1. What are the major growth drivers for the Europe Travel Retail Market market?

Factors such as are projected to boost the Europe Travel Retail Market market expansion.

Europe Travel Retail Market

Europe Travel Retail Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

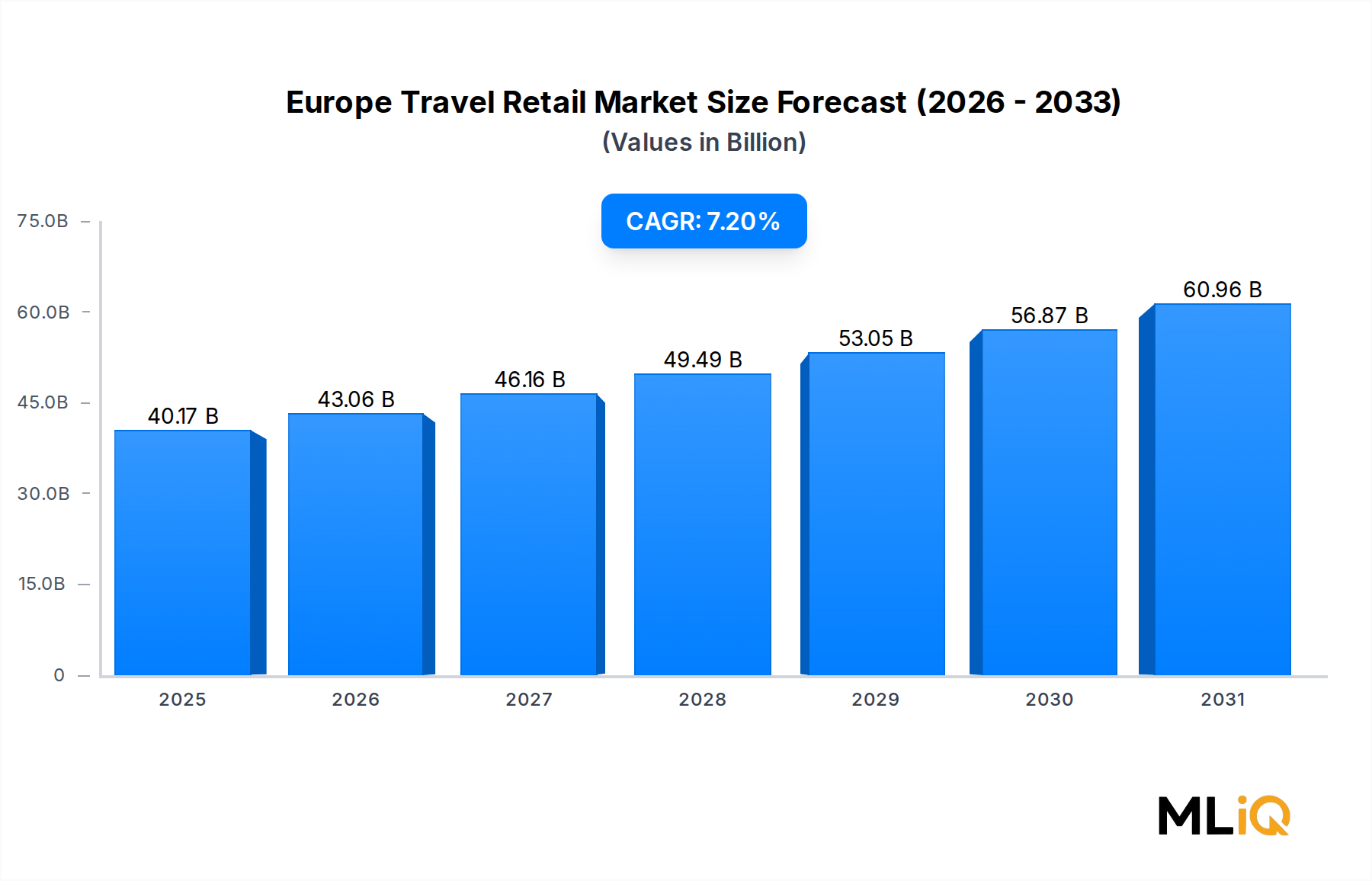

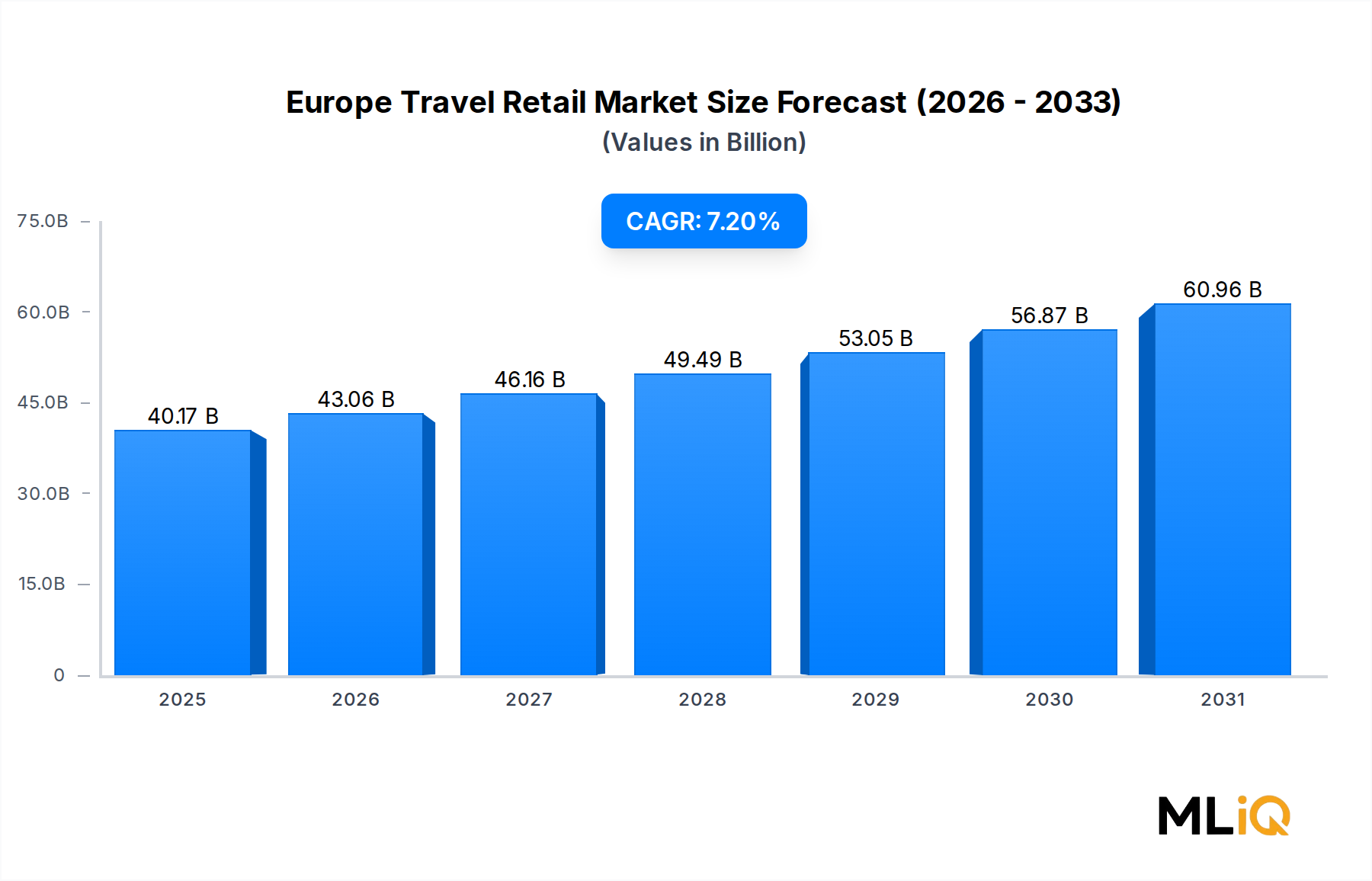

The Europe Travel Retail Market is positioned as one of the most dynamic consumer-facing segments within the broader European retail landscape. As of the base assessment period, the market is valued at $40.17 billion and is projected to expand at a compound annual growth rate (CAGR) of 7.2% through the forecast horizon of 2025–2033. This trajectory reflects a robust post-pandemic recovery cycle underpinned by structural growth in intra-European and intercontinental air travel, rising disposable incomes among European and Asian traveling consumers, and the continued premiumization of travel retail offerings.

Key demand drivers include the resurgence of international tourism across major European transit hubs such as London Heathrow, Frankfurt, Paris Charles de Gaulle, and Amsterdam Schiphol. These airports collectively manage hundreds of millions of passengers annually, providing a captive, high-spending consumer base that travel retailers are increasingly targeting with curated, exclusive merchandise. The expansion of low-cost carrier networks across the Nordics, Iberian Peninsula, and Eastern Europe has widened the passenger demographic, drawing in mid-market spenders alongside traditional luxury buyers.

