1. What are the major growth drivers for the Combi Boiler Market market?

Factors such as are projected to boost the Combi Boiler Market market expansion.

+1 2315155523

Combi Boiler Market

Combi Boiler Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

The global Combi Boiler Market was valued at approximately $29.28 million in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 4.9% through 2033, underpinned by a confluence of policy incentives, technological advancement, and shifting consumer preferences toward compact, energy-efficient heating solutions. Combination boilers — which integrate space heating and domestic hot water provision into a single unit — have gained substantial traction across residential and light commercial segments globally, displacing older, bulkier two-system configurations.

A primary demand driver is the accelerating replacement cycle for legacy boiler infrastructure in mature European markets, particularly the United Kingdom, Germany, and France, where regulatory mandates are compelling homeowners to retire inefficient atmospheric boilers in favor of modern condensing variants. European governments have consistently channeled subsidies and tax relief toward low-carbon heating upgrades, significantly reducing the total cost of ownership for end-users and stimulating replacement demand that would otherwise be price-constrained.

Beyond replacement cycles, new construction activity in Asia Pacific — notably in China, India, and ASEAN nations — is generating incremental first-time installation demand. Rising disposable income levels and urban densification are translating into stronger consumer expectations around comfort, convenience, and energy cost reduction, all of which favor combi boiler adoption in mid- to high-rise residential developments.

The integration of smart connectivity features represents a pivotal macro tailwind. Modern combi boilers increasingly ship with embedded Wi-Fi modules and compatibility with voice-activated virtual assistants, enabling remote scheduling, fault diagnostics, and occupancy-based modulation. This digital overlay is expanding the addressable market beyond traditional plumbing contractors to tech-forward homeowners and property developers seeking intelligent building ecosystems.

Strategic partnerships between boiler OEMs and smart home platform providers are reshaping go-to-market dynamics. Alliances with energy utilities and property management firms are enabling subscription-based maintenance models that lower upfront consumer resistance while securing long-term revenue streams for manufacturers.

On the supply side, raw material cost volatility — particularly for steel, copper, and aluminum used in heat exchangers — remains a margin headwind. However, continued investment in manufacturing efficiency and supply chain localization is partially offsetting these pressures.

Looking ahead to 2033, the market is expected to benefit from the global push toward decarbonization, with hydrogen-blend-ready boilers and hybrid heat pump configurations positioning the sector for structural resilience even as all-electric alternatives gain market share in selected geographies. The combination of government incentives, product innovation, and demographic-driven housing demand provides a durable foundation for sustained market growth across the forecast horizon.

Within the Combi Boiler Market, the condensing technology segment commands the largest revenue share and continues to consolidate its position relative to non-condensing alternatives. Condensing combi boilers operate by recovering latent heat from flue gases that would otherwise be expelled, achieving thermal efficiencies of 90% to 98% — compared to 70% to 80% for conventional non-condensing units. This efficiency differential is the central commercial and regulatory argument driving segment dominance.

The United Kingdom's Part L Building Regulations, Germany's Energy Saving Ordinance (EnEV), and the European Union's Ecodesign Directive have collectively mandated minimum seasonal space heating energy efficiency thresholds that effectively exclude non-condensing boilers from new-build and replacement applications in most EU member states. As a result, condensing combi boilers now represent the default specification across European new-build residential projects and the vast majority of retrofit installations.

Key players operating prominently within the condensing segment include Viessmann, which has built its product strategy around high-efficiency Vitodens condensing wall-hung boilers that incorporate stainless steel inox-radial heat exchangers for longevity and performance stability. Bosch Thermotechnology similarly anchors its Condens and Worcester Bosch product lines around condensing platforms and has invested heavily in manufacturing capacity scaling to meet replacement demand waves in the UK and Benelux markets.

BDR Thermea Group, operating through brands including Baxi and De Dietrich, leverages pan-European manufacturing footprints to supply condensing units across varied regulatory environments, while Wolf GmbH has focused on precision engineering for Central European commercial and residential applications. Ferroli S.p.A and Fondital S.p.A serve Southern European markets where condensing adoption, while lagging Northern Europe historically, is accelerating under EU Ecodesign enforcement.

The Condensing Boiler Market globally has benefited from falling component costs as economies of scale in heat exchanger manufacturing have matured. Stainless steel and aluminum heat exchangers — which are prerequisites for condensing operation — have seen per-unit cost reductions of approximately 15% to 20% over the past decade as supplier competition intensified and manufacturing processes were optimized.

Market share within the condensing segment is gradually consolidating around the top five to six OEMs, as smaller regional manufacturers face challenges meeting increasingly stringent ErP (Energy-related Products) labeling thresholds and the capital expenditure demands of connected product development. Tier-two players are responding through OEM supply agreements with larger brands rather than competing on direct-to-market channels.

