1. What are the major growth drivers for the Business Travel Accident Insurance Market market?

Factors such as are projected to boost the Business Travel Accident Insurance Market market expansion.

+1 2315155523

Business Travel Accident Insurance Market

Business Travel Accident Insurance Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

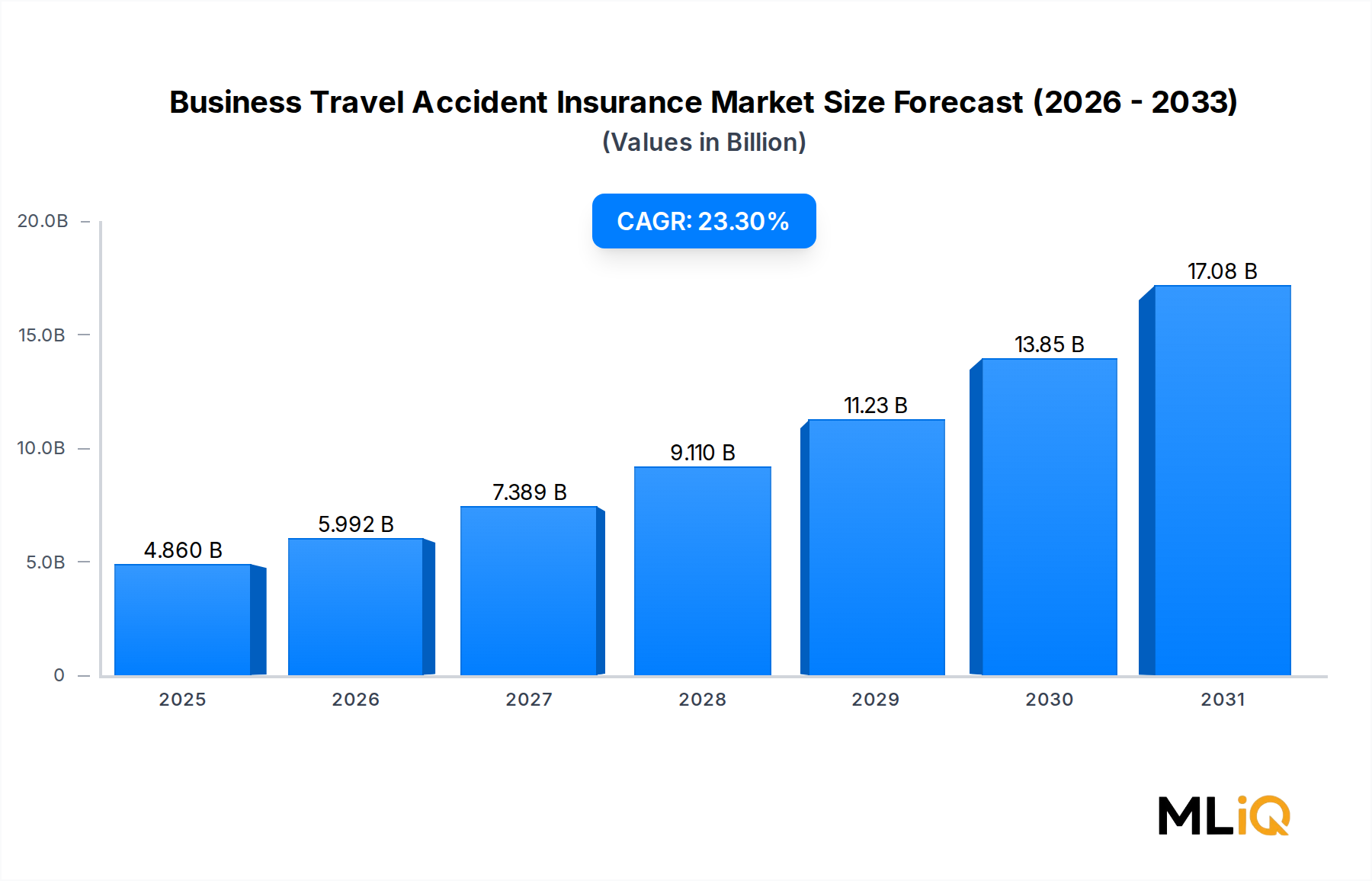

The Business Travel Accident Insurance Market is undergoing a period of accelerated transformation, with the global market valued at $4.86 billion and projected to expand at a compound annual growth rate (CAGR) of 23.3% over the forecast horizon. This extraordinary growth trajectory places the market among the fastest-expanding segments within the broader BFSI (Banking, Financial Services, and Insurance) ecosystem, driven by a confluence of macroeconomic forces, enterprise risk mandates, and post-pandemic resumption of international corporate mobility.

Corporate governance frameworks across North America, Europe, and the Asia Pacific region are increasingly mandating duty-of-care obligations for employers dispatching employees on international assignments. This regulatory push, combined with the organic resurgence of face-to-face business interaction following years of remote-work dominance, has materially elevated demand for comprehensive accident coverage policies tied to work-related travel. Organizations operating across multi-jurisdictional environments are now viewing business travel accident insurance not as a discretionary benefit but as a non-negotiable component of enterprise risk architecture.

Macroeconomic tailwinds reinforcing this demand include the rapid globalization of supply chains, increasing frequency of cross-border mergers and acquisitions requiring executive site visits, and the expansion of multinational corporations into emerging markets across Southeast Asia, Sub-Saharan Africa, and Latin America. These corridors introduce elevated risk profiles — including elevated accident rates, medical infrastructure gaps, and geopolitical volatility — that make structured accident coverage indispensable.

On the supply side, the market is witnessing meaningful product innovation. Insurers are shifting from rigid annual group policies toward dynamic, on-demand coverage models enabled by digital distribution infrastructure and artificial intelligence-powered underwriting engines. The integration of telematics, real-time risk alerts, and embedded insurance within corporate travel booking platforms is reshaping how policies are purchased, managed, and claimed.

