1. What are the major growth drivers for the Event Insurance Market market?

Factors such as are projected to boost the Event Insurance Market market expansion.

+1 2315155523

Event Insurance Market

Event Insurance Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

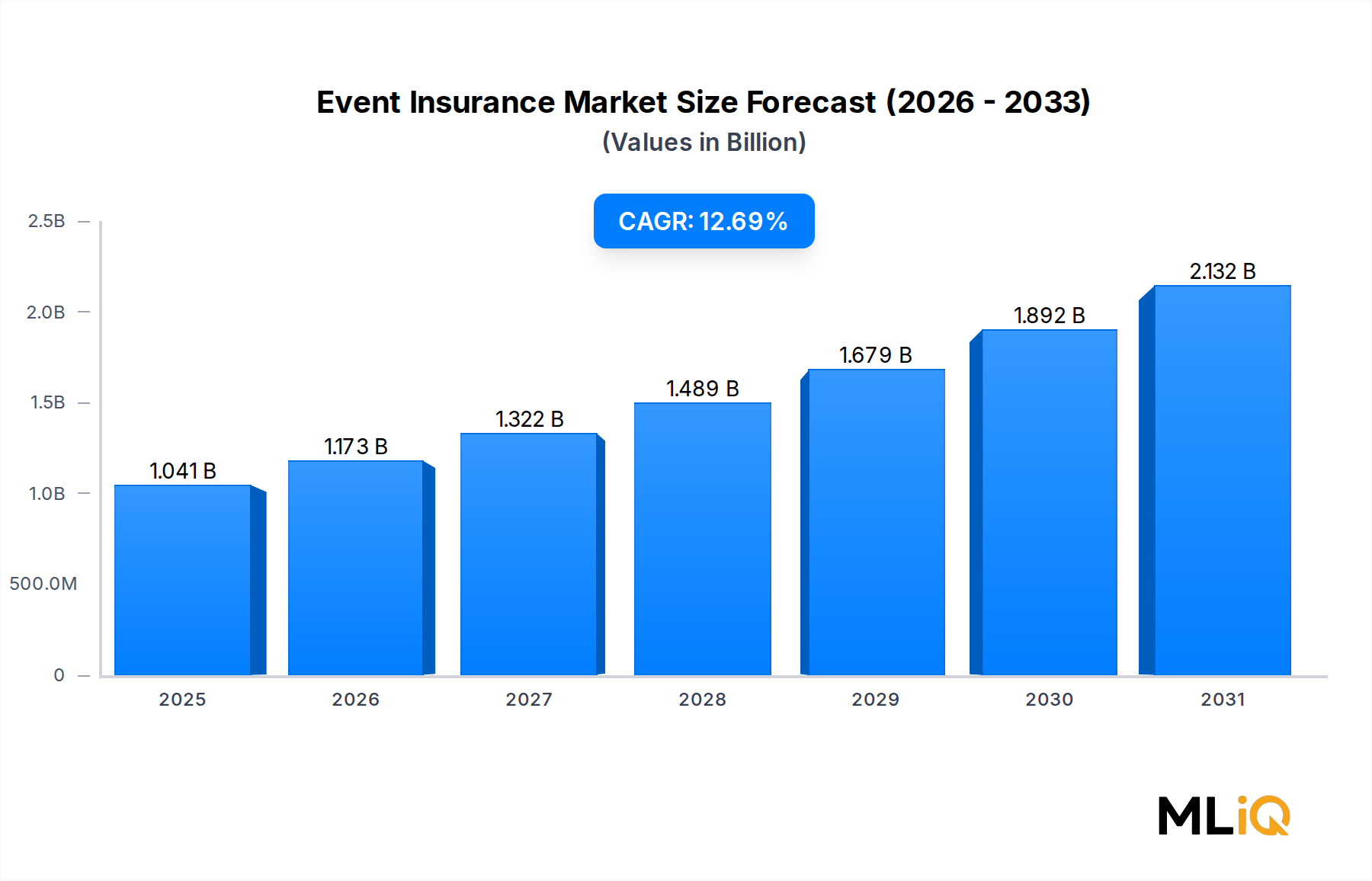

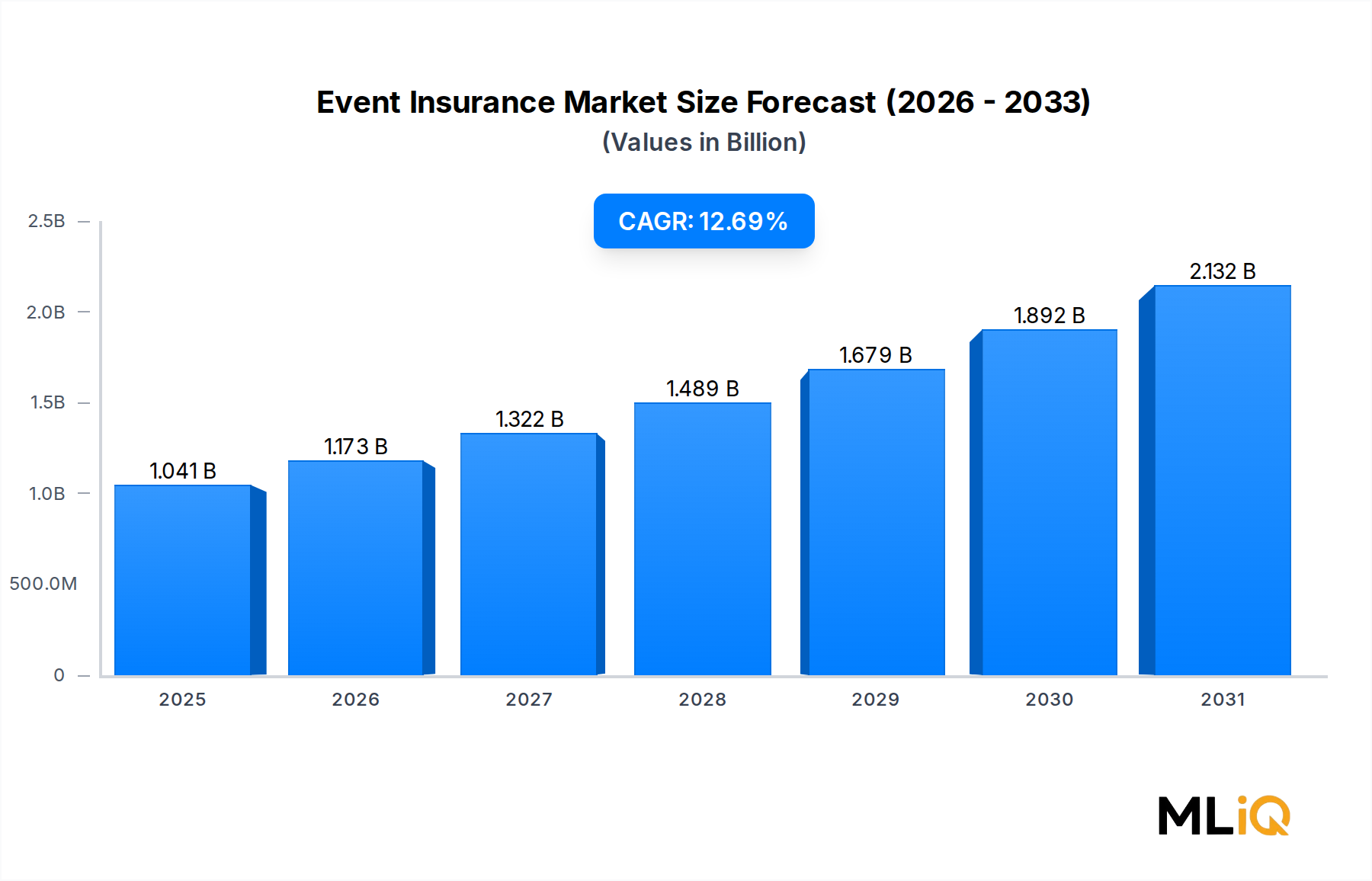

The global Event Insurance Market was valued at $1,040.51 million in the base year and is projected to expand at a compound annual growth rate (CAGR) of 12.7% through the forecast period of 2025 to 2033. This robust growth trajectory reflects a fundamental shift in how individuals, corporations, and public institutions perceive and manage event-related risks. The market encompasses policies that indemnify policyholders against financial losses arising from event cancellation, postponement, abandonment, liability claims, property damage, and bodily injury occurring at or in connection with organized gatherings.

Several macro tailwinds are reinforcing the market's upward momentum. The global live events industry — spanning concerts, sporting competitions, corporate conferences, weddings, festivals, and exhibitions — rebounded sharply following pandemic-era disruptions, generating heightened awareness of catastrophic financial exposure when events are cancelled or curtailed. Insurance penetration, historically low in event management circles, is rising as organizers increasingly mandate coverage as a contractual prerequisite for venue bookings, sponsor agreements, and government permits.

The resurgence of large-scale international events such as the FIFA World Cup, Olympic Games, and global music tours has amplified demand for comprehensive, multi-risk policy structures that bundle cancellation, liability, and weather-related coverage. Corporate enterprises adopting enterprise risk management (ERM) frameworks are systematically procuring event insurance as part of broader operational resilience strategies, contributing to the enterprise end-user segment's growing revenue share.

Technological advancements in underwriting — particularly the integration of predictive analytics, satellite weather data, and AI-driven risk scoring — are enabling insurers to price policies more accurately, reducing adverse selection and expanding addressable market scope. Parametric insurance products, which trigger payouts based on measurable external indices such as rainfall levels or seismic activity, are gaining traction among large event organizers seeking faster claims resolution.

