1. What are the major growth drivers for the Variable life Insurance Market market?

Factors such as are projected to boost the Variable life Insurance Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

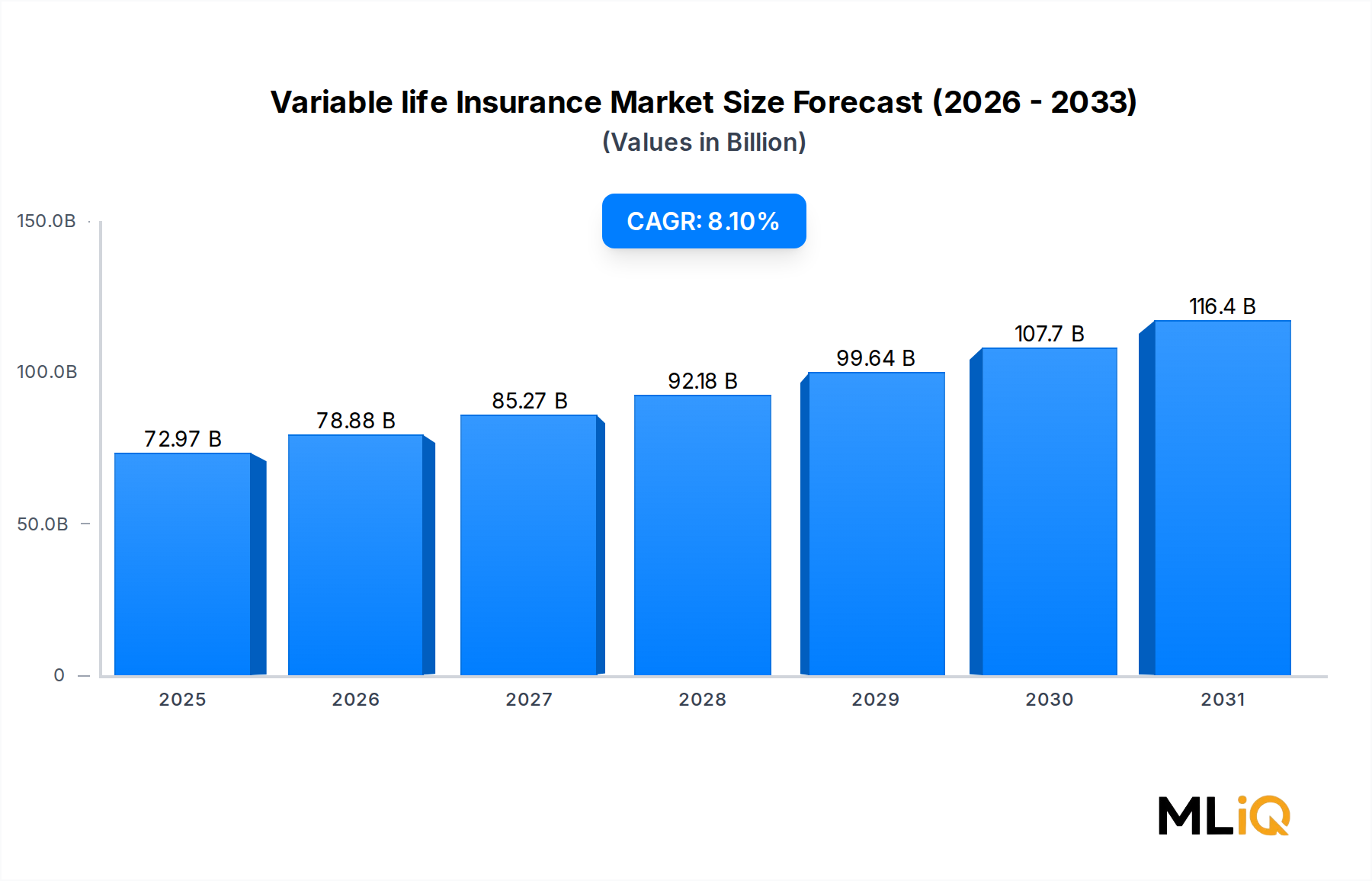

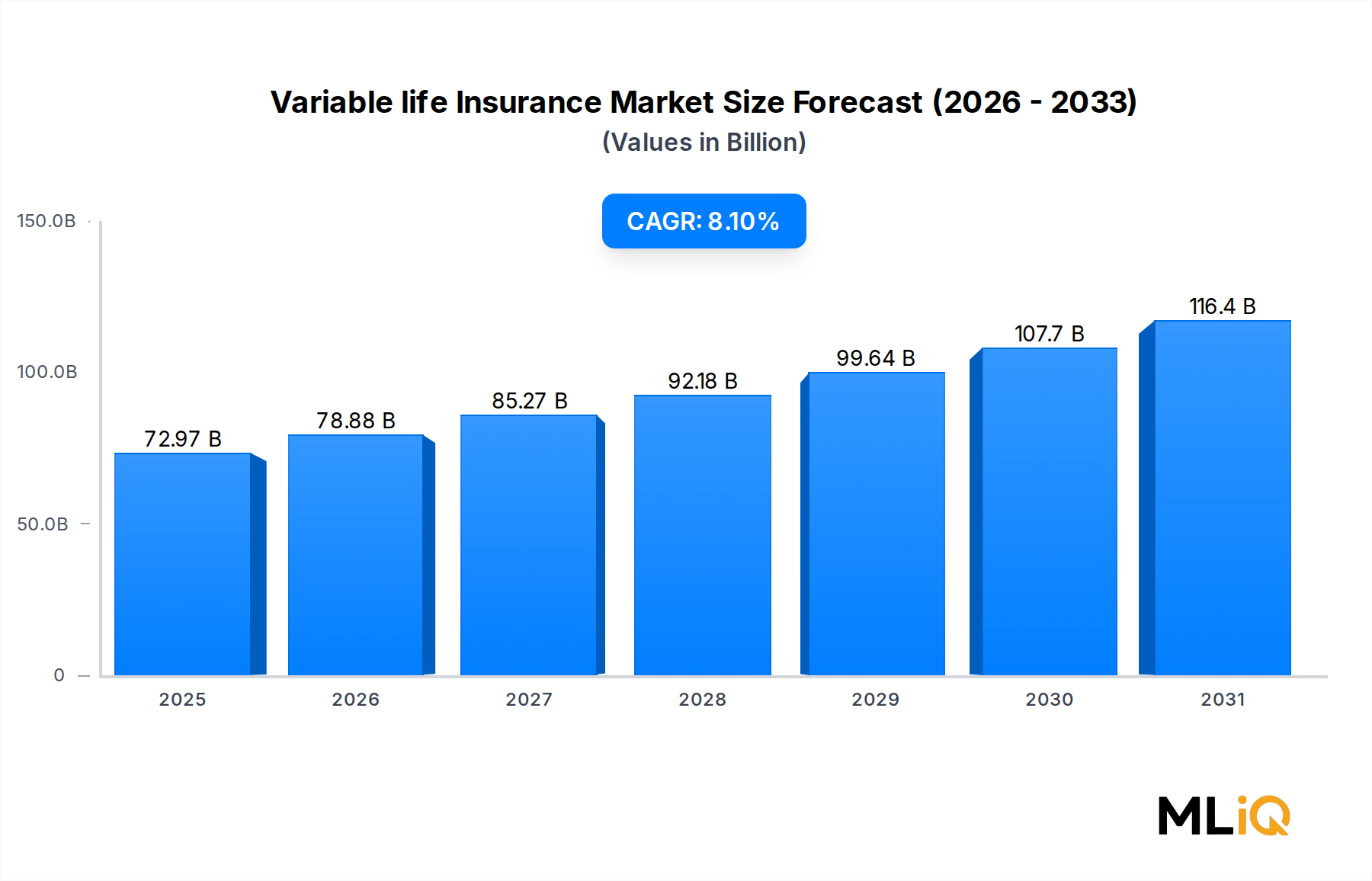

The global Variable Life Insurance Market is currently valued at $72.97 billion and is projected to expand at a compound annual growth rate (CAGR) of 8.1% through 2033, reflecting robust investor appetite for hybrid financial products that combine life coverage with market-linked investment components. This trajectory positions the market well above the broader insurance industry average, driven by a confluence of macroeconomic forces, demographic shifts, and evolving consumer financial literacy.

