1. What are the major growth drivers for the Art Supplies Market market?

Factors such as are projected to boost the Art Supplies Market market expansion.

+1 2315155523

Art Supplies Market

Art Supplies Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

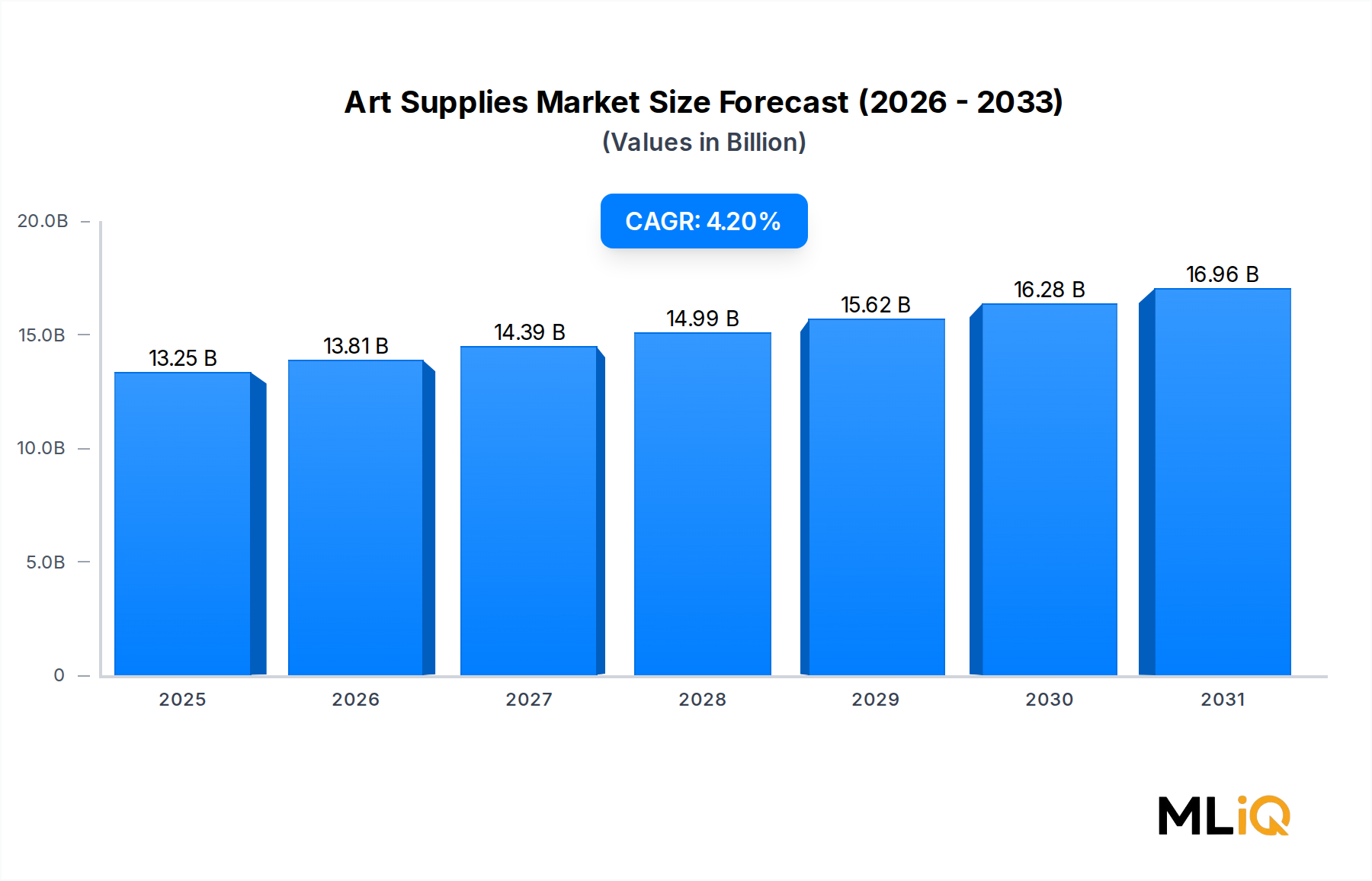

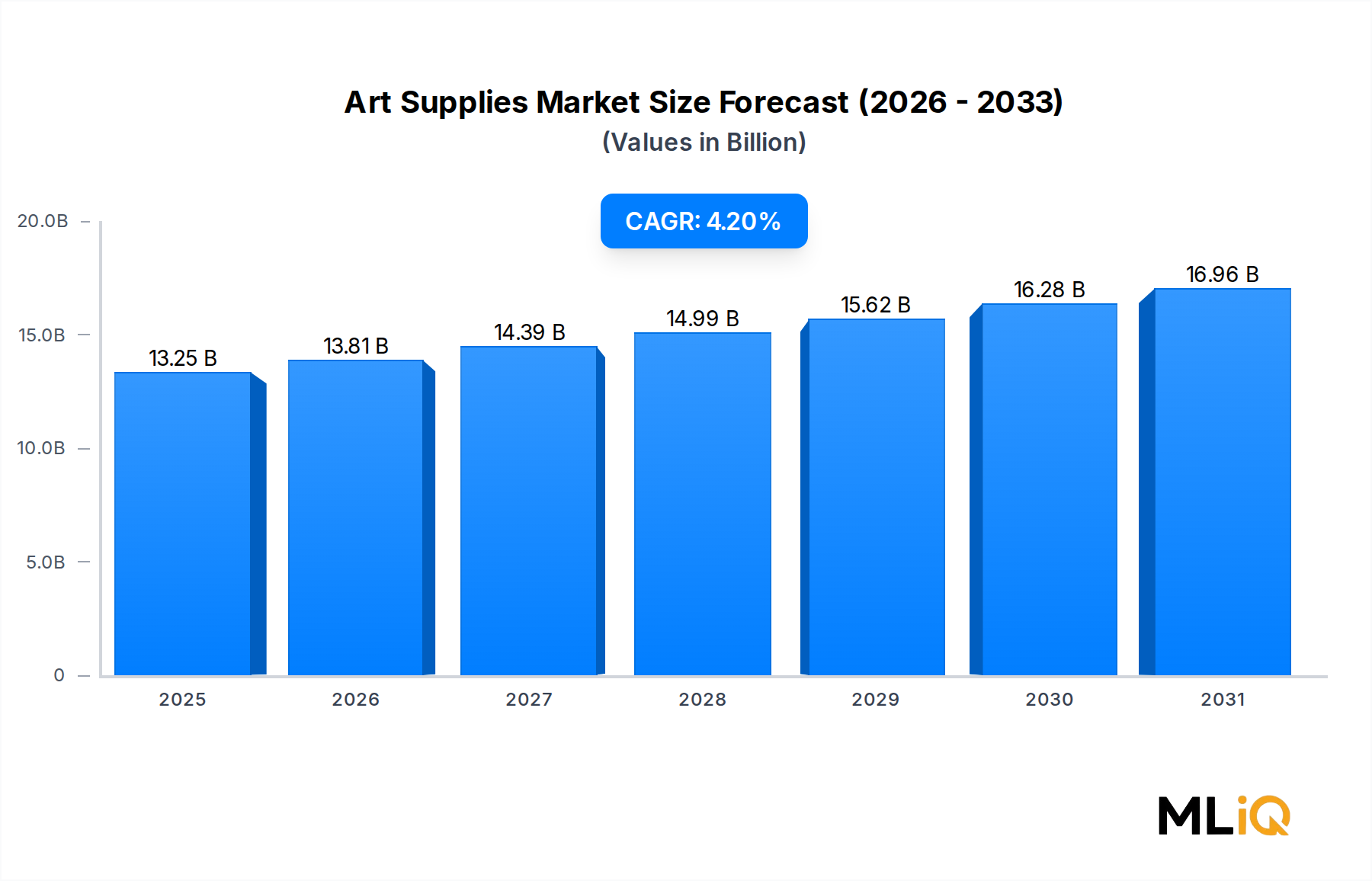

The global Art Supplies Market was valued at $13.25 billion in the base year and is projected to expand at a compound annual growth rate (CAGR) of 4.2% through the forecast period, reflecting sustained consumer interest in both recreational and professional artistic activities. This trajectory places the market among the more resilient segments within the broader Consumer Goods Market, driven by structural tailwinds including rising disposable incomes, the proliferation of social media art communities, and renewed institutional investment in arts education globally.

Demand is anchored by a diversified user base spanning household hobbyists, professional artists, educational institutions, and commercial studios. The post-pandemic period catalyzed a significant behavioral shift: millions of consumers adopted art-making as a wellness and mindfulness activity, generating a durable uplift in retail sales of entry-level and mid-tier products. This trend has persisted beyond the acute pandemic phase, embedding art supplies into routine household spending patterns.

