1. What are the major growth drivers for the E-Commerce Buy Now Pay Later Market market?

Factors such as are projected to boost the E-Commerce Buy Now Pay Later Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

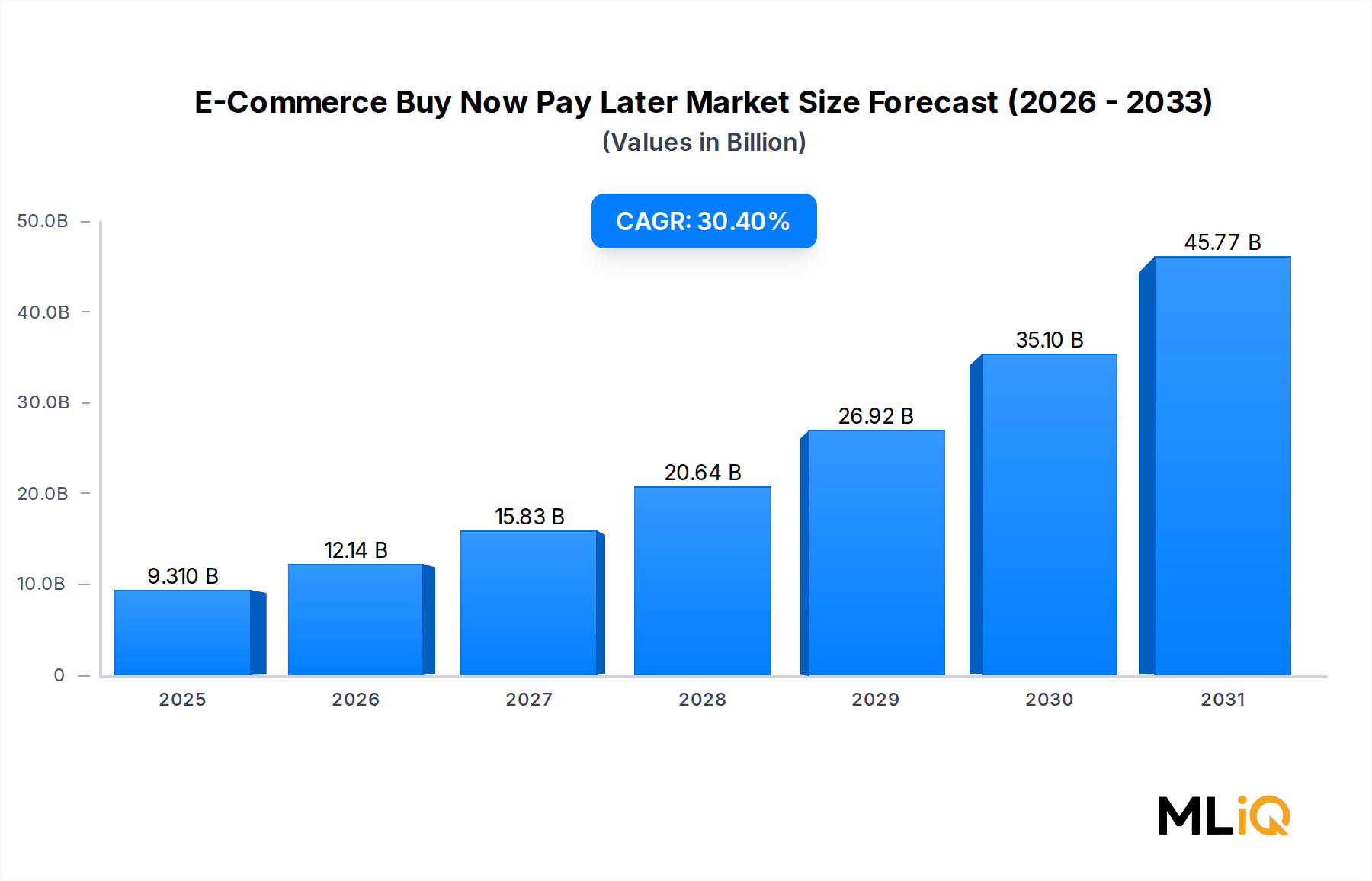

The global E-Commerce Buy Now Pay Later Market is experiencing one of the most accelerated growth trajectories in the broader financial technology sector. Valued at $9.31 billion in the base year, the market is projected to expand at a compound annual growth rate (CAGR) of 30.4% through 2033, driven by a confluence of shifting consumer payment preferences, rising e-commerce penetration, and the rapid democratization of short-term credit among digitally native demographics.

