1. What are the major growth drivers for the Medical Insurance Market market?

Factors such as are projected to boost the Medical Insurance Market market expansion.

+1 2315155523

Medical Insurance Market

Medical Insurance Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

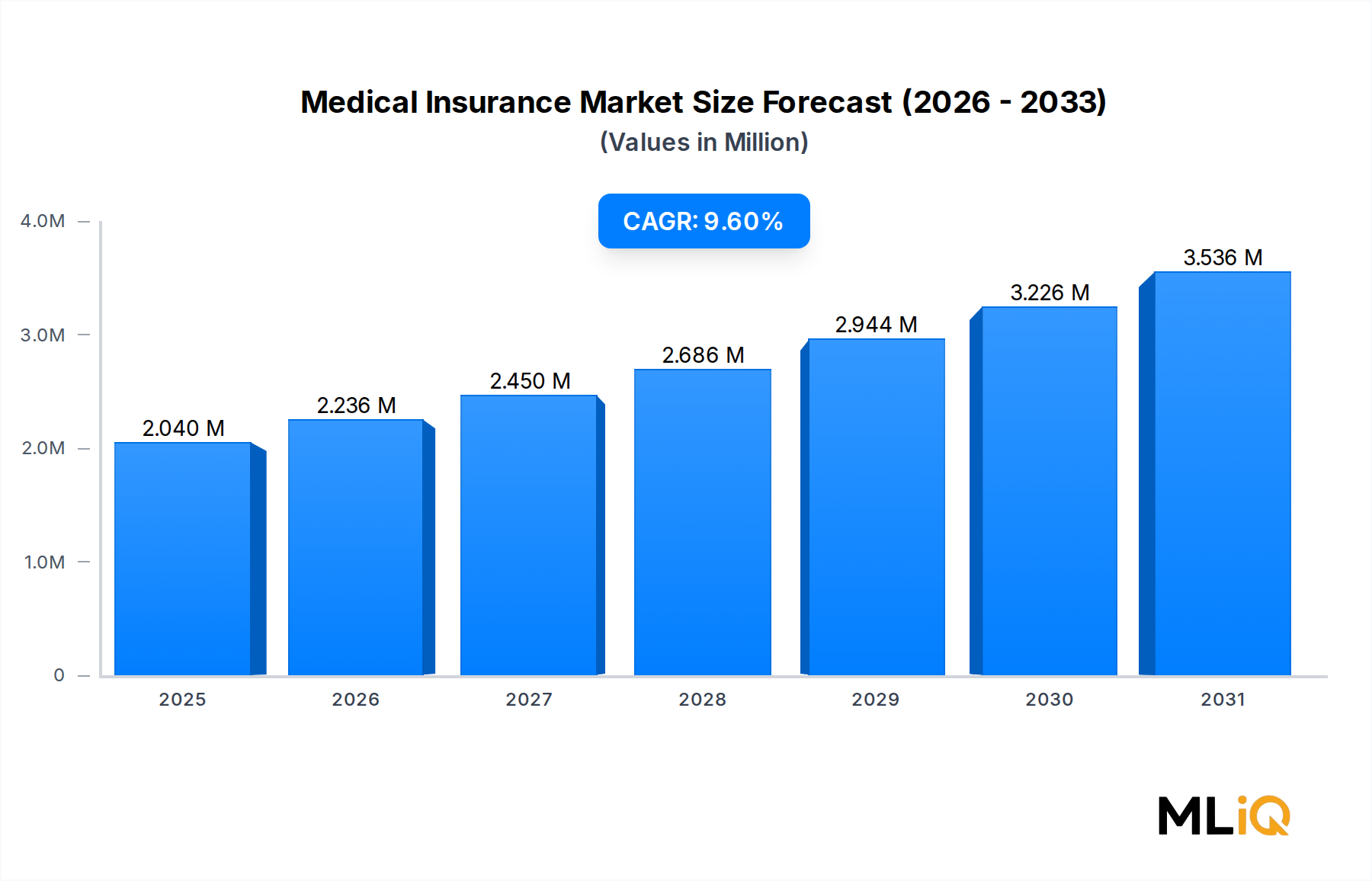

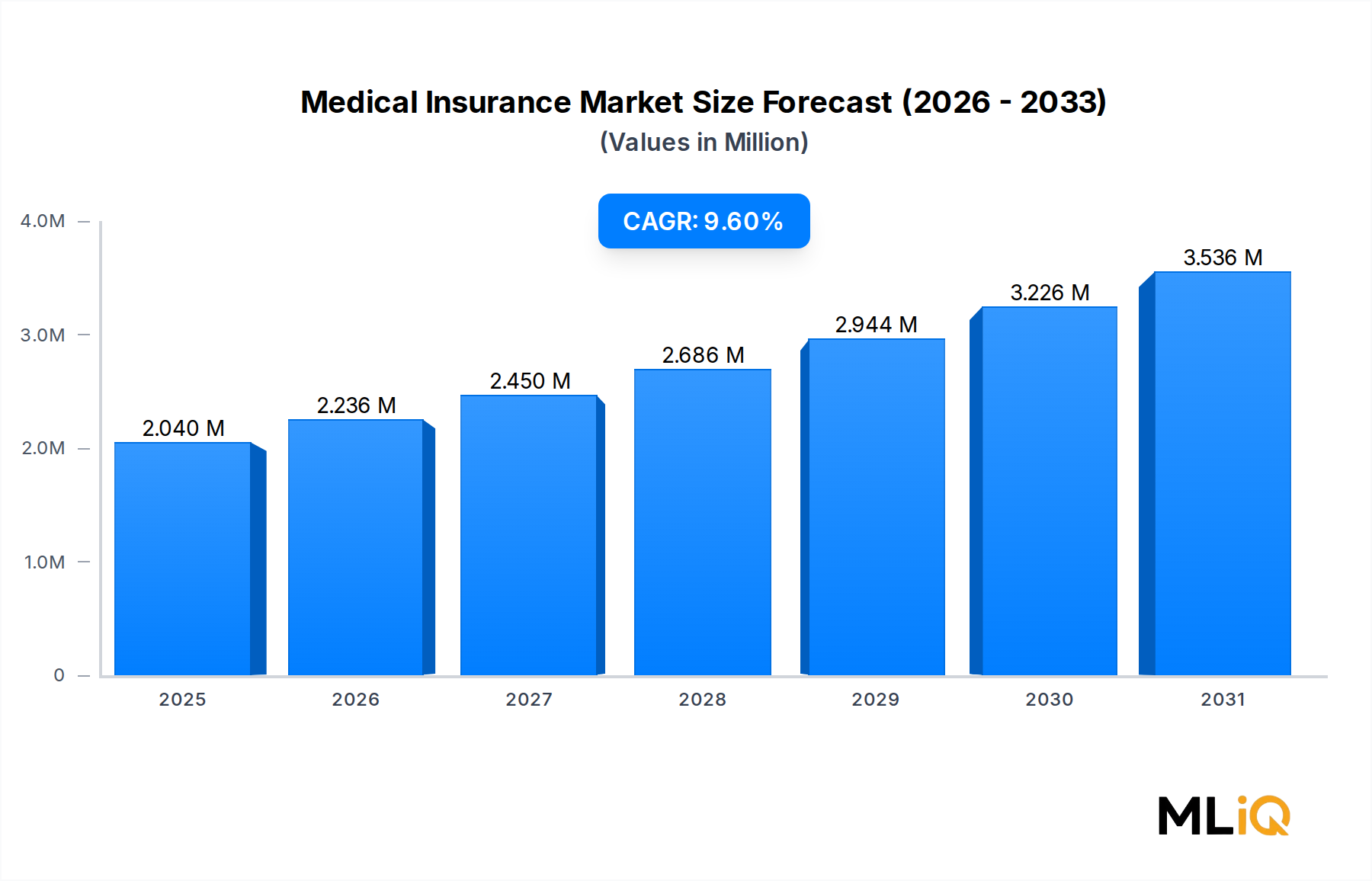

The global Medical Insurance Market is poised for robust expansion, with a current valuation of $2.04 trillion and a projected compound annual growth rate (CAGR) of 9.6% through 2033. This trajectory implies a substantial uplift in absolute market value over the forecast horizon, driven by a confluence of demographic, regulatory, and technological tailwinds.

At the macroeconomic level, aging global populations represent one of the most consequential structural forces shaping the market. The proportion of individuals aged 65 and above is expanding rapidly across North America, Europe, and Asia Pacific, fueling demand for comprehensive inpatient coverage, long-term care riders, and chronic disease management plans. Simultaneously, rising per-capita incomes in emerging economies — particularly across ASEAN nations, India, and Brazil — are enabling broader voluntary insurance uptake among previously uninsured middle-class cohorts.

Healthcare cost inflation remains a pivotal demand amplifier. Average hospital admission costs have escalated sharply in the post-pandemic era, making out-of-pocket payment untenable for most households and accelerating both individual and group plan enrollment. This dynamic is especially pronounced in the United States, where medical inflation continues to outpace general CPI by a significant margin.