On the supply side, manufacturers have responded with product premiumization strategies, introducing eco-friendly formulations, refillable systems, and digitally integrated tools that bridge traditional media with digital workflows. The convergence of physical art supplies with Digital Art Tools Market innovations has expanded the addressable market, particularly among Gen Z and millennial demographics who blend analog and digital creative practices.

Geographically, Asia Pacific represents the fastest-growing regional cluster, propelled by expanding middle-class populations in China and India and aggressive government spending on arts curriculum integration. North America and Europe retain the largest revenue shares, underpinned by established professional artist communities and robust institutional procurement cycles.

Key demand drivers include rising enrollment in art programs at both K-12 and tertiary levels, growth in the DIY craft movement supported by platforms such as Pinterest and YouTube, and increasing adoption of art therapy in clinical and corporate wellness settings. Constraints include raw material cost volatility — particularly for specialty pigments and natural fibers — and the ongoing substitution pressure from digital creation tools.

Looking forward, the market is expected to benefit from continued product innovation, particularly in sustainable and non-toxic formulations targeting the institutional and household segments. Strategic partnerships between art supply manufacturers and e-commerce platforms are anticipated to deepen market penetration in underserved geographies, supporting the projected CAGR of 4.2% through the end of the forecast window.

Within the Art Supplies Market, the Painting Supplies sub-segment commands the largest revenue share, consistently accounting for the plurality of total market value. This dominance is attributable to the broad applicability of painting media — including oil, acrylic, watercolor, and gouache — across all end-user categories from household hobbyists to professional studio artists and institutional buyers.

Acrylic-based products have emerged as the single most dynamic product category within Painting Supplies, driven by their versatility, relatively low cost compared to oil paints, fast drying time, and compatibility with a wide range of surfaces. The Acrylic Paint Market has experienced above-average growth relative to the broader art supplies category, supported by the expanding DIY home décor trend and the format's dominance in both educational and professional settings. Manufacturers such as Liquitex and Winsor & Newton have invested heavily in expanding their acrylic product lines, introducing heavy body, soft body, and fluid variants targeting distinct application needs.

Watercolor products occupy the second largest share within Painting Supplies, benefiting from resurgent popularity among social media artists and illustrators. The portability and accessibility of watercolor sets — particularly pan-based travel kits — have made them a preferred entry point for new artists. Canson Inc and Winsor & Newton have capitalized on this trend through targeted packaging and beginner-friendly kit bundling.

Oil paints, while representing a more mature and slower-growing sub-category, maintain a premium positioning that sustains high average selling prices. Professional-grade oil paint lines from manufacturers such as Winsor & Newton, Faber-Castell, and Da Vinci Brushes command significant revenue from fine art studios, galleries, and advanced-level art institutions.

The dominance of Painting Supplies is further reinforced by institutional procurement patterns. Schools, universities, and art institutes typically allocate the majority of their materials budgets to painting media, easels, canvases, and brushes, creating a reliable B2B revenue stream that insulates the sub-segment from cyclical consumer spending fluctuations.

Competitive intensity within Painting Supplies is high. Market leaders are consolidating share through product premiumization, sustainability certifications (such as ACMI AP non-toxic labels), and direct-to-consumer digital channels. Private-label products from specialty art retailers have introduced pricing pressure at the entry-level tier, compelling branded manufacturers to differentiate on formulation quality, color range breadth, and artist endorsements.

The Painting Supplies sub-segment's share is assessed as consolidating rather than expanding: while absolute revenues are growing in line with the overall market CAGR, the Drawing Supplies and Craft Supplies sub-segments are gaining relative share as DIY craft culture and the Colored Pencils Market experience above-average growth. Nevertheless, Painting Supplies is expected to retain its plurality position throughout the forecast period, anchored by institutional demand and the continued premiumization of professional-grade product lines.

Supply chain resilience is a key strategic differentiator in this sub-segment. Manufacturers with vertically integrated pigment sourcing or long-term supplier agreements for natural and synthetic pigments have demonstrated superior margin stability, particularly during periods of raw material cost volatility.

The Art Supplies Market is propelled by a set of quantifiable structural drivers while simultaneously navigating several binding constraints that temper the overall growth trajectory.

Among the primary drivers, the expansion of arts education represents the most durable demand foundation. UNESCO data indicates that over 60% of countries have strengthened national arts education mandates since 2019, directly increasing institutional procurement of drawing, painting, and craft supplies. This policy tailwind has translated into consistent volume growth in the Institutions end-user segment.