At its core, the E-Commerce Buy Now Pay Later Market represents the intersection of deferred payment mechanisms and online retail, enabling consumers to split purchases into installment payments—often interest-free—at the point of digital checkout. This model has fundamentally disrupted traditional revolving credit products and store-financing schemes by offering frictionless, real-time credit decisioning without the lengthy approval workflows historically associated with consumer lending.

Several macro tailwinds are reinforcing this growth. Global e-commerce penetration continues to rise, with online retail share of total retail sales expanding across all major economies. Concurrently, inflationary pressures in 2022–2024 prompted consumers to seek flexible payment mechanisms that allow budget management without incurring high-interest debt obligations. The millennial and Gen Z cohorts, who form the largest share of digital shoppers, demonstrate a structural preference for deferred payment products over credit cards, creating a sustained demand base that incumbents and challengers alike are racing to capture.

Technological enablers are equally critical. Advances in alternative credit scoring, machine learning-based risk assessment, and real-time bank account verification have significantly reduced underwriting costs for BNPL providers, improving unit economics while expanding the addressable customer base to thin-file and credit-invisible consumers. Integration with major e-commerce platforms and payment orchestration layers has further reduced checkout friction, improving conversion rates for merchant partners.

From a forward-looking perspective, the market is expected to benefit from increasing merchant adoption in high-value categories such as electronics, healthcare, and travel, alongside regulatory clarity in key jurisdictions including the European Union and Australia. The growing Buy Now Pay Later Market for embedded finance tools and the convergence of BNPL with retail banking platforms suggest that the product category will evolve beyond a standalone checkout option into a comprehensive consumer financial health tool. As competition intensifies, differentiation will hinge on data-driven personalization, loyalty integration, and cross-border payment capabilities—making the 2025–2033 forecast period a defining chapter for this market's maturation.

Among all product-type segments analyzed within the E-Commerce Buy Now Pay Later Market, Electronics Appliances—closely grouped with Mobiles and Laptops—represents the dominant revenue-generating category, reflecting the high average order values (AOV) and repeat purchase behavior characteristic of consumer electronics transactions. This segment's supremacy is not incidental; it is structurally reinforced by the price points of consumer electronics, which frequently exceed $300–$1,000 per transaction, making installment payment options both rationally appealing and financially necessary for a significant proportion of online shoppers.

Consumer electronics purchases represent some of the highest-value discretionary spending decisions that households make online. A flagship smartphone priced at $900–$1,200 or a laptop priced between $700 and $1,800 creates a natural alignment with BNPL financing—consumers perceive installment splitting as a means of preserving liquidity while accessing premium products immediately. This behavioral pattern drives disproportionate BNPL adoption in this segment compared to lower-AOV categories.

Mobiles and Laptops as a sub-segment benefit from device replacement cycles that are becoming increasingly frequent, particularly as remote work normalization sustains demand for computing hardware. Smartphone upgrade cycles, historically 24–36 months, are compressing for younger demographics, while laptop refresh rates in both consumer and small business segments have accelerated post-pandemic. BNPL providers have capitalized on this dynamic by establishing direct integrations with major electronics retailers and direct-to-consumer (DTC) technology brands.

Fashion Accessories, the second-largest product segment, exhibits different dynamics. While AOVs are generally lower than electronics, purchase frequency is significantly higher, and brand-conscious consumers—particularly in the 21–40 age bracket—frequently use BNPL products to access premium fashion items, designer accessories, and seasonal collections without immediate full payment. The fashion BNPL sub-segment is also particularly active on social commerce channels, where impulse-driven purchase behavior amplifies BNPL conversion rates.

Key players demonstrating strength across these dominant segments include Affirm Holdings Inc., which has deep integrations with electronics retailers including major direct consumer technology brands, and Klarna Bank, whose European network includes extensive fashion and lifestyle merchant partnerships. Zip co limited has similarly cultivated merchant verticals spanning both electronics and apparel.

The dominance of Electronics Appliances, Mobiles and Laptops within the E-Commerce Buy Now Pay Later Market is further consolidated by merchant incentive structures. Electronics retailers, operating on relatively thin margins, view BNPL integration as a conversion optimization tool rather than merely a payment option—merchants willingly absorb BNPL provider fees (typically 2–8% of transaction value) because BNPL checkout options measurably increase basket sizes and reduce cart abandonment rates by 20–30% compared to credit-only checkout flows.

Looking ahead, this segment's share is expected to remain robust but faces competition from emerging high-AOV verticals including healthcare, home improvement, and travel. Nevertheless, given the enduring consumer appetite for electronics and the continued proliferation of connected devices, Electronics Appliances and Mobiles and Laptops will remain the anchor segment for E-Commerce Buy Now Pay Later Market revenue through 2033.