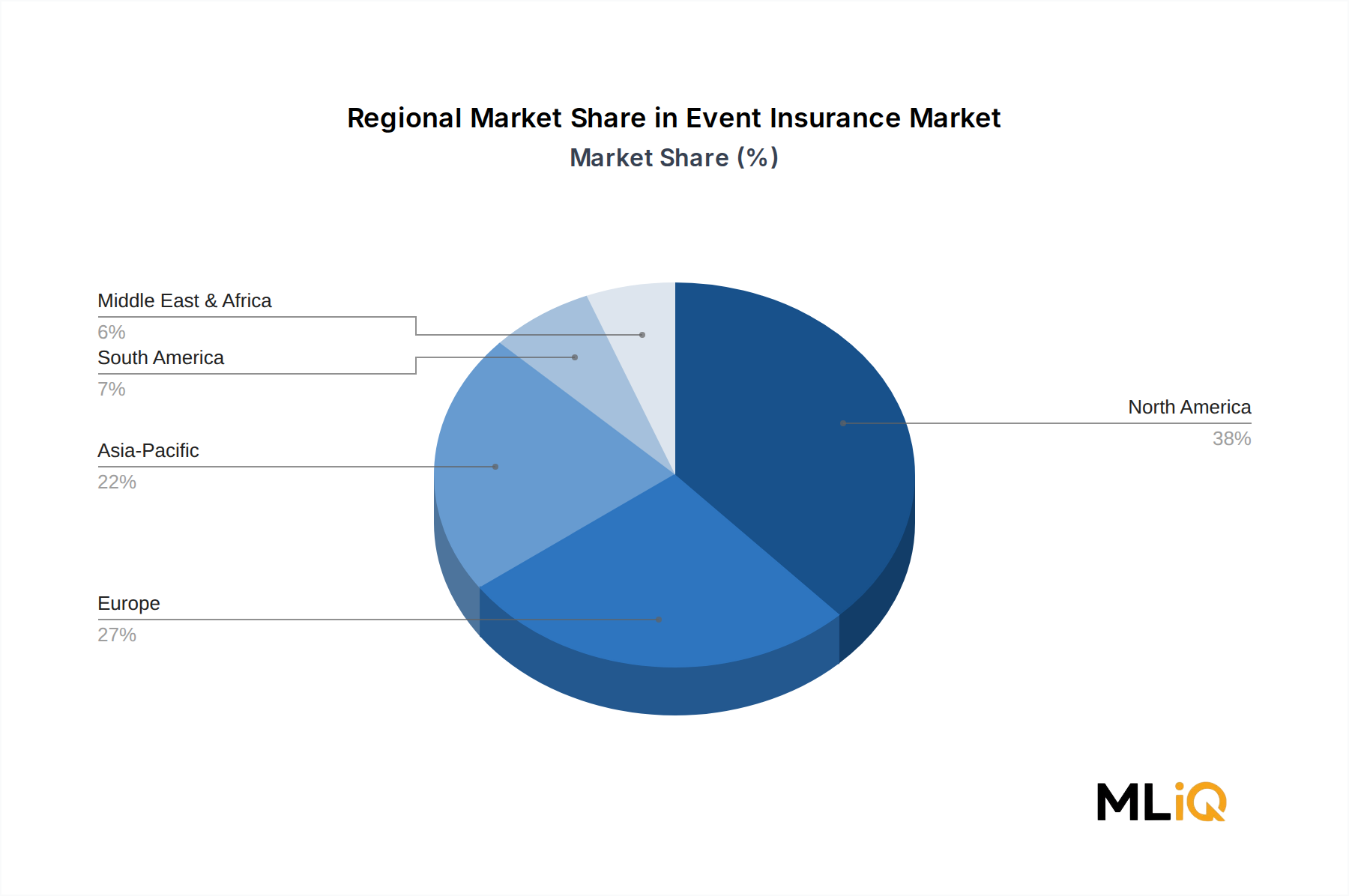

Geographically, North America commands the largest revenue share, underpinned by a mature live events ecosystem, high legal liability awareness, and stringent contractual insurance mandates. The Asia Pacific region is the fastest-growing market, propelled by rapid urbanization, a burgeoning middle class, and a proliferation of entertainment and sporting events in markets such as India, China, and South Korea.

Looking ahead to 2033, the Event Insurance Market is expected to reach a significantly elevated valuation, driven by continued product innovation, expanding distribution through digital insurance platforms, and the normalization of climate-related event disruptions that underscore the necessity of comprehensive coverage. The market's double-digit CAGR positions it as one of the most dynamic sub-segments within the broader specialty insurance landscape.

Within the Event Insurance Market segmented by type, general liability coverage constitutes the single largest revenue-generating category. This dominance is structural rather than cyclical, rooted in the near-universal contractual and regulatory requirements that mandate liability protection for virtually every category of organized event, from intimate private gatherings to large-scale public spectacles.

General liability policies protect event organizers, promoters, and hosts against third-party claims arising from bodily injury or property damage occurring during an event. As litigation culture intensifies across developed economies — particularly in the United States, United Kingdom, and Australia — venue operators and local government authorities increasingly refuse to grant event permits without documented proof of general liability coverage with minimum indemnity thresholds ranging from $1 million to $10 million or more depending on event scale and jurisdiction.

The primacy of general liability within the Event Insurance Market is further reinforced by the breadth of coverage it provides. A single general liability policy can respond to slip-and-fall incidents, crowd crush injuries, third-party property damage caused by event infrastructure or pyrotechnics, and food-related illness claims at catered events. This versatility makes it the foundational layer upon which other event insurance products are stacked, meaning virtually every event insurance buyer purchases some form of general liability protection as a baseline.