Macro tailwinds include favorable currency dynamics that make European duty-free purchases particularly attractive to non-EU travelers, especially those from the United States, China, and Gulf Cooperation Council nations. The digital transformation of the travel retail experience — including pre-order platforms, personalized digital storefronts, and loyalty-integrated purchase systems — is enhancing conversion rates and average transaction values across all channel formats.

Product-wise, perfumes and cosmetics continue to anchor revenue generation, while wine and spirits, luxury goods, and confectionery are demonstrating accelerating demand across airport and cruise liner channels. The integration of experiential retail concepts — tasting rooms, personalized engraving, beauty consultation zones — is elevating the in-store dwell time and per-passenger spend metrics.

From a competitive standpoint, the market is moderately consolidated, with a handful of global operators controlling the majority of concession agreements at high-traffic nodes. However, the emergence of digitally enabled niche operators and brand-direct retail formats is gradually fragmenting the channel mix. Looking forward, the market is expected to benefit from European aviation capacity expansions, a rebound in Chinese outbound tourism, and continued infrastructure investments across Eastern European transit hubs through 2033.

Within the Europe Travel Retail Market, the perfume and cosmetics sub-segment consistently commands the largest share of total revenues, driven by a confluence of structural, behavioral, and channel-specific factors. This segment's supremacy is rooted in the fundamental shopping psychology of the travel retail environment: duty-free exclusivity, aspirational branding, and the tactile, sensory nature of fragrance and beauty products align perfectly with the impulse-driven purchase behavior exhibited by airport and cruise terminal consumers.

Perfume and cosmetics products benefit disproportionately from the duty-free value proposition. In markets where cosmetics and fragrances carry elevated VAT or import duties, the price savings at European travel retail outlets can range from 15% to 30% compared to domestic retail channels, providing a powerful, quantifiable incentive to purchase. This discount dynamic is particularly potent for international visitors from markets such as China, India, and the United States, where prestige beauty brands command premium pricing.

Major luxury conglomerates including LVMH Group (DFS Group Limited) and their portfolio brands — including Dior, Givenchy, and Guerlain — have invested heavily in flagship travel retail boutiques within key European airports. These installations function not merely as points of sale but as brand theaters, delivering immersive consumer experiences that reinforce brand equity while driving transaction volumes. Lagardère SCA, one of the sector's largest concession operators, has strategically structured its retail space allocations to ensure that beauty and fragrance zones occupy premium, high-footfall positions adjacent to departure gates and security exits.

The segment is further supported by the proliferation of limited-edition and travel-exclusive product lines, which create urgency and novelty among repeat travelers. These exclusives serve a dual commercial purpose: they justify higher average selling prices and generate social media shareability that amplifies brand reach beyond the point of purchase.

Gebr. Heinemann SE & Co. KG has been particularly active in developing curated beauty halls within German and Nordic airports, featuring an assortment that spans mass prestige to ultra-luxury tiers, effectively capturing a broader income spectrum of travelers. Similarly, Dufry AG has leveraged its pan-European concession network to implement unified planograms and cross-category promotional mechanics that drive basket size in the beauty category.

The segment's share, estimated to represent approximately 38%–42% of total European travel retail revenues, has remained structurally stable over the past five years, with modest share gains driven by the growing sophistication of skincare offerings alongside traditional fragrance lines. Emerging sub-categories such as niche and indie perfumery, K-beauty skincare, and clinical-grade travel skincare are incrementally diversifying the assortment and attracting younger demographics to the travel retail beauty channel.

Looking ahead, continued investment in digital integration — including AI-powered fragrance recommendation kiosks and augmented reality beauty try-on technologies — is expected to sustain the segment's competitive advantage and maintain its leadership position within the broader Perfume and Cosmetics Market dynamics observed across European retail channels.

The Europe Travel Retail Market is shaped by a set of well-defined structural drivers and identifiable constraints that collectively determine the pace and quality of market expansion through 2033.

On the demand side, the recovery of European passenger traffic to pre-COVID levels — with Eurocontrol reporting a return to approximately 94% of 2019 flight volumes by late 2023 — has been the single most significant catalyst for market re-acceleration. Each percentage point of passenger traffic recovery translates directly into incremental retail opportunity, as travel retail revenues are fundamentally tethered to passenger throughput at transit nodes.

The premiumization trend represents another critical driver. The share of luxury-tier purchases within total travel retail baskets has grown materially, with average transaction values rising by an estimated 12%–18% between 2021 and 2024 across major European airports. This is attributable to a structural shift in the traveler demographic: business-class and premium-economy travelers, who represent a disproportionate share of high-value retail spend, have shown stronger volume recovery compared to budget-segment passengers.