The E-Commerce Buy Now Pay Later Market is propelled by a set of quantifiable, structurally durable drivers, while simultaneously navigating a set of material constraints that could modulate its growth trajectory over the 2025–2033 forecast horizon.

Driver 1: E-Commerce Volume Growth — Global e-commerce sales surpassed $5.8 trillion in 2023 and are forecast to exceed $8 trillion by 2027. As online transaction volumes expand, the addressable universe for BNPL integration grows proportionally. Every incremental percentage point of e-commerce penetration adds tens of billions of dollars in potential BNPL-eligible transactions.

Driver 2: Credit Card Aversion Among Younger Demographics — Survey data consistently indicates that approximately 40–55% of Gen Z consumers in developed markets do not hold a traditional credit card or actively avoid using one. This demographic, which represents the fastest-growing online shopping cohort, naturally gravitates toward BNPL as a substitute credit mechanism that lacks revolving debt stigma.

Driver 3: Merchant Conversion Economics — A/B testing data from large e-commerce platforms indicates that BNPL availability at checkout reduces cart abandonment by 20–30% and increases average order values by 15–25%. These measurable merchant-side benefits create a self-reinforcing cycle of merchant adoption that expands BNPL market reach without requiring direct consumer marketing spend.

Driver 4: Technological Infrastructure Maturity — The maturation of open banking APIs, instant bank verification, and AI-driven underwriting has reduced BNPL origination costs dramatically. Providers can now make real-time credit decisions in under two seconds, enabling seamless checkout integration that does not introduce friction into the purchase funnel.

Constraint 1: Regulatory Tightening — Consumer credit regulators across the EU, UK, and Australia have introduced or are advancing frameworks that classify BNPL products under consumer credit legislation, imposing affordability assessment requirements and disclosure obligations. Compliance costs increase operational expenditure and may restrict credit availability to subprime segments that currently represent meaningful revenue pools.

Constraint 2: Credit Loss Exposure — Rising consumer debt levels and macroeconomic uncertainty increase default rates on BNPL portfolios. Several providers reported elevated net charge-off rates during 2022–2023, compressing margins and triggering investor concern about portfolio credit quality.

Constraint 3: Competitive Margin Compression — The entry of major payment incumbents including PayPal into the BNPL space introduces scale-based pricing pressure that challenges pure-play providers' ability to maintain merchant discount rates.

The competitive landscape of the E-Commerce Buy Now Pay Later Market is characterized by a mix of pure-play BNPL specialists, fintech challengers, and incumbent payment platforms, each pursuing differentiated positioning across merchant verticals, geographies, and consumer segments.

Zip co limited: An Australia-headquartered BNPL provider with a significant presence across the United States, United Kingdom, and Asia Pacific, Zip co limited has pursued a dual-product strategy offering both short-term pay-in-four products and longer-term installment credit facilities to capture a wider consumer credit spectrum.

Splitit Payments Ltd: Splitit Payments Ltd differentiates itself by enabling consumers to use their existing credit card limits for installment payments, effectively eliminating underwriting risk for the provider and making the product compatible with credit-card-holding demographics who prefer installment structures.

Laybuy Holdings Limited: A New Zealand-originated BNPL provider, Laybuy Holdings Limited operates predominantly across Oceania and the United Kingdom, focusing on fashion, lifestyle, and health and beauty merchant verticals with a six-weekly-installment repayment model.

Sezzle Inc.: Sezzle Inc. targets younger, credit-building consumers in North America and has embedded a credit-building feature into its product, positioning BNPL not merely as a payment tool but as a financial health instrument that helps thin-file consumers establish credit history.

Affirm Holdings Inc.: A leading U.S.-based BNPL provider, Affirm Holdings Inc. has built strategic merchant partnerships with major retailers and direct-to-consumer brands, offering both interest-free and interest-bearing installment products calibrated to higher-AOV purchase categories including electronics and travel.

Klarna Bank: One of the most globally recognized BNPL and shopping platforms, Klarna Bank operates across more than 45 countries and has evolved its product suite beyond BNPL to include a broader consumer shopping application, loyalty rewards, and price comparison tools, deepening merchant and consumer engagement.

Bread Financial: Bread Financial operates within the BNPL and private-label credit card space, targeting retail bank and co-brand credit partnerships that integrate installment financing into existing merchant loyalty ecosystems.

Payright Limited: Payright Limited focuses on higher-value, longer-tenure installment plans in Australia and New Zealand, targeting home improvement, healthcare, and automotive aftermarket merchants where purchase values exceed typical pay-in-four thresholds.