Key players commanding significant share within the general liability event insurance sub-segment include The Hartford, Chubb, American International Group, Inc., and Hiscox Ltd. The Hartford leverages its extensive small business distribution network to serve individual event organizers and small enterprises seeking one-time event policies, often through streamlined online underwriting platforms. Chubb, with its globally integrated specialty underwriting capabilities, targets large corporate events, international exhibitions, and high-value sporting events where policy limits and complexity demand sophisticated actuarial modeling.

Hiscox Ltd has carved a particularly strong niche by combining flexible policy structures with digital distribution, offering instant-bind general liability event policies through its online platform. This approach has proven highly effective in capturing the growing segment of micro-event organizers — small wedding planners, community festival organizers, and pop-up market operators — who previously operated without coverage due to friction in the traditional broker-mediated purchasing process.

Professional liability, the second major type segment, addresses claims of negligence or failure to perform professional duties by event management companies, audio-visual contractors, and catering services. While growing, it remains subordinate in revenue terms to general liability, largely because professional liability triggers are less frequent and the buyer universe is narrower, confined primarily to commercial enterprises rather than individual event organizers.

The general liability segment's share is consolidating rather than fragmenting. Insurtech entrants are competing on price and distribution efficiency, but established carriers maintain underwriting authority advantages for large, complex events. The integration of AI-driven risk assessment tools into general liability underwriting is enabling faster policy issuance and more granular pricing differentiation, which is gradually expanding the addressable market by reducing minimum premium thresholds that previously rendered coverage economically unviable for small-scale events.

Overall, general liability's dominance within the Event Insurance Market is expected to persist through 2033, with its absolute revenue base growing in line with or slightly above the overall market CAGR of 12.7%, as expanding legal awareness and contractual mandates continue to drive first-time buyer acquisition.

The Event Insurance Market is propelled by a convergence of structural demand drivers that have materially accelerated following the COVID-19 pandemic, which demonstrated with devastating clarity the financial consequences of uninsured event cancellations. Industry estimates suggest that global event cancellations during 2020 and 2021 generated losses exceeding $30 billion across the entertainment, sports, and corporate events sectors — losses that fell almost entirely on uninsured or underinsured organizers.

The single most significant demand driver is mandated coverage requirements. Venues, sponsors, broadcasters, and municipal authorities are systematically embedding event insurance procurement as a non-negotiable contractual condition. A 2023 survey by the Event Industry Council found that over 74% of event venues in North America now require proof of general liability coverage prior to contract execution, up from 58% in 2019. This mandated demand creates a structurally sticky buyer base insulated from economic cycles.

Climate change is emerging as a secondary but increasingly material driver. The rising frequency and severity of extreme weather events — hurricanes, wildfires, flash floods, and extreme heat episodes — is increasing both the frequency of weather-related event cancellations and the willingness of organizers to pay premiums for weather cancellation riders. Parametric weather insurance adoption has grown at an estimated 18% annually over the past three years, outpacing the broader market.

On the constraints side, the primary restraint is adverse loss experience concentration. The pandemic triggered catastrophic simultaneous claims across virtually the entire event insurance book of business globally, leading numerous carriers to either exit the market entirely, add pandemic exclusions, or dramatically increase premiums. This has created coverage gaps, particularly for biological-risk and government-mandated closure scenarios, that remain contested between insurers and policyholders and may dampen demand from cost-sensitive small event organizers. Premium affordability for micro-events and community gatherings remains a friction point limiting market penetration at the lower end of the buyer spectrum.

The competitive landscape of the Event Insurance Market is characterized by a blend of global insurance conglomerates, specialist underwriters, and emerging insurtech players competing across price, product breadth, and distribution capability.

The Hartford: A leading U.S.-based insurance carrier offering comprehensive event liability products through both broker and direct digital channels, with a particular strength in serving small-to-midsize event organizers through streamlined online application and instant-bind capabilities.