The wellness and mindfulness movement constitutes a second major driver. Global market research consistently identifies art therapy adoption as a high-growth application area, with art therapy programs growing at approximately 6% annually within healthcare and corporate wellness settings. This has created a structurally new demand channel for premium, non-toxic art materials, benefiting players such as Sakura Color Products Corporation and Crayola LLC who have positioned product lines explicitly for therapeutic contexts.

E-commerce channel growth has amplified market reach substantially. Online distribution now accounts for a rising share of total art supplies revenue, with platforms enabling long-tail product discovery and enabling niche manufacturers to access global customer bases without physical retail infrastructure.

On the constraints side, raw material cost volatility presents the most significant near-term risk. Key inputs including cadmium, cobalt, and titanium dioxide — critical components for high-chroma pigment formulations — have experienced price increases of 15–25% over the past three years due to mining supply disruptions and geopolitical factors affecting sourcing regions. This has directly pressured manufacturer margins and, in some cases, necessitated retail price increases that soften volume demand at price-sensitive tiers.

Substitution pressure from digital creation platforms represents a structural headwind, particularly within younger demographics. While the Digital Art Tools Market does not fully substitute for physical media, it competes directly for discretionary creative spending and time allocation, particularly among entry-level consumers who might otherwise purchase starter art supply kits.

The competitive landscape of the Art Supplies Market is characterized by a mix of global conglomerates, specialty manufacturers, and regionally dominant players. The following profiles outline the strategic positioning of key participants:

Sakura Color Products Corporation: A Japan-based manufacturer renowned for its Pigma Micron ink pens and Koi watercolor lines, Sakura maintains a strong position in the professional illustration and fine art segments with a broad global distribution network.

Da Vinci Brushes: Specializing in premium handcrafted artist brushes, Da Vinci Brushes targets professional and semi-professional artists and competes primarily on craftsmanship quality and the use of natural hair materials sourced under ethical standards.

Winsor & Newton: One of the most recognized heritage brands in fine art materials, Winsor & Newton operates across oil, acrylic, watercolor, and gouache categories, commanding a premium positioning in both retail and institutional channels globally.

Prismacolor: Known for its professional-grade colored pencils, markers, and illustration tools, Prismacolor is a dominant player in the art education and professional illustration segments, particularly across North American markets.

Crayola LLC: The world's leading mass-market art supplies brand targeting children and household users, Crayola LLC leverages extensive retail distribution, strong brand equity, and consistent product innovation across crayons, markers, and craft kits.

Koh-I-Noor Hardtmuth: A Czech manufacturer with over two centuries of history, Koh-I-Noor Hardtmuth produces a wide range of drawing and writing instruments and maintains strong distribution across European and emerging markets.

Pentel Co., Ltd.: A diversified Japanese manufacturer offering products from fine-line pens and mechanical pencils to artist brushes and acrylic paints, Pentel competes across both the professional and consumer market tiers with an emphasis on precision and innovation.

Liquitex: A pioneer in professional acrylic paint technology and a subsidiary of ColArt, Liquitex is recognized for its innovation in acrylic mediums and holds a leading position in fine art retail channels globally.

Canson Inc: A premium paper and fine art supplies brand with roots in French paper-making heritage, Canson Inc holds significant market share in drawing and watercolor papers, serving professional artists and educational institutions.

Faber-Castell: A German family-owned conglomerate with a global footprint spanning over 160 countries, Faber-Castell competes across the full spectrum from mass-market school supplies to ultra-premium artist instruments and luxury writing accessories.

March 2024: Faber-Castell announced the expansion of its sustainable product line, introducing a new range of pencils manufactured using 100% PEFC-certified wood, targeting institutional and environmentally conscious consumer segments across Europe and North America.

June 2024: Crayola LLC launched a new art therapy-focused product collection developed in collaboration with licensed art therapists, positioning the brand in the growing clinical and educational wellness application segment.

September 2023: Winsor & Newton unveiled a reformulated Professional Watercolour range featuring enhanced lightfastness ratings, responding to professional artist demand for archival-quality pigment stability in long-term artwork preservation.

November 2023: Sakura Color Products Corporation expanded its direct-to-consumer e-commerce capabilities in Southeast Asia, entering the rapidly growing ASEAN regional market and targeting the underserved professional illustration community in Indonesia and the Philippines.

January 2024: Liquitex introduced a new bio-based acrylic binder line as part of a multi-year sustainability roadmap, reducing the petrochemical content of its most popular medium and varnish products by 30%.