Regulatory mandates are also exerting meaningful influence. Governments across the GCC, South Korea, and several European nations have either introduced or expanded compulsory insurance frameworks, creating captive policyholder bases that insulate market volume from economic cyclicality.

Technological innovation is reshaping the value proposition of medical coverage. The rapid integration of artificial intelligence in underwriting, predictive risk modeling, and claims adjudication is compressing operational costs for insurers while enabling more granular, behavior-linked premium structures. Digital health platforms and wearable biometrics are further enabling real-time health monitoring, which is beginning to alter actuarial assumptions and product design at leading carriers.

On the distribution side, e-commerce and digital-first broking channels are gaining significant ground against traditional agent-led models, particularly among policyholders in the 25–34 age demographic. This shift is accelerating competitive differentiation based on user experience, transparency, and turnaround time on cashless claims.

The competitive landscape features a mix of global diversified insurers — including UnitedHealth Group, AXA Group, Allianz SE, and Ping An Insurance — alongside regional champions and emerging insurtech disruptors. Consolidation through M&A remains active, with larger players acquiring digital health platforms and specialty benefit administrators to broaden their service ecosystems.

Looking forward, the Medical Insurance Market is expected to benefit from expanding public-private partnership models, growing penetration in Southeast Asia and Sub-Saharan Africa, and the mainstreaming of value-based care contracting. These factors collectively underpin the 9.6% CAGR forecast and position the market as one of the most strategically compelling segments within the broader BFSI universe.

Among the market's key segmentation dimensions — age group, distribution channel, and claim type — the 50–64 age cohort consistently emerges as the dominant revenue-generating segment within the Medical Insurance Market. This group commands a disproportionately large share of total premium volume due to its elevated healthcare utilization rates, higher propensity for chronic conditions, and relatively greater disposable income compared to younger cohorts.

Individuals in the 50–64 bracket sit at the intersection of peak earning years and escalating health risk, making them both willing and financially capable of investing in comprehensive medical coverage. Unlike the 65 and Above group, which in many markets is partially absorbed into public insurance schemes such as Medicare in the United States or equivalent national programs in Europe, the 50–64 cohort predominantly relies on private medical insurance — either through employer-sponsored group plans or individually underwritten policies.

From an actuarial standpoint, this age group presents a significantly higher claims frequency and severity profile than younger segments. Average annual healthcare expenditures for individuals aged 50–64 are typically two to three times higher than those for the 25–34 bracket. This translates into larger average premium tickets and proportionally greater contribution to insurer gross written premium (GWP) pools.

