1. What are the major growth drivers for the Sustainable Finance Market market?

Factors such as are projected to boost the Sustainable Finance Market market expansion.

Sustainable Finance Market

Sustainable Finance Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

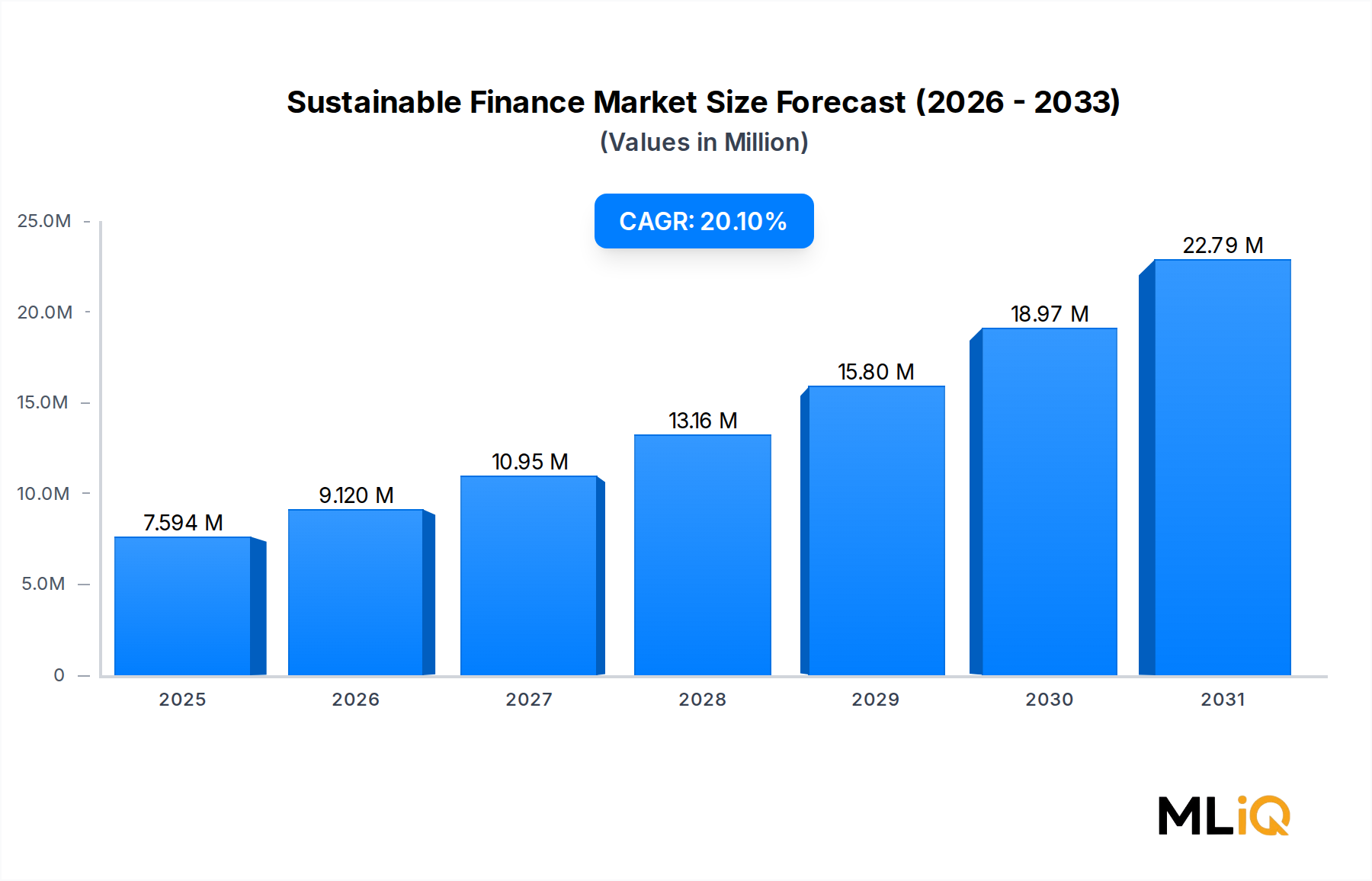

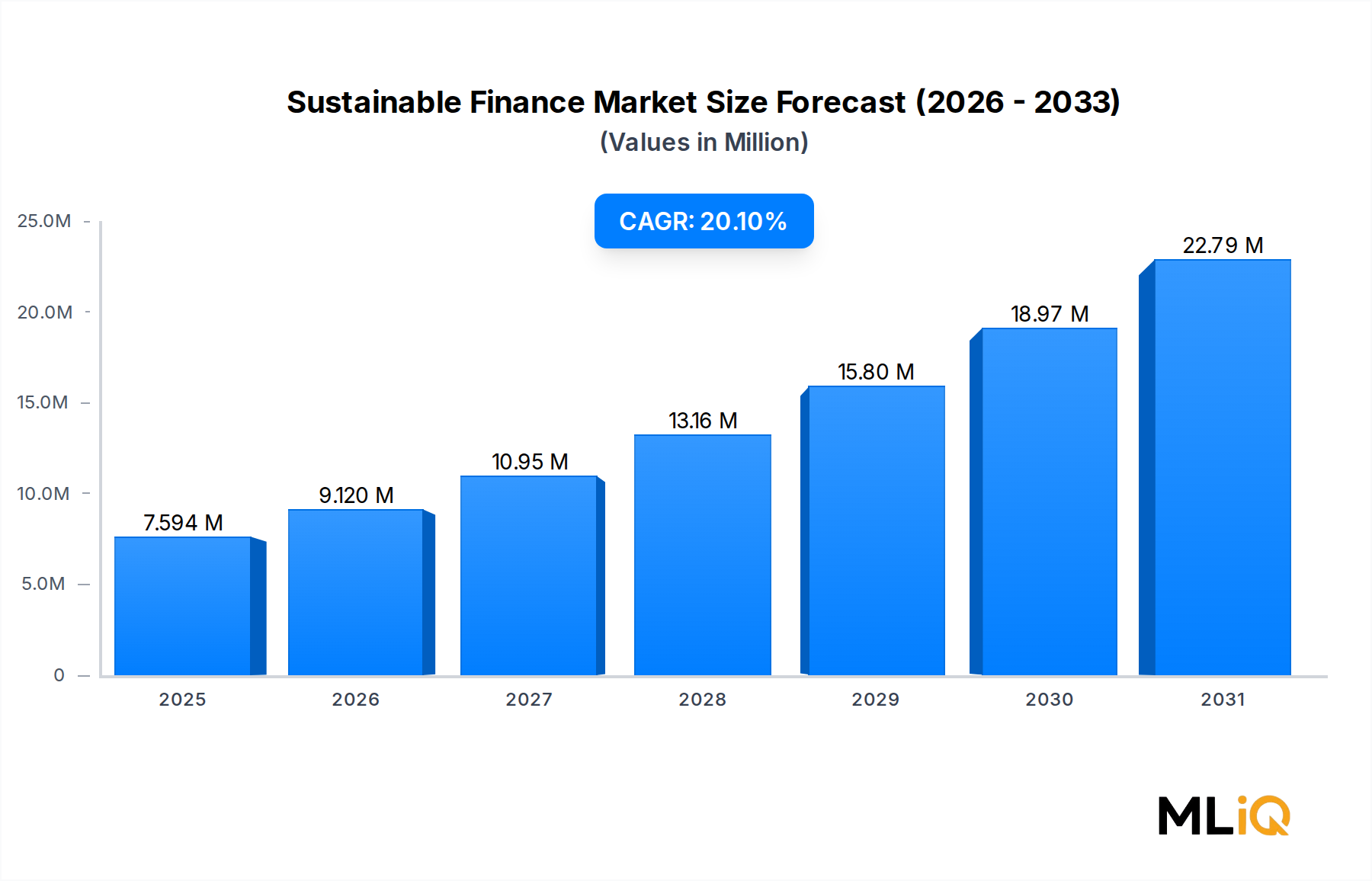

The global Sustainable Finance Market is undergoing a transformative expansion, with its valuation estimated at $7,593.90 billion as of the base assessment period. Driven by a compound annual growth rate (CAGR) of 20.1%, the market is projected to reach significantly elevated levels over the forecast horizon, positioning sustainable finance as one of the fastest-growing segments within the broader BFSI ecosystem. This exceptional growth trajectory reflects a convergence of regulatory mandates, institutional capital reallocation, and rising investor consciousness around environmental, social, and governance (ESG) considerations.

Key demand drivers underpinning this surge include the accelerating global commitment to net-zero targets under the Paris Agreement framework, the mainstreaming of ESG criteria in investment decision-making by pension funds, sovereign wealth funds, and asset managers, and the expansion of green and social bond issuance across both developed and emerging markets. Macro tailwinds further amplify these dynamics: central banks and financial regulators in the European Union, United States, China, and across the Asia Pacific region are increasingly integrating climate risk into prudential supervision, compelling financial institutions to align their balance sheets with sustainability benchmarks.