The condensing segment's dominance is also reinforced by installer familiarity and servicing infrastructure. The training ecosystem — spanning manufacturers' academies, gas-safe certification programs, and distributor network support — has been calibrated around condensing technology for over a decade, creating high switching friction for alternative configurations. Looking forward, the condensing segment is expected to retain above-70% revenue share within the broader Combi Boiler Market through the forecast period, with its share ceiling defined by the pace of transition toward hybrid and heat-pump-integrated solutions rather than competitive displacement by non-condensing variants.

Several quantifiable forces are shaping the demand and supply dynamics of the Combi Boiler Market across the 2024–2033 forecast horizon.

Government Incentive Structures: The UK's Boiler Upgrade Scheme offers grants of up to £7,500 for heat pump installations but simultaneously funds gas boiler efficiency upgrades in off-gas-grid zones. Germany's Federal Office for Economic Affairs and Export Control (BAFA) allocates annual subsidies that cover up to 20% of eligible heating system replacement costs, directly accelerating combi boiler replacement cycles in the existing housing stock of over 40 million units.

Urbanization and Housing Completions: Asia Pacific residential construction output — projected to add over 30 million new urban dwelling units annually through 2030 — is generating a structural pipeline for first-time combi boiler installations. China's ongoing public housing programs and India's Pradhan Mantri Awas Yojana are particularly relevant demand contributors, even as gas network penetration in these markets remains a constraining factor relative to Europe.

Energy Price Volatility as a Double-Edged Driver: The European natural gas price spike observed during 2021–2023, with TTF benchmark prices reaching historic highs, paradoxically accelerated efficiency upgrades as consumers sought to reduce consumption per unit of heat output. Condensing combi boilers' superior efficiency translated directly into lower fuel bills, justifying replacement expenditure.

Supply Chain and Raw Material Constraints: Copper prices, a critical input for boiler heat exchangers and pipework, have exhibited sustained elevation — averaging above $8,500 per metric ton in 2023 — compressing manufacturer margins and constraining volume growth in price-sensitive market segments.

Hydrogen Transition Uncertainty: Regulatory ambiguity around the timeline for hydrogen blending in residential gas networks — with the UK's hydrogen village trials and EU's hydrogen strategy still evolving — is inducing some consumer and developer hesitancy around long-term combi boiler investment, representing a medium-term demand restraint that manufacturers are addressing through hydrogen-ready product certifications.

The Combi Boiler Market features a moderately consolidated competitive landscape dominated by European heritage manufacturers alongside diversified global HVAC conglomerates. The following profiles capture the strategic positioning of leading participants:

Ferroli S.p.A: An Italian manufacturer with strong penetration across Southern Europe, the Middle East, and Asia, Ferroli competes on value-engineered condensing and combi platforms with extensive export-oriented production capacity.

Fondital S.p.A: Another Italian specialist, Fondital focuses on aluminum radiator and boiler system integration, offering combi boiler solutions that leverage its aluminum casting expertise for lightweight heat exchanger design.

Daikin: The Japanese HVAC giant has expanded its European heating portfolio to include gas combi boilers following its acquisition of Rotex, strategically positioning boiler products as part of hybrid heat pump packages targeting the Residential Heating Market.

HTP (Heat Transfer Products): A North American manufacturer headquartered in Massachusetts, HTP concentrates on high-efficiency condensing combi boilers for the US and Canadian markets, competing on domestic hot water performance and compact form factors suited to North American apartment stock.

Bosch Thermotechnology: Operating under the Worcester Bosch brand in the UK and Bosch/Buderus in Continental Europe, Bosch Thermotechnology holds top-three market share positions in multiple European countries and invests heavily in connected product development and installer training infrastructure.

Viessmann: A German family-owned enterprise widely regarded as the premium technology benchmark, Viessmann's Vitodens product line leads on efficiency ratings and IoT integration, with recent strategic investments positioning the company at the intersection of boilers and energy management platforms.

BDR Thermea Group: A Netherlands-headquartered group encompassing Baxi, De Dietrich, and Remeha brands, BDR Thermea leverages multi-brand channel strategies to address both volume and premium residential segments across Europe.

Wolf GmbH: A German manufacturer targeting professional and commercial installers, Wolf competes on system integration depth and technical service quality within Central European markets.

A.O. Smith Corporation: Primarily known for water heating, A.O. Smith has extended its combi product range leveraging its heat transfer expertise, targeting North American and select Asian markets with combination space and water heating units.

Hoval: A Liechtenstein-based manufacturer focusing on sustainable heating and ventilation, Hoval differentiates through integrated system design and energy management for larger residential and light commercial applications.

