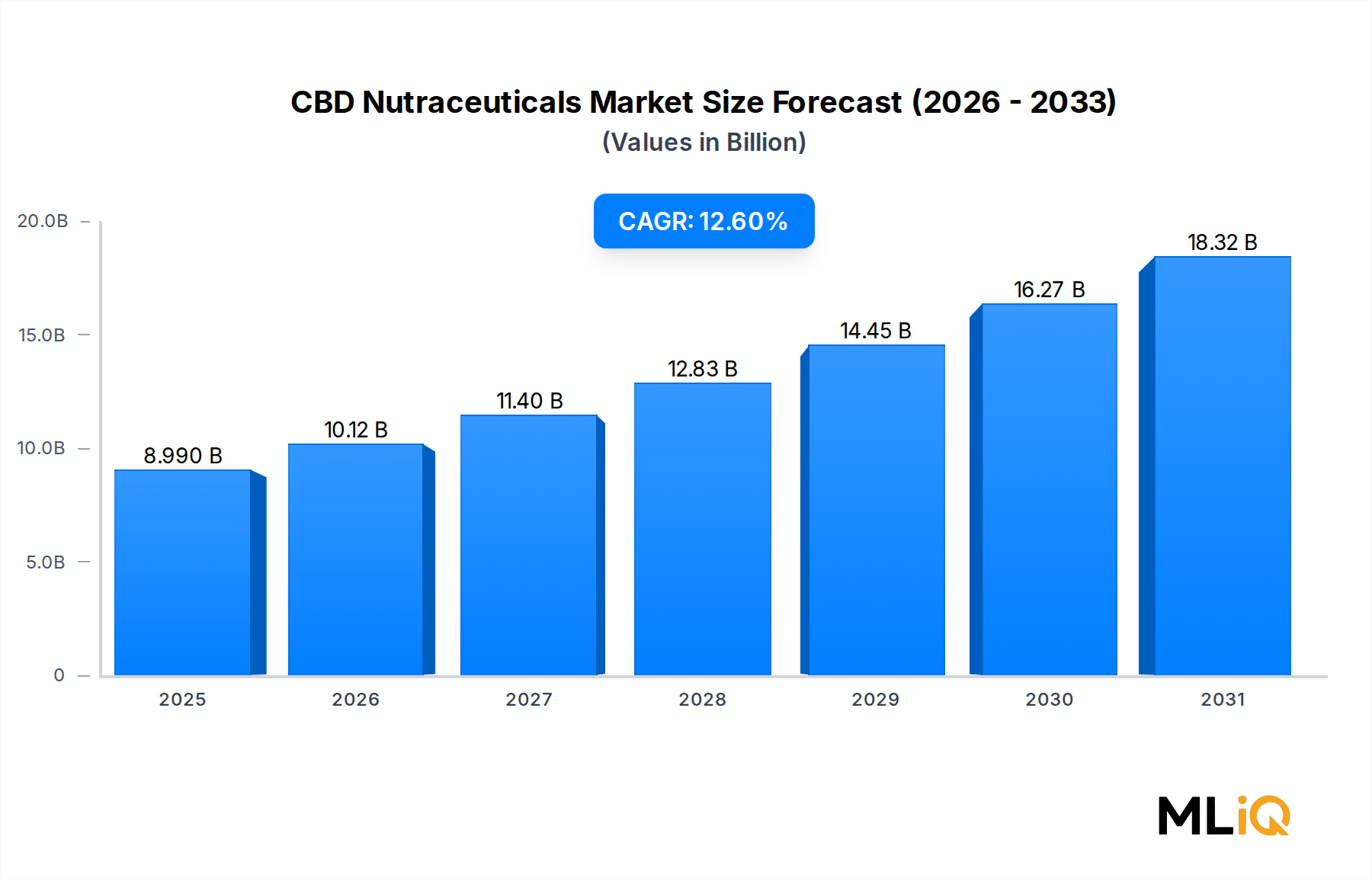

The global CBD Nutraceuticals Market was valued at $8.99 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 12.6% through the forecast period, reflecting strong underlying demand for plant-derived wellness solutions across both established and emerging economies. This growth trajectory positions the market to nearly double in absolute value within the next six to seven years, driven by a convergence of regulatory liberalization, shifting consumer health paradigms, and accelerating product innovation across multiple dosage formats.

At the macro level, the single most powerful tailwind is the global pivot toward preventive healthcare. Consumers across North America, Europe, and increasingly Asia Pacific are allocating a larger share of discretionary health spending toward non-pharmaceutical, natural-origin supplements. CBD-infused nutraceuticals sit squarely within this preference shift, benefiting from a growing body of peer-reviewed research supporting cannabidiol's potential utility in stress management, sleep quality, inflammatory response modulation, and sports recovery. This evidence base, while still maturing, has been sufficient to catalyze mainstream retail channel adoption, moving CBD nutraceuticals from specialty dispensaries and direct-to-consumer e-commerce into mass-market pharmacy chains and health food retailers.

Regulatory momentum has been a secondary but critical driver. The 2018 U.S. Farm Bill's descheduling of industrial hemp established a legal framework that enabled rapid market formalization in the United States, the world's largest single-country market. Subsequently, the European Union's Novel Food authorization pathway, though administratively demanding, has provided a structured route for brands seeking pan-European distribution. These regulatory developments have reduced market entry barriers while simultaneously raising the compliance floor, rewarding well-capitalized, quality-focused operators.

Product diversification is another key demand amplifier. The market has matured well beyond simple oil tinctures to encompass softgel capsules, protein powders, functional gummies, fortified beverages, and topical wellness formats. This diversification broadens the addressable consumer base, pulling in demographics ranging from fitness-oriented millennials to aging baby boomers seeking joint and cognitive support.

On the supply side, improvements in CO2 and ethanol extraction yields, coupled with advances in broad-spectrum and isolate refinement, have steadily compressed production costs, enabling competitive retail price points. Looking ahead, the market's outlook remains robust, with premiumization, clinical substantiation, and international market expansion serving as the three primary vectors of sustained long-term growth through 2031.