At its core, the Variable Life Insurance Market thrives on the dual promise of mortality protection and wealth accumulation. Policyholders allocate premiums across equity, bond, and money market sub-accounts, generating returns that fluctuate with market performance. This structural flexibility continues to attract high-net-worth individuals and long-term savers seeking tax-advantaged investment vehicles. Rising equity markets over the past decade have demonstrated the wealth-generation potential of these products, reinforcing demand among millennials and Gen X consumers entering peak earning years.

Macro tailwinds include persistently low fixed-income yields (prior to the 2022–2023 rate cycle), which eroded the appeal of traditional whole life and endowment products and redirected capital flows toward variable structures. As central banks recalibrate monetary policy, variable life products with diversified sub-account options stand to benefit from both rising yields in bond sub-accounts and continued equity participation. Simultaneously, aging populations across North America, Europe, and parts of Asia Pacific are generating sustained demand for estate planning and legacy transfer mechanisms embedded in variable life contracts.

Digital transformation has emerged as a critical accelerant. Insurers are deploying AI-driven underwriting engines, robo-advisory integration, and mobile policy-management dashboards to reduce acquisition costs and enhance policyholder engagement. These technology investments are compressing the product development cycle and enabling mass customization at scale.

Regulatory convergence — particularly fiduciary standards for financial advisors in the United States and the Insurance Distribution Directive in Europe — is reshaping distribution economics, compelling insurers to improve product transparency and fee disclosures. While this introduces compliance overhead, it ultimately strengthens consumer trust and widens the addressable market.

Looking ahead to 2033, the Variable Life Insurance Market is expected to surpass significant revenue milestones, with Asia Pacific and Latin America contributing disproportionately to incremental growth. Product innovation in ESG-linked sub-accounts, embedded digital riders, and longevity-risk features will define competitive differentiation in the next growth phase.

Among the two primary product archetypes — Fixed Premium Variable Insurance and Variable Universal Life Insurance — it is the Variable Universal Life Insurance Market segment that commands the larger revenue share and continues to consolidate its dominance. This segment's supremacy is attributable to its unmatched structural flexibility: policyholders can adjust premium payments, modify death benefit levels, and reallocate sub-account investments in response to life stage changes, market conditions, or tax planning objectives.

Variable Universal Life (VUL) policies function as a perpetual financial planning instrument rather than a static insurance contract. The adjustable premium feature allows affluent policyholders to overfund policies during high-income years, building a substantial cash value base that can later be accessed tax-free via policy loans or withdrawals. This mechanism has made VUL a cornerstone tool for business succession planning, executive compensation structuring, and high-net-worth estate planning — use cases that generate substantial annual premium volumes and persistently low lapse rates.

The growing sophistication of financial intermediaries has further entrenched VUL's market leadership. Independent broker-dealers, registered investment advisors, and bank-affiliated wealth managers increasingly incorporate VUL policies into holistic financial plans, particularly for clients with maxed-out 401(k) and IRA contribution limits. As tax legislation in the United States and analogous regimes globally continue to tighten deferred compensation structures, the tax-advantaged cash value growth in VUL policies becomes an increasingly valuable planning lever.

Key market participants within this segment include MetLife Inc., Prudential plc, Lincoln Financial Group, and Northwestern Mutual Life Insurance Company, each of which offers proprietary sub-account menus spanning hundreds of investment options from leading asset managers. Product differentiation has shifted from the insurance wrapper itself toward the quality, breadth, and cost structure of available investment options, pushing insurers to forge strategic alliances with third-party fund families.