The segment's dominance is reinforced by several macro trends. First, the global demographic pyramid is broadening at this cohort level as large baby-boomer populations continue to age into this bracket, particularly in North America, Western Europe, and Japan. Second, the prevalence of lifestyle-linked chronic conditions — including type 2 diabetes, cardiovascular disease, and musculoskeletal disorders — is disproportionately concentrated in this age group, increasing policy retention rates and creating demand for specialist referral coverage, prescription drug benefits, and preventive screening riders.

Key players are actively tailoring product portfolios to capture this segment. Humana has developed a suite of pre-Medicare bridge plans specifically targeting individuals in the 50–64 range who are not yet eligible for public coverage. Aetna Inc. has invested in care coordination platforms that integrate with primary care networks to manage complex comorbidities common in this demographic. Bupa has expanded its international health insurance offerings to serve globally mobile professionals in this age bracket.

The distribution dynamics for this segment also differ from younger cohorts. While e-commerce channels are gaining traction across all age groups, the 50–64 segment retains a stronger preference for broker and agent intermediation, particularly when navigating complex plan structures, supplemental benefit riders, and pre-existing condition disclosures. Brokers and agents accounted for the majority of new policy placements within this cohort in mature markets such as the United Kingdom and Germany.

Claim type behavior within the 50–64 segment skews toward cashless claims where hospital network infrastructure supports direct insurer settlement, but reimbursement claims remain significant in markets where cashless infrastructure is still developing, notably across parts of Southeast Asia, the Middle East, and Latin America.

Given these structural characteristics, the 50–64 age group is expected to consolidate its dominant revenue position through 2033, though the 65 and Above segment is projected to post the fastest growth rate as emerging market demographics mature and public coverage gaps widen. Insurers are therefore investing simultaneously in retention tools for the 50–64 cohort and product innovation for the senior segment, creating a dual-track strategic imperative across the competitive landscape.

The Medical Insurance Market is shaped by a set of quantifiable drivers and tangible constraints that collectively determine the pace and direction of premium growth, policy penetration, and product innovation.

Rising Healthcare Expenditure: Global healthcare spending surpassed $10 trillion annually as of recent estimates, with projections indicating continued escalation driven by aging demographics and treatment cost inflation. In the United States alone, national health expenditures represent approximately 18% of GDP, creating systemic pressure that drives individuals and employers toward comprehensive insurance solutions.

Expanding Middle Class in Emerging Markets: Asia Pacific's middle-class population is projected to exceed 3.5 billion individuals by 2030, according to development institution estimates. A significant portion of this cohort represents first-time insurance buyers, creating a structural volume growth opportunity that is already manifesting in accelerating premium growth rates across India, China, and ASEAN nations.

Digital Distribution and Insurtech Penetration: The proliferation of digital broking platforms has materially reduced customer acquisition costs. In markets such as India and China, digital channels now account for a growing share of new individual health insurance enrollments, compressing distribution margins while expanding total addressable market reach.

Regulatory Mandates and Government Partnerships: Compulsory insurance frameworks in markets including Saudi Arabia, the United Arab Emirates, and South Korea have created legislatively mandated demand floors, insulating market volume from economic downturns. These mandates have driven measurable increases in group plan issuance by carriers including AXA Group and Zurich Insurance Company Ltd.

Key Constraints: Premium affordability remains a structural barrier in low-income segments and developing markets where household insurance budgets are constrained. Claims fraud is another material drag, with industry estimates suggesting that fraudulent claims inflate global insurer loss ratios by 5–10% annually. Regulatory complexity across jurisdictions also elevates compliance costs, particularly for multinational carriers operating across both Solvency II-regulated European markets and distinct Asian regulatory regimes. Additionally, adverse selection risk in voluntary individual markets — where sicker individuals disproportionately self-select into plans — continues to challenge pricing accuracy and profitability.