Currency dynamics provide a quantifiable macro tailwind. The persistent strength of the US dollar and Gulf currencies relative to the Euro and British Pound has enhanced the purchasing power of American and GCC travelers at European duty-free outlets, boosting basket sizes by an estimated 8%–14% in USD-equivalent terms since 2022.

On the constraint side, concession cost escalation poses a significant margin headwind. Airport operators, recognizing the revenue-generating potential of retail concessions post-pandemic, have renegotiated contracts with higher minimum annual guarantee clauses, compressing retailer margins across segments. Additionally, evolving EU regulatory frameworks around tobacco and alcohol advertising within transit zones are restricting promotional mechanics for two of the highest-margin product categories in the Duty-Free Retail Market ecosystem.

Supply chain volatility — particularly for electronics and luxury goods — has intermittently constrained product availability and forced inventory prioritization decisions that can temporarily reduce assortment breadth and category revenues.

The competitive landscape of the Europe Travel Retail Market features a blend of large multinational concession operators, regional specialists, and brand-owned retail formats competing across airports, cruise liners, railway stations, border shops, and downtown duty-free outlets.

TRE³: A specialized travel retail operator focused on delivering curated luxury and niche product assortments within European airport environments, emphasizing exclusive brand partnerships and data-driven category management strategies.

FLEMINGO INTERNATIONAL LTD.: An international travel retail operator with growing European exposure, leveraging its global supply chain infrastructure to offer competitive pricing across beauty, spirits, and confectionery categories.

LAGARDÈRE SCA: One of Europe's largest travel retail concession holders, operating an extensive portfolio of duty-free and duty-paid formats across major European airports; the company has consistently invested in digital retail integration and experiential store formats to drive per-passenger yield.

GEBR. HEINEMANN SE & CO. KG: A family-owned travel retail powerhouse headquartered in Hamburg, with deep concession relationships across German, Nordic, and Eastern European airports; known for its strong supplier partnerships and category leadership in spirits and beauty.

DAA PLC.: The operator of Dublin and Cork airports, with a vertically integrated travel retail model that allows direct control over concession space allocation, tenant mix optimization, and passenger experience design.

REGSTAER: A Russian-origin travel retail operator with historical presence across Eastern European and CIS transit hubs, navigating significant operational restructuring in response to geopolitical shifts affecting cross-border passenger flows.

DUFRY AG: One of the largest global travel retail operators by revenue, with a dominant European footprint spanning over 20 countries; Dufry AG has pursued aggressive acquisition-led growth and digital transformation through its Hudson and World Duty Free platforms.

AUTOGRILL S.P.A: An Italian operator specializing in food and beverage concessions within travel environments, with a growing integration of retail formats within its Italian and broader European airport and motorway network operations.

WH SMITH PLC.: A UK-based specialist in news, books, and convenience retail within travel environments; WH Smith has expanded its international airport presence significantly, with over 400 travel units across European and global airports.

LVMH GROUP (DFS GROUP LIMITED): The luxury retail arm of the LVMH conglomerate, operating brand-direct and multi-brand boutiques within premium European airports; its strategy centers on delivering a flagship luxury store experience within transit environments.

March 2023: Dufry AG completed its strategic merger integration with Autogrill S.P.A, creating Avolta — one of the world's largest travel experience companies — with combined revenues exceeding $10 billion and a strengthened pan-European retail and F&B footprint.

June 2023: Gebr. Heinemann SE & Co. KG announced a major concession renewal at Hamburg Airport, securing category-leading positions in beauty, spirits, and confectionery for a further 10-year term, reinforcing its dominance in the German travel retail corridor.

September 2023: Lagardère SCA finalized the divestiture of its travel retail division to Ardian and SIV as part of a broader group restructuring, with the Travel Retail segment rebranded and repositioned for accelerated organic growth under independent ownership.

January 2024: WH Smith PLC. reported a 22% year-on-year revenue increase in its international travel division, driven by new airport concession wins across France, Italy, and Scandinavia and a broadening product mix toward premium gifting and convenience categories.

April 2024: The European Commission published updated guidelines on duty-free allowances for intra-EU travel retail, triggering industry-wide discussions on the long-term structural viability of certain duty-free product categories within the Schengen zone.

November 2024: LVMH Group (DFS Group Limited) launched a new boutique format at Paris Charles de Gaulle Terminal 2E, combining multi-brand luxury retail with personalized client services, targeting the €500+ per-transaction spend segment among premium international travelers.

The Europe Travel Retail Market exhibits significant regional heterogeneity, with distinct growth profiles, demand structures, and competitive dynamics across its key sub-geographies.