From a revenue-share perspective, VUL policies generate higher average premium per policy than fixed premium variants due to the propensity for overfunding and the higher commissionable premium bases that attract broker distribution networks. Persistency rates in the VUL segment have historically been strong among high-income cohorts, reducing the lapse-driven earnings volatility that affects term and whole life portfolios.

Nonetheless, the segment faces regulatory scrutiny. The SEC's oversight of variable product sub-accounts as securities imposes prospectus requirements, suitability standards, and ongoing disclosure obligations that elevate compliance costs. Insurers are responding with streamlined e-delivery compliance platforms and automated suitability documentation systems.

Looking forward, VUL's share is expected to grow as insurers introduce ESG sub-account options, automated rebalancing features, and digital beneficiary management tools. The convergence of the Variable Universal Life Insurance Market with digital wealth platforms is expected to attract a new generation of financially literate consumers who view insurance and investment as a unified product category rather than separate purchasing decisions.

Several quantifiable forces are simultaneously accelerating and moderating growth across the Variable Life Insurance Market.

On the demand side, rising household wealth concentration is a primary driver. The Federal Reserve's 2023 Survey of Consumer Finances indicated that the top 10% of U.S. households by net worth hold over 66% of total wealth — a cohort that disproportionately utilizes variable life products for estate planning and tax mitigation. This wealth polarization is replicating across developed Asian economies including Japan and South Korea, expanding the addressable premium pool.

Longevity risk awareness is another measurable catalyst. Global life expectancy improvements — averaging 0.3 years per annum over the past two decades — are driving demand for financial products that support multi-decade income and protection horizons. Variable life products, with their permanent coverage and investment accumulation features, align directly with this demographic imperative.

Equity market performance correlation is a critical demand variable. Historical analysis shows that VUL new policy sales exhibit a 0.65–0.72 positive correlation with trailing 12-month equity index performance, as rising sub-account values improve the perceived value proposition during upswings. The sustained equity market expansion between 2012 and 2021 contributed meaningfully to premium volume growth during this period.

On the constraint side, market volatility presents a structural headwind. Sub-account value drawdowns during bear markets trigger increased policy lapses among lower-income policyholders and generate reputational risk for insurers, particularly when cash value erosion activates secondary guarantee provisions. The 2020 market drawdown temporarily elevated lapse rates before recovery.

Distribution cost pressure is a quantifiable constraint. Average new policy acquisition costs in the variable life segment range from 85% to 120% of first-year premiums, driven by high broker commissions and compliance overhead, compressing insurer profitability on new business and moderating aggressive market expansion strategies.

Interest rate sensitivity in hedging costs for guaranteed benefit riders also constrains product economics, particularly for insurers offering secondary guarantees on variable products.

MetLife Inc.: A global leader in the variable life segment, MetLife offers a comprehensive VUL product suite with access to over 80 investment sub-accounts. The company leverages its direct and bancassurance distribution channels to maintain top-quartile new premium market share.

Prudential plc: Operating across North America, Asia, and Africa, Prudential plc designs variable life products tailored to high-net-worth and affluent mass-market segments. Its digital distribution capabilities in Asian emerging markets represent a key growth engine.

Lincoln Financial Group: Specializing in wealth accumulation and retirement income products, Lincoln Financial Group commands a strong broker-dealer distribution network in the United States and is recognized for its transparent sub-account fee structures.

Northwestern Mutual Life Insurance Company: As one of the largest mutual insurers in the U.S., Northwestern Mutual combines captive agent distribution with proprietary investment management capabilities, generating high persistency rates in its variable life portfolio.

Transamerica Corporation: Known for its broad independent broker-dealer distribution network, Transamerica Corporation offers competitive VUL and fixed premium variable products with a focus on middle-market and mass-affluent consumers.