March 2024: Viessmann completed integration of its digital energy management platform with Amazon Alexa and Google Home ecosystems, enabling voice-controlled boiler scheduling for Vitodens combi units across European markets, reinforcing its connected product leadership.

June 2024: Bosch Thermotechnology announced a manufacturing capacity expansion at its Worcester facility in the United Kingdom, committing £30 million in capital expenditure to increase annual combi boiler production volumes ahead of anticipated UK replacement demand surge.

September 2024: BDR Thermea Group launched its hydrogen-ready Baxi Assure combi boiler range, certified for operation on natural gas and up to 20% hydrogen blends, preemptively addressing anticipated UK hydrogen grid trial requirements.

November 2024: Daikin Europe announced a co-development agreement with a leading smart home platform provider to create hybrid combi boiler and air-source heat pump systems optimized for dynamic tariff response, targeting Northern European prosumer households.

January 2025: The European Commission published updated Ecodesign implementing measures requiring all new residential boiler units sold in the EU from 2029 to achieve minimum seasonal efficiency ratings of 92%, effectively tightening the entry threshold for condensing combi products.

February 2025: A.O. Smith Corporation reported a strategic distribution partnership with a major North American HVAC wholesale network, expanding its combi boiler reach into over 1,200 additional trade outlets across the United States and Canada.

April 2025: Ferroli S.p.A unveiled a new condensing combi boiler platform with integrated fault prediction algorithms and cloud-based service dispatch capabilities at the MCE Milan trade exhibition, targeting the Italian and Spanish replacement markets.