The segmentation landscape reveals a clear bifurcation between single-trip and multi-trip products, with multi-trip coverage gaining traction among large enterprises managing frequent traveler populations. Distribution is evolving beyond traditional broker networks toward insurance aggregators and direct digital channels, compressing cost structures and improving accessibility for mid-market enterprises.

Looking forward, the Business Travel Accident Insurance Market is poised to sustain its high-growth trajectory through 2030, supported by rising enterprise travel budgets, regulatory harmonization around employee protection globally, and deepening penetration of insurtech-driven personalization. The convergence of health, accident, and travel assistance into unified policy structures is expected to further expand the addressable market and average premium per policy, creating substantial upside for both incumbent carriers and digitally native challengers.

Within the Business Travel Accident Insurance Market, product type segmentation between single-trip and multi-trip travel insurance reveals a dynamic competitive tension, with multi-trip travel insurance increasingly asserting revenue dominance among large-enterprise and multinational corporate clients. However, single-trip travel insurance remains the volumetric leader in transaction count, particularly among small and mid-sized enterprises (SMEs) and organizations with episodic rather than systematic international travel patterns.

Multi-trip travel insurance policies, also referred to as annual multi-trip plans, are structured to cover an unlimited or capped number of journeys within a defined policy year, typically up to a maximum duration per individual trip ranging from 30 to 90 days. For corporations managing a frequent-traveler workforce — defined broadly as employees undertaking more than 4 international trips annually — multi-trip policies offer significant administrative efficiency and cost optimization relative to purchasing discrete single-trip coverage for each journey.

The dominance of multi-trip coverage in the enterprise segment is reinforced by several structural factors. First, consolidated policy management reduces administrative overhead for corporate HR and finance functions responsible for travel risk compliance. Second, insurers offer volume-based pricing adjustments on multi-trip group policies, making per-employee premium costs substantially lower at scale. Third, the duty-of-care framework prevalent in regulated markets such as the European Union, the United Kingdom, and Australia mandates consistent coverage across all work-related travel, making the predictability of multi-trip policies operationally preferable.