April 2024: Pentel Co., Ltd. formed a strategic distribution partnership with a major pan-European stationery distributor to accelerate its market share growth in Germany, France, and the Benelux region, directly targeting the institutional and office channel.

February 2024: The Art and Creative Materials Institute (ACMI) updated its product certification standards for non-toxic labeling, creating new compliance requirements affecting over 200 products across multiple manufacturers, with full enforcement expected by late 2025.

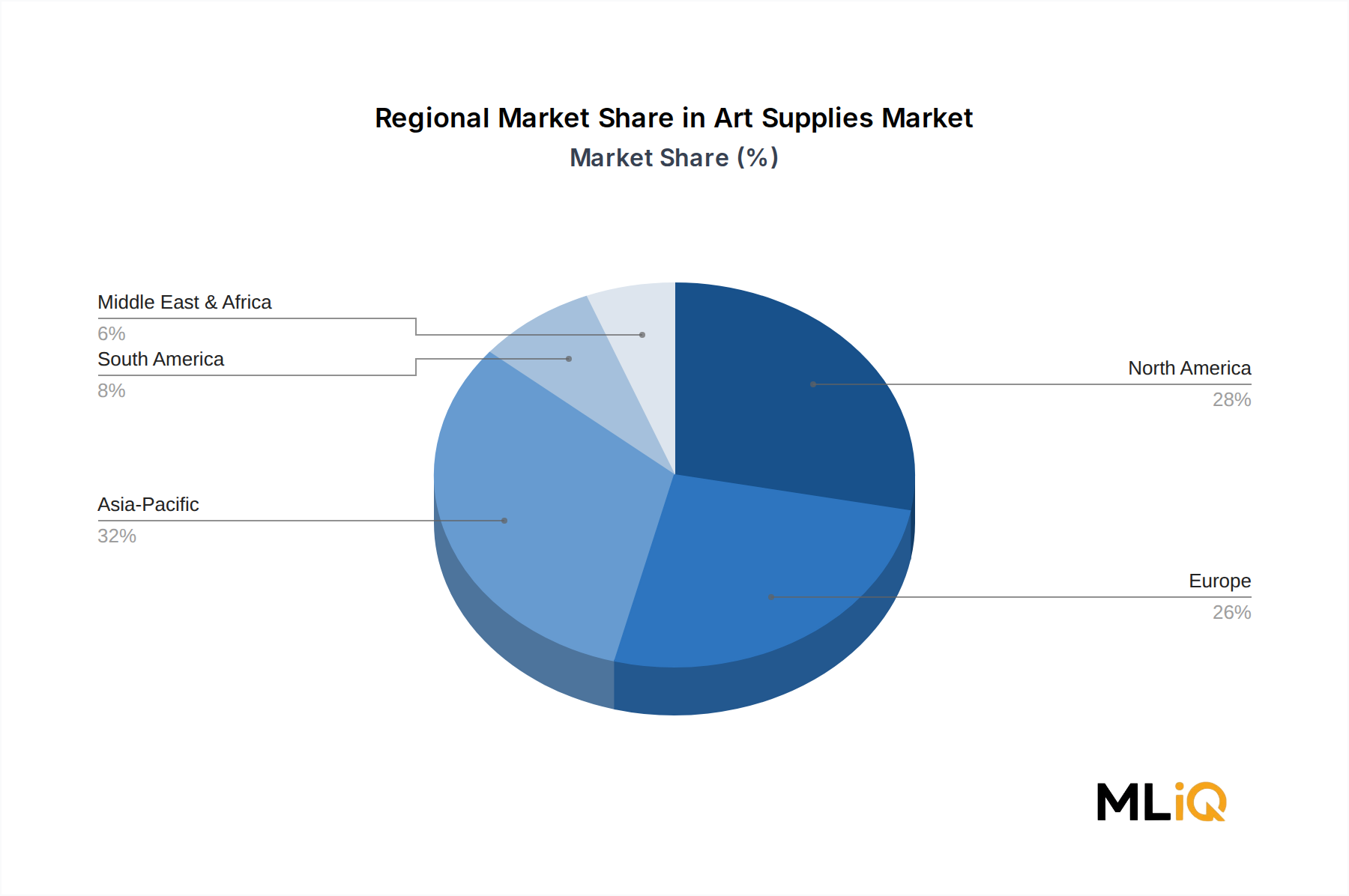

The Art Supplies Market exhibits distinct regional growth profiles reflecting variations in consumer demographics, institutional procurement, and economic development trajectories.