Hiscox Ltd: A specialist insurer with significant underwriting expertise in event liability and cancellation products, known for its flexible policy design and strong digital distribution infrastructure that enables rapid policy issuance for both individual and commercial event buyers.

MARSH LLC: One of the world's largest insurance broking and risk advisory firms, MARSH LLC provides event risk consulting and insurance placement services to large corporate clients, entertainment companies, and international sporting bodies, leveraging its global carrier relationships to structure complex, multi-layered event insurance programs.

GEICO: While primarily a personal lines insurer, GEICO participates in the event insurance segment through partnerships and affiliated underwriting, targeting individual consumers seeking straightforward, low-cost event liability protection.

InEvexco Ltd.: A specialist managing general agent focused exclusively on event insurance, InEvexco Ltd. offers a comprehensive suite of products including cancellation, abandonment, liability, and non-appearance coverage, serving professional event organizers and entertainment industry clients.

Allstate Insurance Company: Allstate Insurance Company leverages its extensive independent agent network and brand recognition to distribute event insurance products across personal and small business segments, competing on accessibility and bundled policy discounts.

American International Group, Inc.: A global insurance leader with deep underwriting expertise in specialty risks, American International Group, Inc. provides large-limit event insurance programs for high-value sporting events, international exhibitions, and major entertainment productions.

Chubb: Chubb is recognized for its high-capacity specialty underwriting and superior claims handling, serving premium event clients including Fortune 500 corporate events, luxury private gatherings, and major international sporting competitions.

Aon plc: As a global professional services firm specializing in risk, Aon plc designs and places bespoke event insurance programs for multinational clients, integrating risk analytics and alternative risk transfer mechanisms to optimize coverage structures.

R.V. Nuccio & Associates Insurance Brokers, Inc.: A specialized boutique brokerage focused on entertainment and event insurance, R.V. Nuccio & Associates Insurance Brokers, Inc. has built a strong market position by serving niche segments including film productions, concerts, and festivals with tailored coverage solutions.

January 2024: Hiscox Ltd announced the expansion of its digital event insurance platform to include parametric weather cancellation riders, enabling instant policy binding with weather-index-linked payouts for outdoor event organizers across the United Kingdom and United States.

March 2024: Aon plc published a comprehensive Event Risk Benchmarking Report documenting a 23% year-over-year increase in event insurance purchasing among Fortune 1000 companies, attributing growth to post-pandemic ERM policy mandates.

June 2024: MARSH LLC launched a dedicated Event Risk Practice Group consolidating its global event insurance placement capabilities, targeting the rapidly expanding Asia Pacific live events sector with localized underwriting partnerships in Singapore, India, and Australia.

August 2024: American International Group, Inc. introduced an AI-powered underwriting platform for large-scale event risks, reducing policy turnaround time from 15 business days to under 48 hours for events with insured values up to $50 million.

October 2024: The Lloyd's of London market released updated event cancellation policy wordings explicitly addressing pandemic and communicable disease exclusion clauses, following two years of industry-wide negotiations aimed at restoring some level of biological risk coverage at commercially viable premium levels.

February 2025: InEvexco Ltd. announced a strategic partnership with a leading insurtech platform to integrate real-time venue risk scoring into its event liability underwriting workflow, improving pricing precision for high-footfall urban events.

April 2025: Chubb expanded its event insurance product suite in the Asia Pacific region, launching dedicated coverage products for K-pop concerts and esports tournaments in South Korea and Japan, reflecting the region's rapidly growing entertainment event economy.

North America dominates the global Event Insurance Market, accounting for an estimated 38% of total market revenue in the base year. The United States is the primary contributor, supported by a deeply embedded live events industry valued at over $1.5 trillion annually, stringent venue liability mandates, and a highly litigious legal environment that drives proactive insurance procurement. Canada and Mexico contribute incrementally, with Canada exhibiting stronger insurance penetration due to regulatory frameworks that align more closely with U.S. standards. The North American market is relatively mature, growing at an estimated regional CAGR of 10.2%, slightly below the global average, as penetration levels are already comparatively high.