Key players competing aggressively for multi-trip corporate mandates include Chubb Limited, AXA SA, American International Group Inc., and Zurich American Insurance Company. These carriers leverage proprietary global assistance networks, 24/7 emergency response infrastructure, and integrated travel risk intelligence platforms to differentiate their multi-trip offerings from commodity alternatives. Chubb, in particular, has invested heavily in its global accident and health division, building out customized multi-trip solutions for Fortune 500 clients with complex jurisdictional requirements.

Single-trip travel insurance, while lower in per-policy premium value, commands strategic importance as a gateway product and as the primary vehicle for serving the large and fragmented SME segment. Players such as VisitorsCoverage Inc. and insurance aggregator platforms have built significant distribution scale around single-trip products by embedding them within corporate booking tools, expense management software, and airline booking portals. The frictionless, point-of-need availability of single-trip coverage makes it particularly well-suited to the digital-first buying behavior of millennial and Gen-Z business travelers who expect instant, mobile-accessible policy issuance.

The segment share dynamics are gradually shifting. As insurtech infrastructure matures and large insurers develop more flexible modular policy architectures, the distinction between single-trip and multi-trip products is blurring. Emerging "on-demand" or "per-diem" coverage models allow employees to activate and deactivate accident coverage at the trip level within an overarching corporate program, combining the flexibility of single-trip with the administrative coherence of multi-trip frameworks. This hybrid model is expected to capture a growing share of the market through 2028, reshaping segment revenue allocation and compelling traditional carriers to accelerate product modernization.

The consolidation of multi-trip dominance is also being reinforced by the international application segment, where persistent cross-border travel — particularly in corridors such as North America to Europe, intra-Asia Pacific, and the emerging Middle East to South Asia route — generates recurring, high-value claims activity that multi-trip structures are better equipped to handle on both the coverage and administrative dimensions.

The Business Travel Accident Insurance Market is propelled by a set of well-defined, quantifiable drivers while simultaneously facing structural constraints that insurers and policymakers must navigate with precision.

Primary Driver — Duty-of-Care Regulatory Mandates: Corporate duty-of-care legislation has expanded materially across the G20 economies, with frameworks such as the UK Corporate Manslaughter Act, EU Directive 2019/1937 on whistleblower protection (which implicitly extends to employee safety disclosures), and Australia's Model Work Health and Safety Act compelling organizations to demonstrate active protection mechanisms for traveling employees. Non-compliance penalties in regulated jurisdictions can reach $10 million or more per incident, creating a powerful compliance incentive for purchasing comprehensive accident insurance.

Secondary Driver — Business Travel Volume Recovery: Global corporate travel spending reached approximately $1.4 trillion in 2024, recovering to pre-pandemic levels per industry benchmarks. The International Air Transport Association (IATA) projected business travel seat demand growth of 7–9% year-over-year through 2025, directly expanding the insurable population base.

Tertiary Driver — Rising Medical Cost Inflation: Healthcare cost inflation in key business travel destinations, particularly the United States (averaging 6–8% annual medical cost increases), Southeast Asia, and the Middle East, has increased the financial exposure of uninsured or underinsured business travelers, prompting corporate procurement teams to upgrade accident coverage limits.

Primary Constraint — SME Awareness Gap: A significant proportion of SMEs — particularly in emerging markets — remain unaware of or underinvested in formal business travel accident insurance, limiting market penetration below its theoretical maximum. Bridging this gap requires substantial distribution investment.

Secondary Constraint — Claims Complexity in Multi-Jurisdictional Environments: Cross-border claims adjudication remains operationally complex, with differing legal frameworks, healthcare provider networks, and currency risk introducing delays and cost overruns that suppress insurer margins and occasionally deter purchasers who have experienced poor claims experiences.

