Open-Loop Segment Dominance in the Prepaid Credit Card Market

Within the Prepaid Credit Card Market, the open-loop segment stands as the unequivocal dominant revenue generator, commanding a disproportionate share of total market value relative to its closed-loop counterpart. Open-loop prepaid cards, which operate on major payment networks such as Visa, Mastercard, and American Express, are accepted at any merchant that accepts those network-branded cards — a characteristic that gives them near-universal utility and makes them fundamentally more attractive to both issuers and end consumers.

The structural advantage of open-loop cards over closed-loop variants originates in their versatility. Whereas closed-loop cards are restricted to specific merchant networks, retail chains, or branded ecosystems, open-loop cards function as de facto debit alternatives with the additional flexibility of anonymized transactions and preloaded funding. This positions them favorably across a wide spectrum of applications — from government disbursement programs and payroll cards to travel prepaid solutions and corporate expense management platforms.

From a revenue composition standpoint, open-loop prepaid cards generate income through multiple streams: interchange fees charged to merchants at point of sale, monthly maintenance fees, ATM withdrawal charges, reload fees, and foreign exchange conversion margins on international transactions. This multi-stream fee architecture creates a more robust and diversified revenue model compared to closed-loop alternatives, which typically rely on a single-merchant relationship and carry limited interchange rights.

Key players within the open-loop prepaid segment include Visa Inc, Mastercard Incorporated, and The American Express Company at the network level, while Capital One Financial Corporation, Citibank, and Wells Fargo operate as significant card issuers leveraging these network rails. H&R Block Inc. has carved out a distinct niche by offering open-loop prepaid cards as part of integrated tax refund disbursement services, effectively bundling the financial product with a high-frequency annual service event that drives mass adoption among underbanked segments.

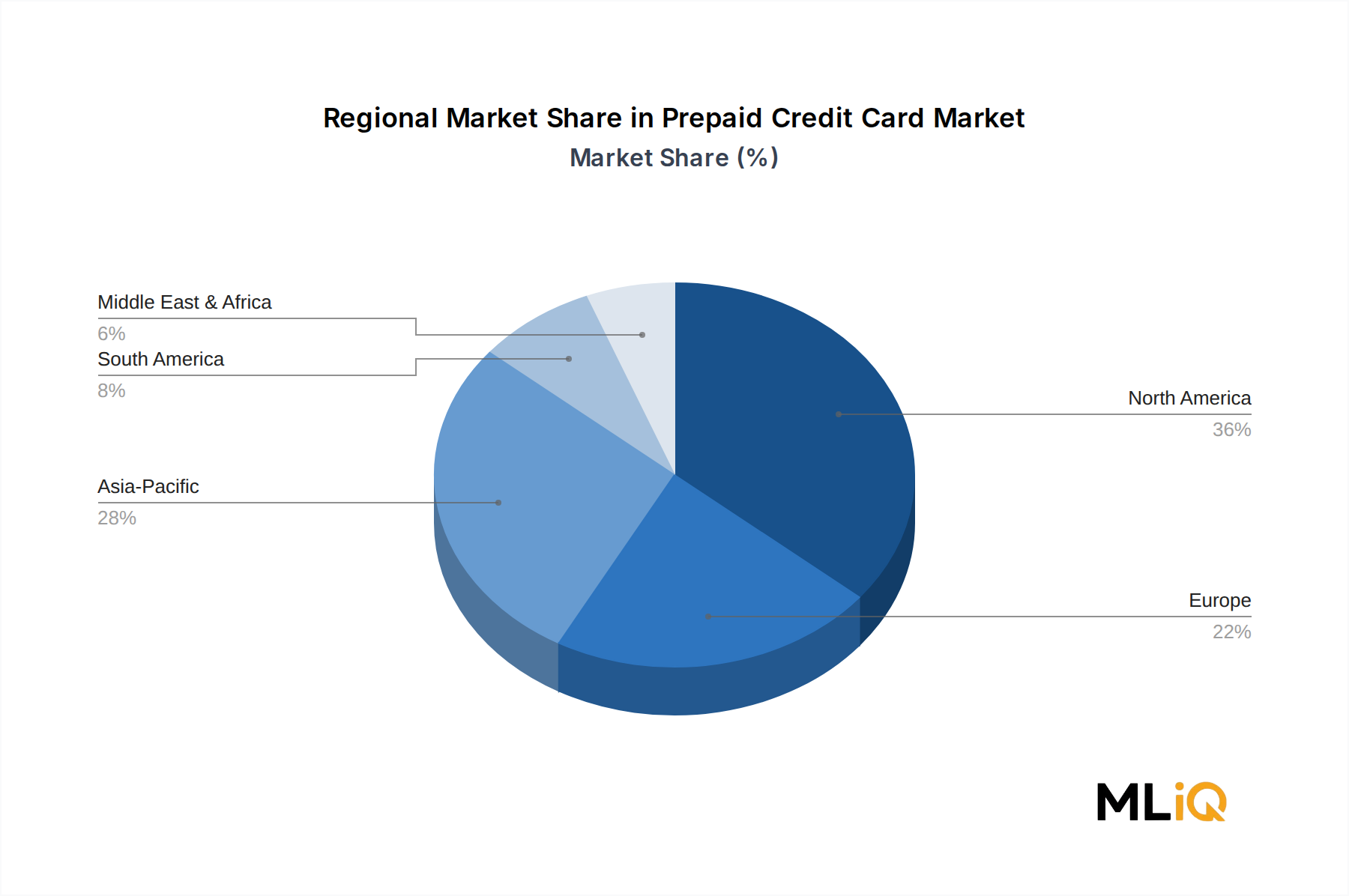

The dominance of the open-loop segment is further reinforced by government adoption. Across the United States, Canada, the United Kingdom, and large swaths of Asia Pacific, public sector agencies have adopted open-loop prepaid infrastructure to distribute social welfare payments, unemployment benefits, and disaster relief funds. These G2P programs introduce millions of new cardholders into the prepaid ecosystem annually, creating a self-reinforcing cycle of adoption and merchant acceptance expansion.

The segment's share is not merely stable — it is actively expanding. As financial institutions and fintech companies develop more sophisticated open-loop prepaid offerings embedded with digital account management, real-time spending notifications, and integration with the Digital Payments Market, the value proposition widens further. Closed-loop products, while retaining relevance in gifting and specific retail loyalty contexts, are increasingly being outpaced in growth rate by open-loop alternatives, which benefit from network effects, regulatory tailwinds, and the global push toward interoperable digital payment infrastructure.

Investment in open-loop prepaid technology is also being catalyzed by the maturation of the Smart Card Market, which supplies the chip-and-PIN and contactless-enabled card substrates that are now standard across most open-loop prepaid product lines. As EMV chip adoption reaches near-universal levels in developed markets, open-loop prepaid cards are completing their security and acceptance parity with traditional credit and debit cards, further removing barriers to mainstream adoption.