Demand is also being propelled by corporate sustainability commitments. Multinational corporations across utilities, transport and logistics, chemicals, and food and beverage sectors are issuing sustainability-linked instruments to finance decarbonization programs, creating robust pipeline activity in both equity and fixed income markets. The growing role of multilateral development banks and development finance institutions as catalysts for blended finance structures is extending the market's reach into frontier economies.

From an investment-type perspective, fixed income instruments, particularly green bonds and social bonds, dominate transaction volumes, while mixed-sustainability bonds are rapidly gaining traction as issuers seek more flexible financing frameworks. The equity segment, encompassing ESG-screened funds and impact-oriented portfolios, is also registering strong inflows as retail and institutional investors seek risk-adjusted returns aligned with sustainability outcomes.

Looking forward, the Sustainable Finance Market is expected to benefit from the proliferation of standardized disclosure frameworks, technological innovation in ESG data analytics, and the deepening integration of climate scenario analysis into mainstream portfolio management. The rising sophistication of sustainability-linked derivative instruments and transition finance products will further expand the market's addressable universe. Strategic players including Goldman Sachs, BNP Paribas, Deutsche Bank AG, and HSBC Group are positioning themselves as pivotal intermediaries in this evolving landscape, underscoring the market's institutional depth and long-term resilience.