Europe represents the second-largest regional market, with the United Kingdom, Germany, and France as primary revenue contributors. The U.K. benefits from a sophisticated specialty insurance ecosystem centered on Lloyd's of London, which has historically been the global hub for complex event cancellation and non-appearance coverage. European regional growth is estimated at a CAGR of 9.8%, constrained somewhat by economic headwinds and relatively mature insurance infrastructure, but supported by growing demand from the continent's robust festival, sporting, and corporate events calendar.

Asia Pacific is the fastest-growing regional market, projected to expand at a CAGR of 17.3% through 2033, significantly outpacing the global average. India and China are the primary growth engines, driven by rapid urbanization, rising disposable incomes, a burgeoning middle class increasingly engaged in premium entertainment and wedding events, and government-sponsored mega-events that require comprehensive insurance programs. South Korea and Japan contribute through their globally significant entertainment industries. Insurance penetration in Asia Pacific remains materially below North American and European levels, creating substantial runway for market expansion.

The Middle East & Africa region is emerging as a notable growth market, propelled by large-scale government-sponsored events including World Expos, major sporting championships, and cultural festivals, particularly in GCC countries such as Saudi Arabia and the UAE. South Africa anchors the African sub-market. Regional CAGR is estimated at 14.1%.

South America, led by Brazil and Argentina, represents the smallest regional market by current revenue share but exhibits a CAGR of approximately 11.5%, supported by the region's vibrant carnival, sporting, and music festival culture.

The Event Insurance Market, as a financial services product, does not have conventional physical supply chain inputs in the manner of manufacturing industries. However, it possesses several critical upstream dependencies that influence product availability, pricing, and market capacity.

The primary upstream input is reinsurance capacity. Event insurance carriers cede a substantial proportion of their exposure to reinsurers — particularly for catastrophic, industry-wide loss scenarios such as pandemic cancellations or major natural disasters. The Reinsurance Market is therefore the most critical upstream supplier for the Event Insurance Market. Post-pandemic, reinsurance capacity for event-related business tightened dramatically, with many global reinsurers either excluding pandemic triggers entirely or pricing pandemic-related capacity at multiples of pre-2020 rates. This reinsurance capacity constraint directly translated into reduced event insurance carrier appetite and elevated retail premiums, particularly for large-scale events.

A second critical input is actuarial and risk data. The accuracy and depth of historical loss data, weather modeling outputs, and venue safety assessments directly determine the quality of underwriting decisions. Data sourcing from meteorological agencies, claims databases, and third-party risk intelligence providers represents an upstream cost that is rising as demand for higher-resolution risk data intensifies. Vendors supplying AI-driven risk analytics tools and satellite weather data feeds are effectively raw material suppliers to the underwriting process.

The Risk Management Software Market has become an increasingly important adjacent input, as event insurers integrate risk assessment software platforms into their underwriting workflows. Price volatility in software licensing and data subscription costs can influence underwriting expense ratios. Additionally, the Insurance Brokerage Market serves as a critical distribution intermediary, and consolidation among brokers can concentrate distribution power and affect premium pricing dynamics.

Historically, the most severe supply chain disruption occurred during 2020–2021, when pandemic-related event cancellations generated simultaneous claims across virtually the entire global event insurance book of business, depleting reinsurer reserves and triggering a hard market cycle characterized by premium increases of 30–60% in some coverage categories.

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.7% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Event Insurance Market market expansion.

Key companies in the market include The Hartford, Hiscox Ltd, MARSH LLC, GEICO, InEvexco Ltd., Allstate Insurance Company, American International Group, Inc., Chubb, Aon plc, R.V. Nuccio & Associates Insurance Brokers, Inc..

The market segments include Type, Coverage, End User.

The market size is estimated to be USD 1040.51 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Event Insurance Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Event Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.