QuickFee Group LLC: QuickFee Group LLC serves the professional services sector, providing installment payment solutions for legal, accounting, and financial advisory firms, differentiating itself by targeting B2B-adjacent BNPL use cases.

PayPal: As a global payments incumbent, PayPal has leveraged its existing merchant and consumer network to deploy BNPL features—including Pay Later and Pay in 4—at scale, benefiting from zero incremental merchant integration costs and access to an established two-sided platform.

January 2024: Klarna Bank filed confidentially for a U.S. initial public offering, signaling renewed investor confidence in the BNPL sector following a period of valuation correction and signaling strategic intent to deepen North American market penetration.

March 2024: The UK Financial Conduct Authority released its formal consultation on BNPL regulation, proposing that BNPL products be brought under the Consumer Credit Act framework, requiring affordability assessments and standardized disclosure language across all BNPL providers operating in the British market.

June 2023: Affirm Holdings Inc. expanded its partnership with Amazon to offer BNPL at checkout for eligible purchases, extending its consumer reach to one of the world's largest e-commerce audiences and significantly broadening its addressable transaction base.

September 2023: The Consumer Financial Protection Bureau (CFPB) in the United States issued interpretive guidance classifying BNPL lenders as credit card issuers under the Truth in Lending Act, triggering significant compliance recalibration among U.S.-based providers.

November 2023: Sezzle Inc. launched its Sezzle Up credit-building product expansion, adding reporting to all three major U.S. credit bureaus to strengthen its positioning as a financial inclusion tool for underbanked and credit-invisible consumers.

February 2024: Zip co limited announced the completion of its U.S. business restructuring, narrowing its focus to the Zip Pay and Zip Money product lines while divesting non-core international assets to improve profitability metrics.

April 2024: PayPal announced expanded BNPL availability across its merchant network in Germany and France, reflecting growing European consumer appetite for installment-based payment options beyond traditional credit instruments.