The global Medical Insurance Market features a highly competitive landscape comprising multinational conglomerates, regional specialists, and technology-enabled challengers. The following profiles capture the strategic positioning of leading participants:

UnitedHealth Group: The largest health insurer by revenue globally, UnitedHealth Group operates through its Optum and UnitedHealthcare divisions, integrating insurance underwriting with pharmacy benefits management and data analytics to achieve vertical integration across the healthcare value chain.

The Cigna Group: Cigna operates a global health services platform spanning employer benefits, individual coverage, and behavioral health, with a particularly strong presence in expatriate and international health insurance segments.

Aetna Inc.: A subsidiary of CVS Health, Aetna leverages its parent company's retail pharmacy and MinuteClinic network to offer integrated care pathways, differentiating on care coordination and chronic disease management for its commercially insured population.

Humana, Inc.: Humana is a dominant player in Medicare Advantage plans in the United States, with a growing focus on home health and value-based care models that align insurer incentives with clinical outcomes.

Kaiser Foundation Health Plan, Inc.: Operating as a non-profit integrated delivery system, Kaiser Foundation combines insurance coverage with owned hospital and physician networks, enabling cost containment through care coordination unavailable to indemnity insurers.

AXA Group: AXA maintains one of the largest global footprints in international private medical insurance, with strong positions across Europe, the Middle East, and Asia Pacific, supported by digital transformation investments in automated underwriting.

Allianz SE: Allianz operates across health, life, and property casualty segments with significant market share in Germany and Central Europe, leveraging bancassurance partnerships for distribution scale.

AIA Group: AIA is the leading pan-Asian life and health insurer by new business value, with dominant positions in Hong Kong, Thailand, and China, where rapid middle-class growth is driving health plan enrollment.

Ping An Insurance (Group) Company of China, Ltd.: Ping An is the largest insurer in China by premium volume, operating an ecosystem that integrates health insurance with telemedicine, AI diagnostics, and digital health services through its Good Doctor platform.

Munich Re Group: As a global reinsurer with a significant health reinsurance book, Munich Re supports cedents in pricing complex health risks and provides capacity for catastrophic health claims and pandemic-related exposures.

Aviva: Aviva maintains strong positions in the United Kingdom and Canadian health and group benefits markets, with growing investment in digital wellness programs linked to premium adjustments.

Medibank Private Limited: Australia's largest private health insurer, Medibank competes on integrated health management and has expanded telehealth services as a retention and cost management tool.

Anthem Insurance Companies, Inc.: Operating under the Elevance Health brand, Anthem is a major managed care organization with extensive Medicaid and commercial plan membership across the United States.

MetLife, Inc.: MetLife provides supplemental health and group benefits with a broad employer client base, with growth initiatives targeting voluntary benefit expansion in its worksite distribution model.

Bupa: A globally recognized non-profit health insurer, Bupa operates health insurance, clinics, and hospitals across more than 190 countries, emphasizing integrated care delivery.

Zurich Insurance Company Ltd: Zurich offers corporate and individual health insurance products with particular strength in Swiss domestic markets and global employee benefits programs for multinational employers.

January 2024: UnitedHealth Group announced the full integration of its Optum Health value-based care platform with its UnitedHealthcare insurer operations, targeting $1 billion in administrative cost savings through shared data infrastructure.

March 2024: AIA Group launched a next-generation AI-powered underwriting engine in Hong Kong and Singapore, reducing individual health policy issuance time from 72 hours to under 10 minutes for standard risk profiles.

May 2024: Ping An Insurance completed the expansion of its Good Doctor telemedicine platform to cover over 400 million registered users, enabling real-time claims pre-authorization for outpatient consultations directly within its health insurance app.

July 2024: The European Insurance and Occupational Pensions Authority published updated guidance on climate-linked health risk disclosures, requiring large carriers including Allianz SE and AXA Group to quantify heat-related morbidity exposures in solvency reporting.