Guardian Life Insurance Company of America: Guardian Life Insurance Company of America emphasizes dividend-participating variable products and targets business owners and professionals through its career agency system.

Manulife Financial Corporation: With strong positions in Canada, the United States (via John Hancock), and Asia Pacific, Manulife Financial Corporation integrates behavioral wellness incentives into its variable life product design, reducing mortality costs.

Nationwide Mutual Insurance Company: Nationwide Mutual Insurance Company competes aggressively in the indexed and variable life segments, differentiating through competitive rider economics and robust wholesaler support programs.

Pacific Life Insurance Company: A prominent player in the high-net-worth VUL segment, Pacific Life Insurance Company is known for premium financing strategies and estate planning applications that target ultra-high-net-worth clients.

New York Life Insurance Company: As a mutual insurer with strong financial strength ratings, New York Life Insurance Company maintains a loyal career agent force that generates high-quality, low-lapse variable life business.

Protective Life Corporation: Protective Life Corporation focuses on cost-competitive variable and term life products, leveraging reinsurance structures to optimize capital efficiency.

Chubb Limited: Chubb Limited brings its global property and casualty distribution infrastructure to bear in cross-selling variable life products to existing corporate and high-net-worth client relationships.

Tata AIA Life Insurance Company Limited: A key player in the Indian market, Tata AIA Life Insurance Company Limited combines Tata Group's brand equity with AIA Group's insurance expertise to offer unit-linked variable life products to India's expanding middle class.

Aditya Birla Capital Ltd: Aditya Birla Capital Ltd competes in the Indian variable life segment through its integrated financial services platform, targeting urban and semi-urban consumers with digitally distributed ULIP-linked variable products.

State Farm Life Insurance Company: A dominant domestic U.S. carrier, State Farm Life Insurance Company distributes variable life products through its exclusive agent network, emphasizing simplicity and trust in policyholder communications.

Securian Financial Group, Inc.: Securian Financial Group, Inc. focuses on workplace and employer-sponsored variable life solutions, making it a distinctive player in the group and worksite distribution channel.

Allstate Insurance Company: Allstate Insurance Company has expanded its life insurance portfolio to include variable and indexed products, leveraging cross-sell opportunities within its large personal lines customer base.

Quantum Leben: Quantum Leben serves the European variable life and unit-linked segment with a focus on digital policy administration and modular product design for independent financial advisors.

The OneLife Company S.A.: The OneLife Company S.A. specializes in wealth management life insurance solutions for high-net-worth and ultra-high-net-worth clients across Europe, with expertise in cross-border estate planning structures.

FUTURE GENERALI INDIA INSURANCE COMPANY LTD.: FUTURE GENERALI INDIA INSURANCE COMPANY LTD. targets the Indian market with competitively priced variable life and ULIP products distributed through retail and digital channels.

January 2024: Lincoln Financial Group launched a next-generation VUL platform featuring real-time sub-account rebalancing and integrated ESG fund options, targeting financial advisors managing millennial and Gen Z client portfolios.

March 2024: Manulife Financial Corporation announced a strategic partnership with a leading fintech firm to embed AI-driven risk profiling tools into its variable life policy application workflow, reducing underwriting turnaround from 72 hours to under 4 hours.

May 2024: The U.S. Securities and Exchange Commission finalized updated disclosure requirements for variable life product prospectuses, mandating standardized fee comparison tables and enhanced risk disclosures, effective January 2025.

July 2024: Tata AIA Life Insurance Company Limited reported a 23% year-over-year increase in unit-linked variable life premium collections in India, driven by expanded bancassurance tie-ups with mid-tier private sector banks.

September 2024: Pacific Life Insurance Company introduced a new indexed sub-account option within its VUL product suite, allowing policyholders to participate in equity index upside with a defined floor protection mechanism.