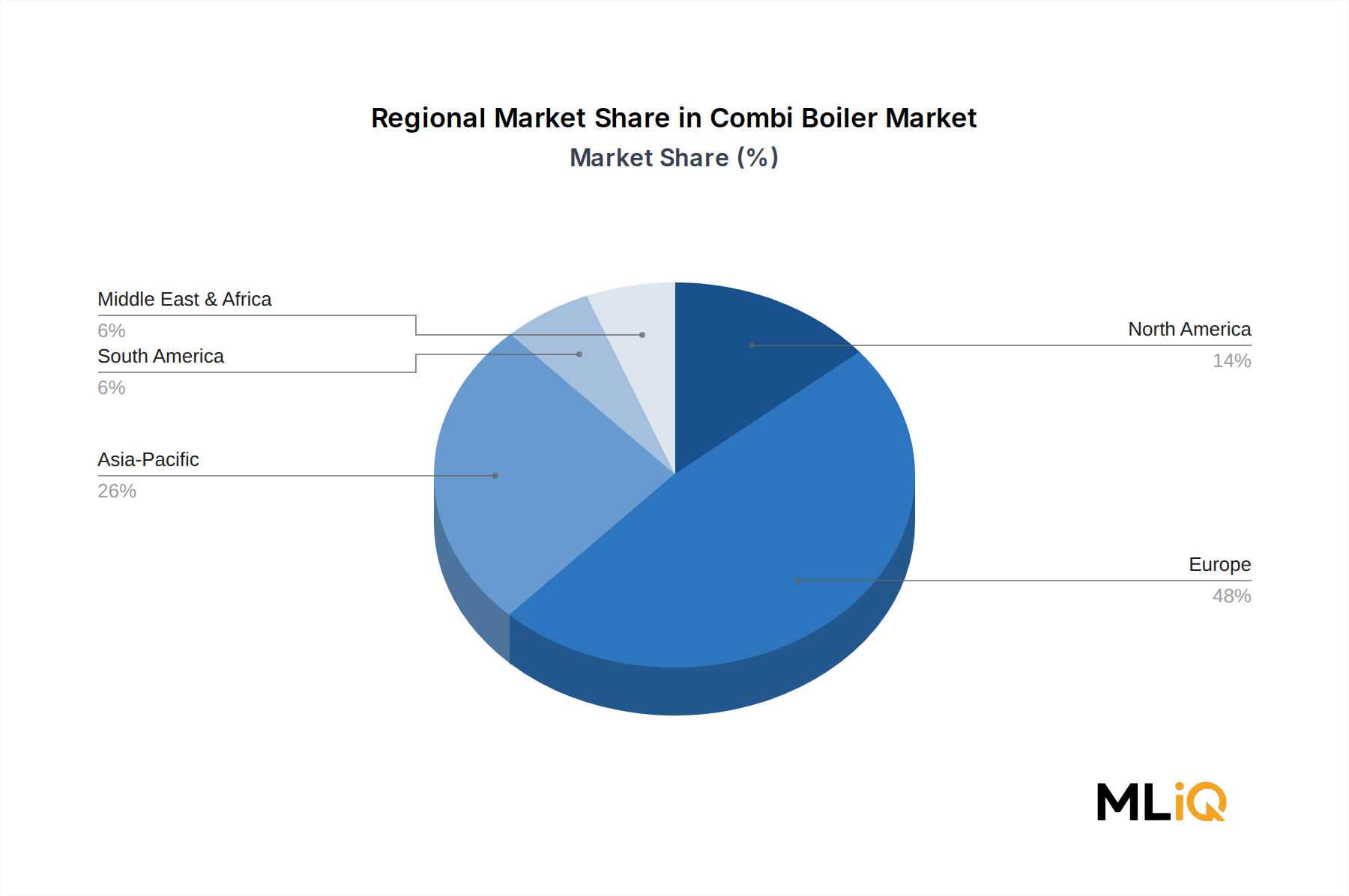

The Combi Boiler Market exhibits pronounced regional heterogeneity in terms of maturity, growth trajectory, and demand driver composition.

Europe remains the most mature and largest revenue-generating region, accounting for an estimated 55% to 60% of global market value in 2024. The United Kingdom alone represents the single largest national market by installed base, with approximately 1.7 million combi boilers installed annually. Germany and France follow as the second and third largest European markets. Regional CAGR for Europe is estimated at approximately 3.5% through 2033, constrained by market saturation in the core UK and German segments but sustained by replacement demand, efficiency upgrade mandates, and Eastern European market development.

Asia Pacific is identified as the fastest-growing regional market, with an estimated CAGR of 7.2% through 2033. Growth is concentrated in China — where urban gas network expansion is enabling gas-fired heating adoption in northern provinces — and in India, where rising middle-class household formation is driving demand for centralized space and water heating solutions. Japan and South Korea represent more mature sub-markets with entrenched domestic manufacturers but growing import competition.

North America exhibits a CAGR of approximately 4.1%, with growth anchored in high-density urban housing in the northeastern United States and Canadian metropolitan areas where combination space and domestic hot water units provide meaningful footprint and cost advantages over separate-system configurations. HTP and A.O. Smith are the primary volume competitors in this region.

The Middle East and Africa region is an emerging growth market, with the GCC sub-region showing elevated adoption rates in premium residential and hospitality construction driven by comfort expectations and energy diversification policies. Regional CAGR is estimated at 5.4%, with Turkey serving as both a production hub and domestic consumption market.

South America, led by Brazil and Argentina, represents the smallest revenue contributor but is growing at an estimated 4.8% CAGR, driven by gradual gas infrastructure build-out and urbanization in secondary cities.

Three technology vectors are exerting transformative pressure on the Combi Boiler Market's product and business model landscape over the 2025–2033 period.

Hydrogen-Compatible Combustion Systems: The development of hydrogen-blend-ready and eventually hydrogen-dedicated combi boilers is the most structurally significant technology shift. Major manufacturers including Viessmann, BDR Thermea, and Baxi have already certified units for 20% hydrogen blending without hardware modification. The evolution toward 100% hydrogen capability requires redesigned burner assemblies, modified fuel valve geometries, and updated control logic — representing R&D investments estimated industry-wide at over $500 million through 2030. Adoption timelines are contingent on national hydrogen grid infrastructure commitments, with the UK's hydrogen town trials representing the first commercial-scale proof points expected between 2026 and 2028.

AI-Driven Predictive Maintenance and Demand Response: The integration of machine learning algorithms into boiler control systems is enabling predictive fault detection — reducing emergency call-out rates by an estimated 30% to 40% in early adopter deployments — and dynamic load modulation in response to grid price signals. This capability aligns with the broader Smart Thermostat Market evolution, where devices increasingly orchestrate heating assets as flexible grid resources. OEMs partnering with energy utilities on demand-response aggregation programs are creating new B2B2C revenue models that supplement traditional hardware margins.

Hybrid Heat Pump Integration: The development of factory-matched combi boiler and air-source heat pump hybrid systems represents the most immediate competitive threat to standalone gas combi boilers in Northern European markets. These systems use the heat pump as the primary heat source at moderate outdoor temperatures and switch to the gas boiler during peak demand or cold snaps, achieving system-level efficiencies superior to either standalone technology. The Heat Pump Market and Combi Boiler Market are converging at the product architecture level, with manufacturers developing unified control

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Combi Boiler Market market expansion.

Key companies in the market include Ferroli S.p.A, Fondital S.p.A, Daikin, HTP, Bosch Thermotechnology, Viessmann, BDR Thermea Group, Wolf GmbH, A.O. Smith Corporation, Hoval.

The market segments include Fuel Type, Technology.

The market size is estimated to be USD 29.28 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Combi Boiler Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Combi Boiler Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.