North America represents the most mature regional market, accounting for approximately 32% of global revenue. The United States drives the majority of regional demand through a combination of robust retail infrastructure, high per-capita art education spending, and a large professional artist community. Canada and Mexico contribute secondary revenue streams, with Mexico showing above-average growth driven by expanding middle-class participation in art education. The regional CAGR is estimated at 3.6%, reflecting a mature but stable growth environment anchored by institutional and professional demand channels.

Europe holds the second-largest revenue share at approximately 28% of the global total. Germany, the United Kingdom, and France are the leading national markets, supported by strong fine art traditions, well-funded public arts education systems, and high consumer willingness to pay for premium products. The regional CAGR is estimated at 3.4%, with growth restrained by demographic saturation and high market penetration in core product categories. Italy and Spain represent secondary growth nodes, particularly for premium painting and drawing supplies.

Asia Pacific is the fastest-growing region, projected at a regional CAGR of 6.1%, substantially above the global average. China and India are the primary engines: China benefits from government-mandated arts curriculum expansion and a surging middle-class consumer base, while India's growth is driven by rapidly expanding K-12 enrollment and rising urban disposable incomes. Japan and South Korea contribute premium-tier demand, particularly in professional and hobbyist segments. ASEAN markets represent a high-potential frontier with relatively low current penetration.

Latin America, led by Brazil and Argentina, is growing at an estimated CAGR of 4.5%, supported by increasing arts education investment and the expansion of e-commerce channels that improve product accessibility in geographically dispersed markets.

The Middle East & Africa region is the smallest by absolute value but shows dynamic growth in Gulf Cooperation Council countries and South Africa, with a regional CAGR estimated at 5.2% driven by government cultural investment programs and expanding educational infrastructure.

The supply chain underpinning the Art Supplies Market is complex, spanning multiple upstream material categories with distinct sourcing geographies and price dynamics. Understanding these dependencies is critical for forecasting margin trajectories and identifying strategic vulnerabilities.

Pigments constitute the most strategically sensitive input category. Inorganic pigments — including titanium dioxide (white), cadmium compounds (reds, oranges, yellows), and cobalt derivatives (blues, greens) — are subject to significant price volatility driven by mining output disruptions, environmental regulations, and energy-intensive processing requirements. Titanium dioxide prices rose by approximately 18% between 2021 and 2023 due to tightened Chinese production capacity and elevated energy costs in European refining facilities. Cadmium-based pigments face additional regulatory risk related to heavy metal restrictions, particularly in the European Union, which is driving reformulation investment across multiple manufacturers.

Natural fiber inputs — including kolinsky sable, hog bristle, and pony hair used in artist brushes — are subject to sourcing risks related to animal welfare regulations and geographic concentration of supply in Russia and China. The geopolitical disruption of Russian supply chains since 2022 has created upward pricing pressure on premium natural hair brushes, benefiting synthetic fiber alternatives and companies such as Da Vinci Brushes that maintain diversified sourcing strategies.

Paper and board substrates represent a significant input for both the Craft Paper Market and fine art paper products. Pulp prices experienced a 22% increase in 2022 before moderating in 2023, directly affecting the cost structures of manufacturers reliant on high-grade cotton rag and wood-free papers. Canson Inc and Fabriano, as vertically integrated paper manufacturers, were partially insulated from these fluctuations.

Solvents and binders — particularly acrylic emulsions and linseed oil — are petrochemical-derived inputs that track crude oil price movements, introducing macroeconomic sensitivity into the cost base of painting supply manufacturers. The Pigments and Dyes Market dynamics therefore have direct cascading effects on the Art Supplies Market's input cost structure.

Logistics disruptions during 2021–2022 — including container shipping bottlenecks and port congestion — elevated landed costs for Asian-manufactured products by an estimated 20–35%, compressing margins for importers and accelerating reshoring assessments among European and North American distributors.

The regulatory environment governing the Art Supplies Market is multi-layered, encompassing product safety standards, chemical restriction frameworks

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.2% from 2020-2034 |

| Segmentation |

|

Factors such as are projected to boost the Art Supplies Market market expansion.

Key companies in the market include Sakura Color Products Corporation, Da Vinci Brushes, Winsor & Newton, Prismacolor, Crayola LLC, Koh-I-Noor Hardtmuth, Pentel Co., Ltd., Liquitex, Canson Inc, Faber-Castell.

The market segments include Product Type, End User, Distribution Channel.

The market size is estimated to be USD 13.25 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4065, and USD 6809 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Art Supplies Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Art Supplies Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.