The United Kingdom remains the single largest national market within the European travel retail context, anchored by London Heathrow — one of the world's highest-revenue single-airport retail environments. Despite post-Brexit complications that temporarily disrupted VAT-free shopping for domestic passengers, inbound international traveler volumes have rebounded strongly, and the UK market is estimated to account for approximately 18%–22% of total European travel retail revenues. The primary demand driver is the concentration of high-spending international transit passengers, particularly from North America, the Middle East, and Asia Pacific.

Germany represents the second-largest national market, with Frankfurt Airport functioning as a major continental hub. German travel retail benefits from strong business traveler volumes and a mature concession infrastructure. The market is growing at an estimated CAGR of 6.8%, slightly below the pan-European average, reflecting its maturity and high existing base.

France, anchored by Paris Charles de Gaulle and Paris Orly, is experiencing above-average growth driven by strong luxury goods demand from Chinese and American tourists. The French market is estimated to be growing at approximately 7.8% CAGR, benefiting from the aspirational positioning of Parisian brands within the travel retail assortment and the broader Global Consumer Goods Market premiumization trend.

The Nordics and Benelux represent some of the fastest-growing sub-regions within Europe, driven by expanding low-cost carrier penetration, rising outbound leisure travel, and progressive airport retail modernization programs. Stockholm Arlanda and Amsterdam Schiphol have both made significant investments in expanding retail concession space and improving the traveler experience. These markets are collectively estimated to grow at a blended CAGR of 8.1%–8.6% through 2033.

Eastern Europe — encompassing markets such as Poland, Czech Republic, and Romania — represents the highest-growth frontier, with nascent travel retail infrastructure rapidly scaling to meet surging passenger volumes. While absolute revenues remain a fraction of Western European levels, the growth velocity in Eastern European transit hubs is among the highest on the continent, supported by greenfield airport development and rising middle-class travel propensity.

Pricing strategy within the Europe Travel Retail Market is governed by a complex interplay of duty-free regulatory frameworks, brand-mandated minimum advertised price policies, concession cost structures, and competitive benchmarking against both domestic retail and online channels.

The foundational pricing advantage of travel retail — the elimination or reduction of VAT and import duties — is most potent for high unit-value categories. In the Luxury Goods Market, duty savings on watches, jewelry, and designer accessories can represent 20%–35% of the domestic retail price, making travel retail a primary purchase channel for aspirational consumers. In the Wine and Spirits Market, duty-free savings on premium and ultra-premium spirits typically range from 15%–25%, supporting strong category conversion rates among departing international passengers.

However, the margin structure for travel retail operators has come under increasing pressure from multiple vectors. Airport authorities, emboldened by post-pandemic traffic recovery, have significantly escalated concession fees and minimum guarantee thresholds in recent contract renewal cycles. Industry estimates suggest that concession cost as a percentage of gross retail sales has risen from approximately 25%–30% pre-pandemic to 30%–38% in more recently negotiated agreements at major European hubs, compressing operator EBITDA margins.

Supplier dynamics further complicate the margin picture. Luxury and premium brand owners — particularly those operating in the Perfume and Cosmetics Market — are increasingly asserting direct control over their travel retail distribution through brand-operated boutiques or highly prescriptive wholesale agreements that limit the operator's ability to discount or bundle products. This brand-direct pressure, while positive for retail price integrity, limits the promotional flexibility that operators historically used to drive footfall and basket size.

On the cost side, labor expenses at European airports — driven by minimum wage increases and unionized workforce agreements — have risen materially since 2022, adding a structurally higher fixed cost base that is difficult to offset through productivity gains alone. Currency volatility also introduces procurement cost unpredictability for operators sourcing internationally produced goods denominated in USD or GBP.

To counteract margin compression, leading operators are increasingly investing in private-label product development, data-driven assortment optimization, and digital pre-order platforms that reduce peak-period staffing requirements while increasing conversion certainty. The Airport Retail Market is also witnessing growing adoption of automated checkout and self-service technologies aimed at reducing per-transaction labor costs.

The Europe Travel Retail Market has been an active arena for

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Europe Travel Retail Market market expansion.

Key companies in the market include TRE³, FLEMINGO INTERNATIONAL LTD., LAGARDÈRE SCA, GEBR. HEINEMANN SE & CO. KG, DAA PLC., REGSTAER, DUFRY AG, AUTOGRILL S.P.A, WH SMITH PLC., LVMH GROUP (DFS GROUP LIMITED).

The market segments include Product, Channel.

The market size is estimated to be USD 40.17 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 3850, and USD 7449 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Europe Travel Retail Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Europe Travel Retail Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.