Within the Sustainable Finance Market, the green bond segment stands as the single largest transaction type by revenue share, commanding a dominant position that reflects both historical depth and current momentum. Green bonds—debt instruments whose proceeds are exclusively applied to finance or refinance eligible green projects—have become the cornerstone instrument of the sustainable finance architecture globally. Their prominence is attributable to a well-established issuance framework, strong regulatory backing, and broad acceptance across sovereign, supranational, agency, and corporate issuer categories.

The Green Bond Market has evolved substantially since the first supranational issuance by the European Investment Bank in 2007. Today, annual global green bond issuance consistently exceeds hundreds of billions of dollars, with cumulative outstanding volumes placing this segment at the epicenter of sustainable capital markets. Within the Sustainable Finance Market's transaction type segmentation—which includes green bonds, social bonds, and mixed-sustainability bonds—green bonds account for the largest share by issuance volume and secondary market liquidity.

The dominance of green bonds is reinforced by several structural factors. First, the International Capital Market Association's (ICMA) Green Bond Principles provide a widely accepted voluntary framework that reduces information asymmetry between issuers and investors, facilitating price discovery and reducing greenium compression. Second, regulatory incentives in the European Union, particularly the EU Green Bond Standard and the EU Taxonomy Regulation, have created a defined eligibility architecture that institutional investors can integrate into their portfolio mandates. Third, central bank asset purchase programs in Europe and beyond have included green bonds in eligible collateral pools, enhancing liquidity and secondary market functionality.