The competitive landscape of the Business Travel Accident Insurance Market is dominated by a combination of global insurance conglomerates, specialized accident and health carriers, and digitally native insurtech challengers. Below is a structured profile of the key participants:

MetLife Services and Solutions, LLC.: MetLife leverages its extensive global benefits administration infrastructure to offer integrated group accident and travel coverage, targeting multinational corporations seeking consolidated employee benefits programs across jurisdictions.

Chubb Limited: Chubb is recognized as a market leader in global accident and health insurance, deploying a broad portfolio of business travel accident solutions backed by one of the industry's most extensive global assistance networks and a strong direct enterprise sales force.

Arch Capital Group Ltd.: Arch Capital competes through its specialty insurance division, emphasizing flexible underwriting for high-risk industry verticals such as energy, construction, and mining where business travel accident exposure is elevated.

VisitorsCoverage Inc.: VisitorsCoverage operates a digital-first insurance marketplace that aggregates and distributes travel accident policies from multiple carriers, with a strong focus on small business and individual business traveler segments through a self-service online platform.

Tata AIG General Insurance Company Limited: Tata AIG holds a commanding position in the high-growth Indian corporate travel insurance segment, combining local market expertise with AIG's global underwriting capabilities to serve both domestic and international business travel corridors originating from South Asia.

American International Group, Inc.: AIG maintains a globally diversified accident and health book, with proprietary risk management services and dedicated multinational client programs that integrate travel accident coverage with broader enterprise risk management frameworks.

AXA SA: AXA competes aggressively across both group and individual business travel accident segments, supported by its global assistance subsidiary AXA Partners, which provides real-time emergency medical evacuation, repatriation, and crisis response services that differentiate its offerings.

The Hartford: The Hartford focuses primarily on the North American commercial market, offering business travel accident coverage as part of integrated employer benefit packages with strong integration into its group life and disability insurance distribution channels.

Starr International Company, Inc.: Starr International specializes in complex, high-value accident coverage for corporate executives and high-risk travelers, offering bespoke policy structures with elevated coverage limits and specialized war risk and terrorism endorsements.

Zurich American Insurance Company: Zurich targets multinational corporate clients with its Global Programs framework, enabling consistent business travel accident coverage across more than 215 countries and territories through a coordinated local-global policy architecture.

January 2023: AXA SA announced the expansion of its AXA Partners global assistance network to include enhanced mental health support services for business travelers, responding to growing corporate demand for holistic traveler wellbeing coverage beyond physical accident benefits.

March 2023: Chubb Limited launched a refreshed suite of multinational business travel accident programs incorporating real-time geopolitical risk scoring, enabling dynamic premium adjustment based on destination risk profiles at the time of policy activation.

July 2023: Tata AIG General Insurance Company Limited partnered with a leading Indian corporate travel management company to embed business travel accident insurance directly within the corporate booking workflow, achieving significant growth in policy issuance volume.

November 2023: The Hartford introduced an AI-powered claims triage system for its business travel accident book, reducing average claims processing time by an estimated 40% and improving claimant satisfaction scores materially.

February 2024: American International Group, Inc. completed the acquisition of a specialist travel risk intelligence platform, integrating real-time security alerting capabilities into its enterprise business travel accident policy management portal.

May 2024: Zurich American Insurance Company announced a strategic alliance with a global travel management company to co-develop embedded insurance solutions targeting mid-market enterprises, expanding distribution reach beyond traditional broker channels.

September 2024: MetLife Services and Solutions, LLC. unveiled an updated global benefits platform with enhanced business travel accident module capabilities, including parametric accident payout triggers for select high-frequency travel corridors.