November 2024: Prudential plc completed the acquisition of a digital insurance distribution platform in Southeast Asia, accelerating its variable life market penetration across Indonesia, Vietnam, and the Philippines.

February 2025: The European Insurance and Occupational Pensions Authority (EIOPA) issued revised guidelines on unit-linked and variable life product cost transparency under the Retail Investment Strategy framework, impacting product structuring across EU member states.

April 2025: MetLife Inc. unveiled a new suite of longevity riders attachable to its variable universal life policies, incorporating actuarial adjustments for extended life expectancy assumptions as of 2025 mortality tables.

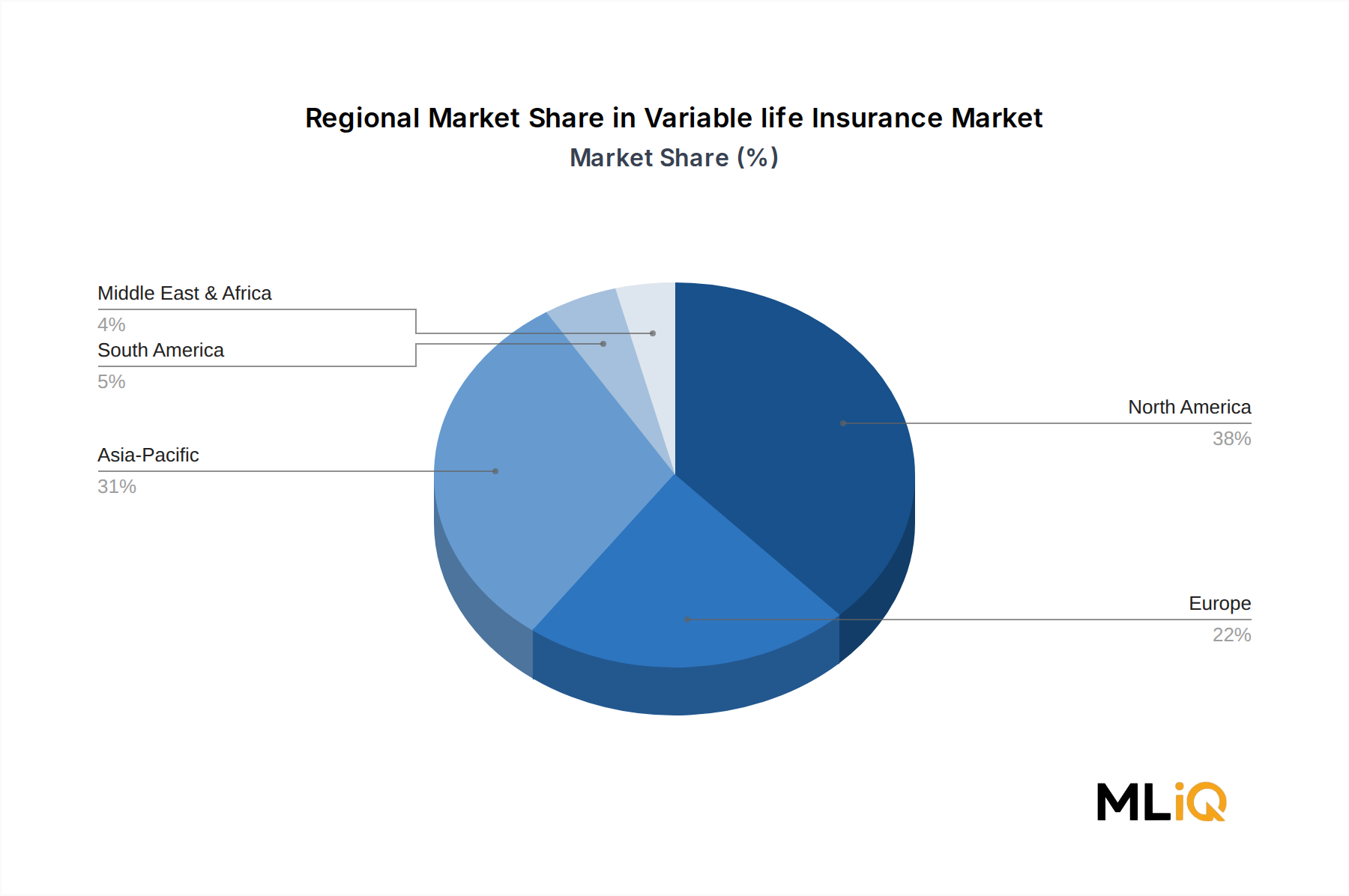

North America remains the most mature and revenue-dominant region within the Variable Life Insurance Market. The United States alone accounts for an estimated 42% of global variable life premium volume, supported by deep financial intermediary infrastructure, well-established regulatory frameworks, and a large high-net-worth consumer base with sophisticated estate planning needs. The regional CAGR for North America is estimated at 5.8% through 2033, reflecting market saturation in certain demographic cohorts but offset by product innovation and distribution channel expansion into underserved mass-affluent segments. Canada contributes incrementally, with variable life products gaining traction through bank-affiliated wealth management divisions.

Asia Pacific is the fastest-growing region in the Variable Life Insurance Market, projected to register a CAGR of 11.4% over the forecast period. China, India, Japan, South Korea, and ASEAN collectively represent a rapidly expanding addressable market, driven by growing middle-class wealth accumulation, rising insurance penetration from historically low bases, and government initiatives promoting long-term savings. India's ULIP-linked variable life segment is particularly dynamic, with double-digit premium growth underpinned by demographic dividends and digital distribution ecosystems. China's regulatory framework, while evolving, continues to channel retail investment flows into compliant variable life structures through state-affiliated and private insurers.