From an industry vertical perspective, utilities represent the largest issuer category within the green bond space, financing large-scale renewable energy infrastructure including solar, wind, and hydropower assets. Transport and logistics issuers—including rail operators, electric vehicle manufacturers, and port authorities—constitute the second most significant issuer cohort, aligning capital expenditure with decarbonization pathways. Government and quasi-government issuers have also become major participants, with sovereign green bonds from France, Germany, the United Kingdom, and several Asia Pacific nations adding significant volume and credibility to the asset class.

Key players operating prominently within the green bond segment include BNP Paribas, which has consistently ranked among the leading green bond underwriters globally, and Goldman Sachs, whose sustainable finance division has structured and distributed notable sovereign and corporate issuances. Deutsche Bank AG has developed dedicated green bond structuring desks, while HSBC Group has positioned itself as a primary arranger across Asian and emerging market green bond issuances. Triodos Bank, a pioneer in sustainable banking, has maintained a strong focus on impact-aligned fixed income products since its founding.

The segment's share within the broader Sustainable Finance Market is consolidating rather than fragmenting. While social bonds and sustainability-linked bonds have experienced faster percentage growth rates in recent years—partly driven by pandemic-era social financing needs—green bonds retain their leadership position due to investor familiarity, secondary market depth, and the breadth of eligible project categories under evolving taxonomy frameworks. The anticipated rollout of the EU Green Bond Standard as a best-practice benchmark is expected to further institutionalize issuance quality and investor confidence, cementing green bonds' dominant position through the forecast period.

The convergence of green bond structures with transition finance frameworks—addressing hard-to-abate sectors such as chemicals and heavy industry—represents the next frontier of product innovation within this segment, potentially expanding the addressable issuer universe and sustaining volume growth.

The Sustainable Finance Market is shaped by a robust set of quantifiable drivers alongside notable structural constraints that collectively determine its growth velocity and geographic distribution.

Among primary drivers, regulatory mandates constitute the most powerful accelerant. The European Union's Sustainable Finance Disclosure Regulation (SFDR), effective from March 2021, has compelled over 50,000 financial market participants across the EU to disclose sustainability risks and adverse impacts, directly channeling institutional capital toward sustainable instruments. The Taxonomy Regulation's six environmental objectives provide a codified framework that has already classified trillions of euros of economic activities, creating a compliance-driven demand for sustainable investment products.

Institutional capital reallocation is a second major driver. Global ESG assets under management surpassed $35 trillion in recent years according to industry estimates, representing approximately one-third of total global AUM. This reallocation is structurally driven by pension fund trustees and insurance companies incorporating ESG risk factors into fiduciary duty interpretations, supported by guidance from bodies such as the UN Principles for Responsible Investment (PRI), which counts over 5,000 signatories representing more than $120 trillion in AUM.

Corporate net-zero commitments represent a third driver: over 9,000 companies have submitted science-based targets through the Science Based Targets initiative (SBTi), each requiring capital financing for decarbonization, creating direct demand for sustainability-linked loans and bonds within the Sustainable Finance Market.

On the constraint side, greenwashing risk and inconsistent taxonomy standards across jurisdictions create investor uncertainty. The absence of a globally harmonized green taxonomy—with divergence between the EU, China, ASEAN, and the United States frameworks—increases transaction costs and due diligence burdens, particularly for cross-border issuances. Data quality and ESG rating inconsistency represent an additional constraint: studies have documented correlation coefficients as low as 0.54 between major ESG rating agencies' scores for identical corporates, undermining portfolio construction discipline and investor confidence.

Arabesque: A pioneer in AI-driven ESG data analytics, Arabesque integrates quantitative sustainability scoring into asset management workflows, enabling fund managers to systematically align portfolios with ESG benchmarks within the Sustainable Finance Market.