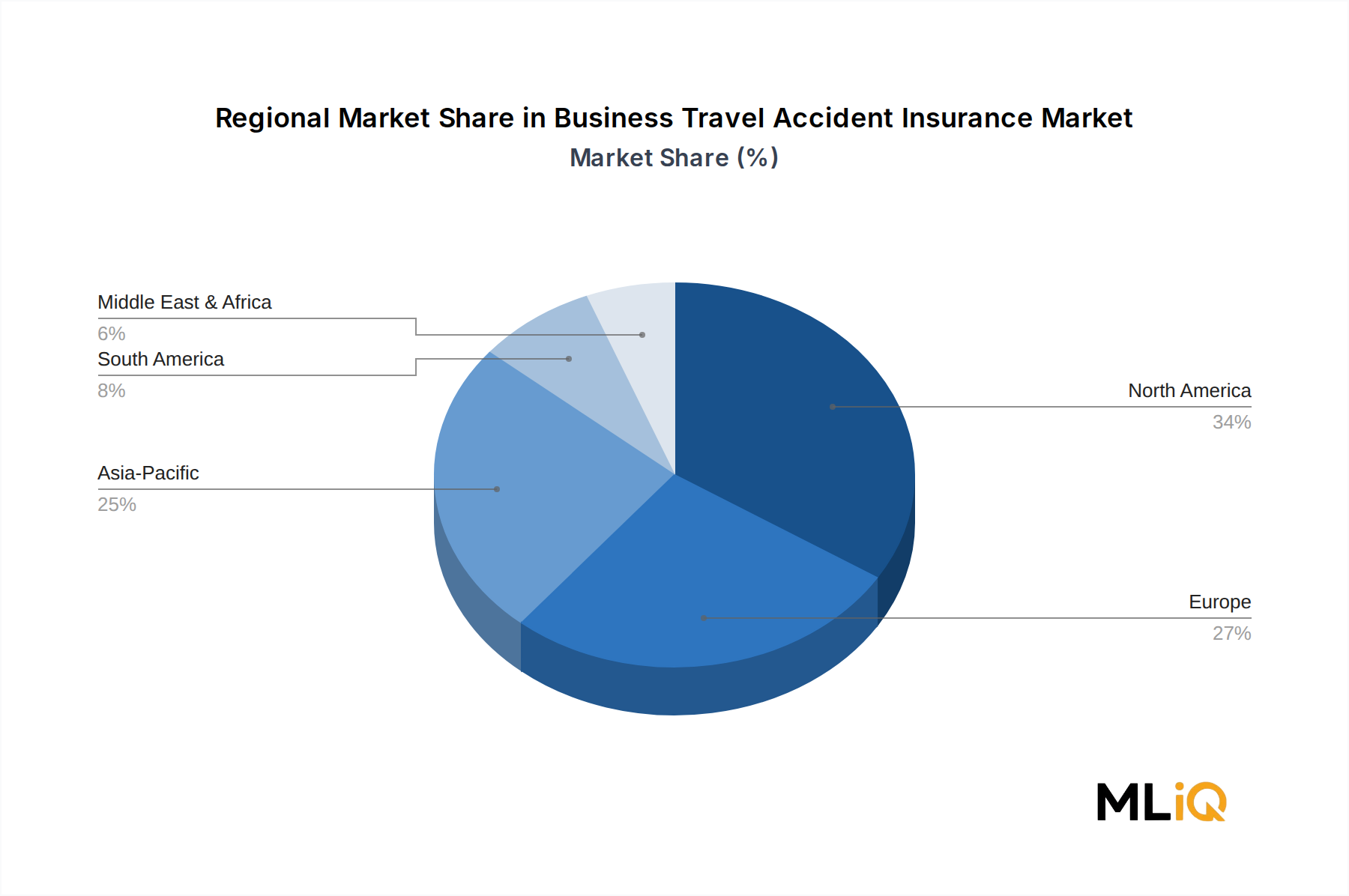

The Business Travel Accident Insurance Market exhibits distinct regional growth profiles shaped by varying regulatory environments, corporate travel volumes, insurance penetration rates, and economic development trajectories.

North America represents the most mature regional market, accounting for an estimated 34–36% of global revenue share. The United States anchors this dominance, supported by deep insurance market infrastructure, high per-employee coverage limits mandated by corporate governance standards, and the sheer volume of outbound business travel — the U.S. alone generates over 30 million annual business travel trips internationally. Canada and Mexico contribute incrementally, with Mexico's growing manufacturing and nearshoring activity creating new demand corridors. Regional CAGR for North America is estimated at approximately 18–19%, reflecting maturity relative to global averages.