September 2024: Humana, Inc. and a consortium of U.S. health systems announced a value-based care contract covering 1.2 million Medicare Advantage beneficiaries, tying insurer payments directly to quality outcomes rather than fee-for-service volumes.

November 2024: Bupa completed the acquisition of a Southeast Asian digital health benefits administrator, expanding its corporate client footprint across Malaysia, Thailand, and the Philippines.

February 2025: Munich Re Group announced a new pandemic risk reinsurance treaty with a syndicate of primary health insurers in Asia Pacific, providing $500 million in excess-of-loss coverage for future infectious disease outbreak scenarios.

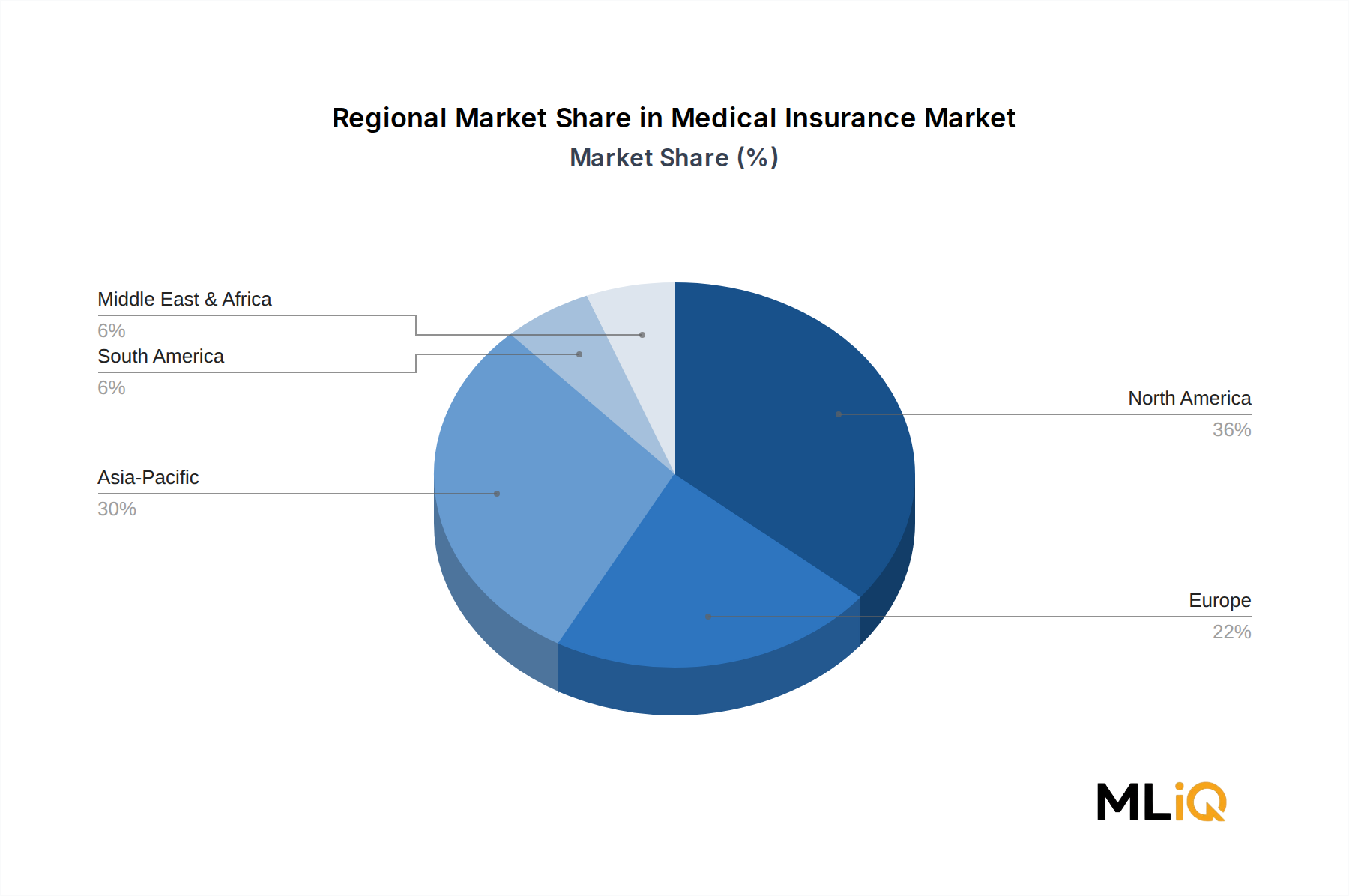

The Medical Insurance Market exhibits significant regional variation in maturity, growth velocity, regulatory structure, and product mix. A comparative analysis across the five principal regions reveals the following dynamics:

North America: North America represents the most mature and highest-revenue region, accounting for approximately 40% of global medical insurance premium volume. The United States is the single largest national market, where employer-sponsored insurance covers the majority of the working-age population and Medicare Advantage enrollment continues to expand among seniors. The regional CAGR is estimated at 6.5–7.5% through 2033, reflecting market saturation offset by rising premium rates and continued shift toward Medicare Advantage and individual marketplace plans under the Affordable Care Act framework. Canada and Mexico contribute smaller but growing premium pools.

Asia Pacific: Asia Pacific is the fastest-growing region in the Medical Insurance Market, with a projected CAGR of 12–14% through 2033, driven by China's expanding commercial health insurance layer above the basic social insurance system, India's Ayushman Bharat expansion, and Southeast Asian market development. The region's vast uninsured population — estimated at several hundred million individuals — represents a structural growth reservoir. Digital-first insurer models are especially prevalent in China and India, where incumbent players face competition from technology-integrated platforms.