Deutsche Bank AG: One of the world's largest financial institutions with a dedicated sustainable finance team, Deutsche Bank AG has underwritten billions in green and sustainability-linked bonds while offering ESG advisory services to corporate and sovereign clients.

Acuity Knowledge Partners: Specializes in research and analytics outsourcing for sustainable finance, providing ESG research support, green bond verification, and impact reporting services to global asset managers and investment banks.

Triodos Bank: A mission-driven bank exclusively focused on financing sustainable enterprises across energy, agriculture, culture, and social sectors, Triodos Bank operates as a benchmark institution for impact-oriented lending and deposit products.

South Pole: A leading carbon project developer and sustainability solutions provider, South Pole enables corporate clients to access voluntary carbon markets, develop nature-based solutions, and structure net-zero transition strategies.

Starling Bank: A digital-native challenger bank incorporating sustainability metrics into retail banking products, Starling Bank exemplifies the growing role of neobanks in democratizing access to green financial products.

Aspiration Partners, Inc.: A U.S.-based fintech offering sustainable financial services to consumers, including carbon footprint tracking, fossil-fuel-free investment accounts, and plant-a-tree debit card programs.

Goldman Sachs: A global investment banking powerhouse that has committed over $750 billion to sustainable finance initiatives, Goldman Sachs operates across green bond underwriting, ESG equity products, and climate infrastructure investment.

NOMURA HOLDINGS, INC.: Japan's largest investment bank, NOMURA HOLDINGS, INC. has expanded its sustainable finance capabilities across Asian capital markets, including green bond distribution and ESG-linked structured products.

KPMG International: A global professional services firm providing ESG assurance, sustainability reporting advisory, and green finance verification services to financial institutions and corporates navigating the Sustainable Finance Market.

Stripe: A global payments technology company that has embedded sustainability into its infrastructure through Stripe Climate, facilitating carbon removal purchases via API integrations with millions of businesses.

Clarity AI: A technology company delivering sustainability analytics and regulatory reporting solutions to asset managers, helping them comply with SFDR, EU Taxonomy, and other disclosure mandates.

PwC: A Big Four professional services firm with a dedicated sustainable finance and ESG practice, PwC provides assurance, strategy, and regulatory compliance services to financial institutions and corporates globally.

HSBC Group: One of the world's largest banks, HSBC Group has committed to providing $750 billion to $1 trillion in sustainable finance and investment by 2030, with significant green bond issuance and structured sustainability-linked lending activity.

Treecard: A green fintech startup offering a wooden debit card backed by sustainable spending, directing a portion of revenues toward reforestation programs, representing the retail segment of sustainable banking innovation.

Refinitiv: A global financial data and infrastructure provider offering ESG scoring, green bond data, and sustainable finance analytics products that power investment decision-making across institutional platforms.

BNP Paribas: Europe's largest bank by assets, BNP Paribas has positioned itself as a market leader in green bond origination, social bond structuring, and ESG financing across corporate, sovereign, and municipal clients globally.

January 2024: The European Securities and Markets Authority (ESMA) published updated guidelines on fund naming conventions related to ESG and sustainability terms, directly impacting over 3,600 EU-domiciled funds and reshaping product labeling across the Sustainable Finance Market.

March 2024: Goldman Sachs launched a new sustainability-linked lending facility totaling $5 billion targeted at mid-market corporates in North America committing to verified science-based emissions reduction targets.

April 2024: The International Sustainability Standards Board (ISSB) reported that over 20 jurisdictions had formally committed to adopting or aligning with IFRS S1 and IFRS S2 climate disclosure standards, creating a near-global baseline for sustainability reporting.

June 2024: BNP Paribas completed the structuring of a €3 billion sovereign sustainability bond for a European government, representing one of the largest single sustainable sovereign issuances of the year.

August 2024: South Pole announced a strategic partnership with a consortium of Asian development banks to scale nature-based carbon credit origination across Southeast Asia, targeting 50 million verified carbon credits over five years.