Asia Pacific is the fastest-growing regional market, with a projected CAGR exceeding 27–28% through the forecast period. China, India, Japan, and the ASEAN bloc are the primary growth engines. India's rapidly internationalizing corporate sector, combined with government-backed initiatives promoting global trade engagement, has created a surge in business travel accident insurance demand. China's outbound corporate travel recovery post-2022 restrictions and Japan's sustained high-frequency intra-Asia business travel further amplify regional momentum. Insurance penetration in Asia Pacific remains below global averages, representing a substantial untapped opportunity.

Europe is characterized by regulatory sophistication and high baseline penetration, with the United Kingdom, Germany, and France leading in premium volume. EU duty-of-care directives and GDPR-adjacent data governance frameworks for traveler information management have elevated compliance-driven purchasing. European regional CAGR is estimated at 20–22%, sustained by demand from SMEs newly engaging with formal travel risk management.

Middle East and Africa represent an emerging high-potential region, with GCC-based multinationals and the rapid expansion of intra-African business corridors driving demand growth. South Africa serves as a regional hub for sub-Saharan Africa corporate travel insurance distribution. Regional CAGR is projected at 24–25%, above the global average, though from a comparatively smaller absolute base.

South America, led by Brazil and Argentina, is experiencing renewed interest in corporate travel accident coverage as regional economic stabilization encourages cross-border business activity, though currency volatility and distribution infrastructure gaps temper penetration rates.

Investment activity within and adjacent to the Business Travel Accident Insurance Market has accelerated meaningfully over the 2022–2024 period, with capital flowing across three primary channels: strategic acquisitions by incumbent insurers, venture and growth equity funding for insurtech challengers, and partnership-based co-investment in distribution infrastructure.

On the M&A front, large carriers including American International Group, Inc. and AXA SA have executed targeted acquisitions of travel risk intelligence and digital claims processing platforms, reflecting a strategic imperative to vertically integrate data and technology capabilities into their business travel accident offerings. These transactions are typically valued in the range of $50 million to $300 million, depending on the maturity and revenue scale of the target.

The InsurTech Market has been a primary recipient of venture capital directed at disrupting traditional business travel accident distribution and underwriting. Startups developing embedded insurance APIs, parametric coverage engines, and AI-driven risk assessment tools have collectively attracted several hundred million dollars in funding across Series A through Series C rounds during this period. Investors including specialized insurtech venture funds and the corporate venture arms of major carriers are the dominant funding sources.

The Digital Insurance Platform Market has attracted particular strategic capital, as aggregator and marketplace platforms serving the corporate travel segment offer scalable distribution economics that legacy broker networks cannot replicate. VisitorsCoverage Inc. and comparable platforms have benefited from both organic growth investment and third-party capital as insurers seek distribution partnerships to reach SME and mid-market segments cost-effectively.

The sub-segment attracting the greatest concentration of capital is on-demand and embedded business travel accident insurance, where the intersection of travel booking technology and real-time policy issuance creates a high-frequency, high-margin revenue model. Strategic partnerships between carriers and travel management companies — exemplified by the Zurich-TMC alliance announced in May 2024 — represent a capital-light alternative to outright M&A that is

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 23.3% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Business Travel Accident Insurance Market market expansion.

Key companies in the market include MetLife Services and Solutions, LLC., Chubb Limited, Arch Capital Group Ltd., VisitorsCoverage Inc., Tata AIG General Insurance Company Limited, American International Group, Inc., AXA SA, The Hartford, Starr International Company, Inc., Zurich American Insurance Company.

The market segments include Type, Application, Distribution Channel.

The market size is estimated to be USD 4.86 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4335, and USD 7261 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Business Travel Accident Insurance Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Business Travel Accident Insurance Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.