Europe presents a moderate growth trajectory with an estimated regional CAGR of 6.3%. The United Kingdom, Germany, and France anchor premium volumes, with growth constrained by maturing demographics, stringent MiFID II and Insurance Distribution Directive compliance requirements, and consumer preference for simpler protection products in certain markets. Cross-border wealth management life insurance — predominantly structured through Luxembourg and Liechtenstein — represents a niche but high-value growth corridor.

Latin America is an emerging contributor, with Brazil and Mexico leading variable and unit-linked life insurance adoption. The region is projected to grow at a CAGR of 9.2%, driven by expanding formal financial sector participation, dollarization of savings in high-inflation economies, and bancassurance partnerships with large regional banking groups.

Middle East and Africa represent a nascent but opportunity-rich market, with the GCC countries — particularly the UAE and Saudi Arabia — driving variable life adoption among expatriate professional populations and high-net-worth local investors, growing at an estimated 7.6% CAGR.

The Variable Life Insurance Market is stratified across three primary customer segments, each exhibiting distinct purchasing criteria, price sensitivity, and channel preferences.

The high-net-worth and ultra-high-net-worth (HNW/UHNW) segment represents the highest-value cohort by average premium. These clients — typically defined as those with investable assets exceeding $1 million — purchase variable life primarily for estate liquidity, charitable giving structures, and generation-skipping trust funding. Price sensitivity in this segment is low relative to the

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Variable life Insurance Market market expansion.

Key companies in the market include Quantum Leben, Securian Financial Group, Inc., State Farm Life Insurance Company, Northwestern Mutual Life Insurance Company, Lincoln Financial Group, Transamerica Corporation, Guardian Life Insurance Company of America, FUTURE GENERALI INDIA INSURANCE COMPANY LTD., MetLife Inc., Chubb Limited, Allstate Insurance Company, Tata AIA Life Insurance Company Limited, Pacific Life Insurance Company, Manulife Financial Corporation, Nationwide Mutual Insurance Company, The OneLife Company S.A., Aditya Birla Capital Ltd, Prudential plc, New York Life Insurance Company, Protective Life Corporation.

The market segments include Type, Application.

The market size is estimated to be USD 72.97 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Variable life Insurance Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Variable life Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.