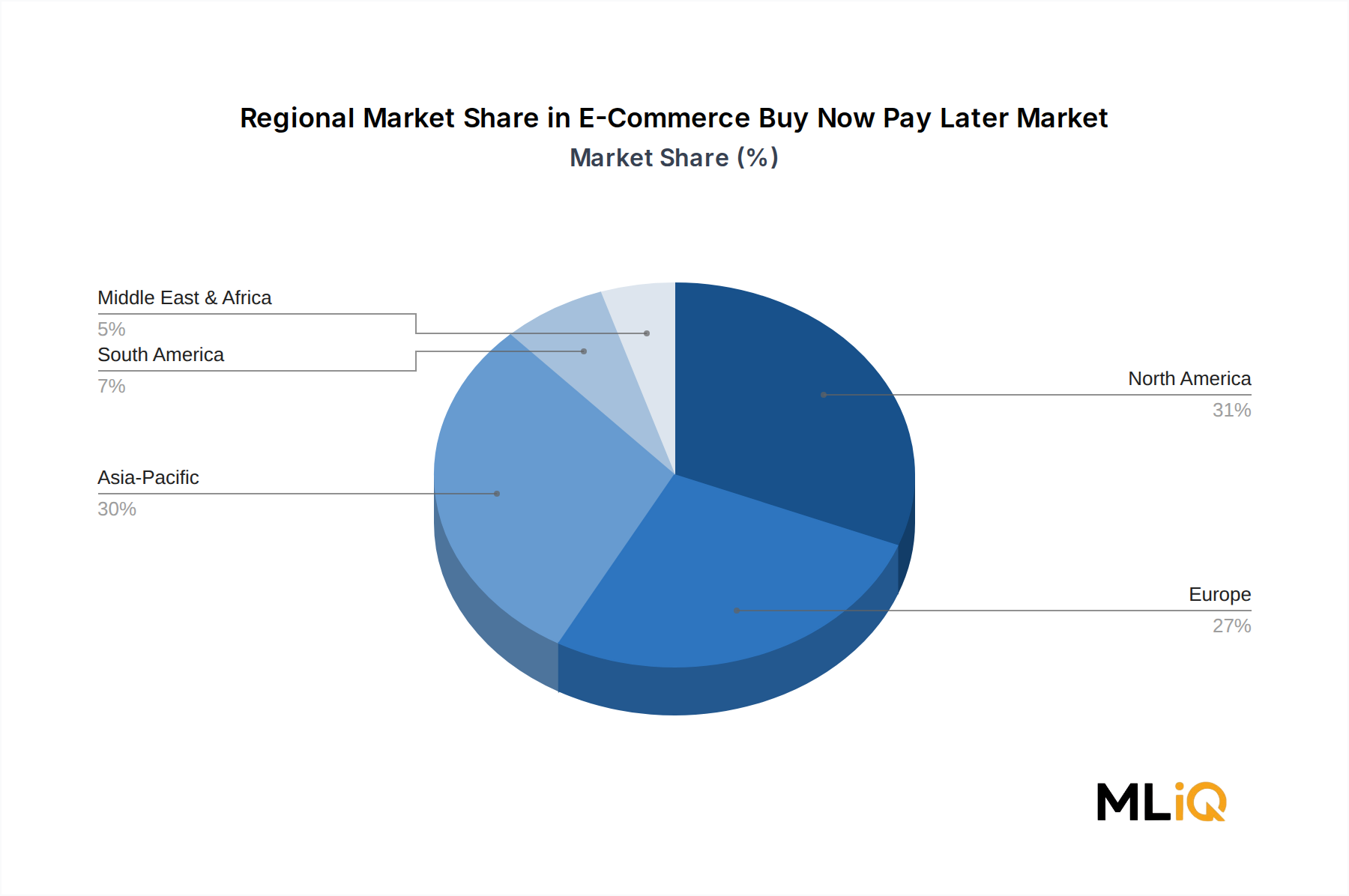

The E-Commerce Buy Now Pay Later Market exhibits pronounced regional heterogeneity in terms of adoption maturity, regulatory environment, and consumer credit culture, making regional analysis essential for accurate market sizing and opportunity assessment.

North America remains the largest single regional market by absolute revenue, accounting for an estimated 35–38% of global BNPL e-commerce transaction volumes. The United States is the primary engine of this dominance, driven by high e-commerce penetration, a large population of credit-averse younger consumers, and the aggressive merchant integration strategies of Affirm Holdings Inc., PayPal, and Sezzle Inc. Canada and Mexico contribute incrementally but represent faster-growth sub-markets given lower current BNPL penetration relative to e-commerce volumes. The North American market is expected to grow at approximately 28–30% CAGR through 2033.

Europe is the most structurally complex region, combining mature BNPL markets—notably Sweden, Germany, and the United Kingdom, where Klarna Bank originated—with nascent markets in Southern and Eastern Europe. Europe's aggregate BNPL e-commerce share is estimated at 28–32% of global revenues, though growth is moderated by regulatory consolidation. Klarna Bank and Laybuy Holdings Limited are dominant across Northern and Western Europe, while Splitit Payments Ltd and PayPal are expanding in Continental markets. European CAGR is projected at 25–27%, slightly below the global average due to regulatory headwinds.

Asia Pacific represents the fastest-growing region for the E-Commerce Buy Now Pay Later Market, with a projected CAGR of 35–40% through 2033. Markets including India, Indonesia, Vietnam, and the Philippines exhibit high unbanked and underbanked population shares, creating fertile ground for BNPL as an alternative credit access mechanism. Australia and New Zealand are comparatively mature, anchored by providers including Zip co limited, Afterpay (owned by Block Inc.), and Payright Limited. China's market operates under distinct regulatory parameters that constrain foreign provider entry.

The Middle East and Africa region is emerging as a high-potential frontier market, with GCC countries—particularly the UAE and Saudi Arabia—seeing rapid BNPL adoption driven by young, digitally active populations, high smartphone penetration, and government-backed digital economy initiatives. Regional CAGR is estimated at 32–36%.

South America, led by Brazil and Argentina, exhibits strong BNPL demand but faces currency volatility and economic instability risks that create provisioning challenges for providers. Brazil's large installment credit culture (parcelamento) provides a cultural precedent for BNPL adoption, though formal BNPL provider penetration remains early-stage.

While the E-Commerce Buy Now Pay Later Market is fundamentally a financial services and technology construct rather than a physical goods market, it possesses distinct upstream dependencies that function analogously to supply chain dynamics in traditional product markets. Understanding these dependencies is critical for assessing operational risk and cost structure evolution.

The primary upstream input for BNPL providers is capital—the cost of funds deployed to finance consumer receivables. BNPL providers either fund receivables from their own balance sheets, securitize portfolios in capital markets, or sell receivables to banking partners. The cost

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 30.4% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the E-Commerce Buy Now Pay Later Market market expansion.

Key companies in the market include Zip co limited, Splitit Payments Ltd, Laybuy Holdings Limited, Sezzle Inc., Affirm Holdings Inc., Klarna Bank, Bread Financial, Payright Limited, QuickFee Group LLC, PayPal.

The market segments include Product Type, Repayment Model, End User, Millennials, Gen X, Baby Boomers.

The market size is estimated to be USD 9.31 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5769, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "E-Commerce Buy Now Pay Later Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the E-Commerce Buy Now Pay Later Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.