Europe: Europe combines mandatory social health systems with supplementary private medical insurance markets. The United Kingdom, Germany, France, and the Benelux countries host the most developed private markets. The regional CAGR is estimated at 5.5–6.5%, with growth concentrated in voluntary dental, optical, and mental health riders. Regulatory compliance costs associated with Solvency II and GDPR create structural barriers that favor established carriers over new entrants.

Middle East and Africa: The GCC subregion has seen compulsory health insurance mandates in Saudi Arabia and the UAE drive rapid premium volume growth, with the broader Middle East and Africa region estimated at a CAGR of 10–11%. South Africa represents the continent's most developed private health market, dominated by medical aid schemes. North Africa and Sub-Saharan Africa remain largely underpenetrated but are attracting investment from global reinsurers and development-focused insurers.

South America: Brazil dominates regional premium volume, supported by a large supplementary health insurance market (planos de saúde) that covers approximately 25% of the population. Argentina and other markets face currency volatility and regulatory uncertainty that constrains insurer investment. The regional CAGR is estimated at 7–8% in USD terms.

While medical insurance is primarily a domestically consumed financial service, cross-border trade flows are material and growing in specific segments — particularly international private medical insurance (IPMI), reinsurance treaties, and digital health benefit administration.

The IPMI segment represents a significant cross-border corridor, with expatriate and globally mobile populations in the GCC, Southeast Asia, and

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.6% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Medical Insurance Market market expansion.

Key companies in the market include The Cigna Group, Aviva, Kaiser Foundation Health Plan, Inc., Medibank Private Limited, Anthem Insurance Companies, Inc., AIA Group, Munich Re Group, MetLife, Inc., Ping An Insurance (Group) Company of China, Ltd., AXA Group, Aetna Inc., Zurich Insurance Company Ltd, Humana, Inc., Bupa, UnitedHealth Group, Allianz SE.

The market segments include Age Group, Distribution Channel, Claim Type.

The market size is estimated to be USD 2.04 trillion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in trillion and volume, measured in .

Yes, the market keyword associated with the report is "Medical Insurance Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Medical Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.