October 2024: HSBC Group announced the expansion of its sustainable trade finance program into 15 new markets across Africa and Southeast Asia, extending green and social trade instruments to SME exporters in high-growth corridors.

December 2024: Clarity AI secured a Series C funding round, raising $80 million to accelerate development of AI-powered regulatory reporting tools for SFDR and EU Taxonomy compliance, reflecting rising institutional demand for automated ESG data infrastructure.

February 2025: The G20 Sustainable Finance Working Group released its updated roadmap prioritizing transition finance frameworks, blended finance for emerging markets, and biodiversity-related financial disclosures as priority themes for 2025–2026.

The Sustainable Finance Market exhibits pronounced regional heterogeneity in terms of market maturity, growth velocity, and primary demand drivers, with five major regions each presenting distinct dynamics.

Europe remains the most mature and largest regional market, accounting for an estimated 40–45% of global sustainable finance activity. The region's leadership is anchored by the European Union's comprehensive regulatory architecture, including SFDR, the EU Taxonomy Regulation, and the Corporate Sustainability Reporting Directive (CSRD). The United Kingdom, Germany, France, and the Nordics collectively represent the deepest pools of green bond issuance and ESG fund AUM. European regional CAGR is estimated at approximately 15–17%, reflecting a market that is consolidating rather than in early hyper-growth. Germany leads in green bond sovereign issuance, while France has pioneered sovereign sustainability-linked instruments.

North America represents the second largest regional market, driven primarily by the United States and increasingly by Canada. Following the passage of the Inflation Reduction Act in 2022, U.S.-based sustainable investment flows accelerated materially, with $369 billion in climate and clean energy incentives catalyzing private capital mobilization. The United States sustainable finance CAGR is projected at approximately 18–20%, supported by state-level ESG investment mandates, corporate net-zero commitments from Fortune 500 companies, and the expansion of the voluntary carbon market.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 22–25%, led by China, Japan, South Korea, and the ASEAN bloc. China alone has become the world's largest green bond issuer by cumulative volume, driven by government-directed capital allocation toward renewable energy and clean transportation. Japan's transition finance agenda—addressing its unique dependence on industrial carbon-intensive sectors—is creating significant demand for sustainability-linked instruments. India's green bond market is expanding rapidly following the sovereign's debut green bond issuance in 2023.

The Middle East & Africa region is emerging as a new frontier for sustainable finance, with the GCC states leveraging sovereign wealth fund mandates and Vision 2030-type programs to channel capital toward clean energy and infrastructure. South Africa has the continent's most developed green bond market. Regional CAGR is estimated at 19–21%.

South America, led by Brazil and its biodiversity finance agenda, presents significant opportunity particularly in nature-based solutions and sustainable agriculture finance, with regional CAGR approximating 17–19%.

Technology is reshaping the Sustainable Finance Market at an accelerating pace, with three primary innovation vectors emerging as most disruptive to incumbent business models and value chains.

First, artificial intelligence and machine learning applied to ESG data processing represent the most broadly impactful technological shift. Traditional ESG scoring methodologies rely on lagged, self-reported corporate data; AI-powered platforms such as those operated by Arabesque, Clarity AI, and Refinitiv are ingesting alternative data streams—satellite imagery for deforestation monitoring, NLP-processed regulatory filings, supply chain shipment data, and social media sentiment—to produce real-time

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Sustainable Finance Market market expansion.

Key companies in the market include Arabesque, Deutsche Bank AG, Acuity Knowledge Partners, Triodos Bank, South Pole, Starling Bank, Aspiration Partners, Inc., Goldman Sachs, NOMURA HOLDINGS, INC., KPMG International, Stripe, Clarity AI, Pwc, HSBC Group, Treecard, Refinitiv, BNP Paribas.

The market segments include Investment Type, Transaction Type, Industry Verticals.

The market size is estimated to be USD 7593.90 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Sustainable Finance Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Sustainable Finance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.