1. What are the major growth drivers for the Barbecue Grill Market market?

Factors such as are projected to boost the Barbecue Grill Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

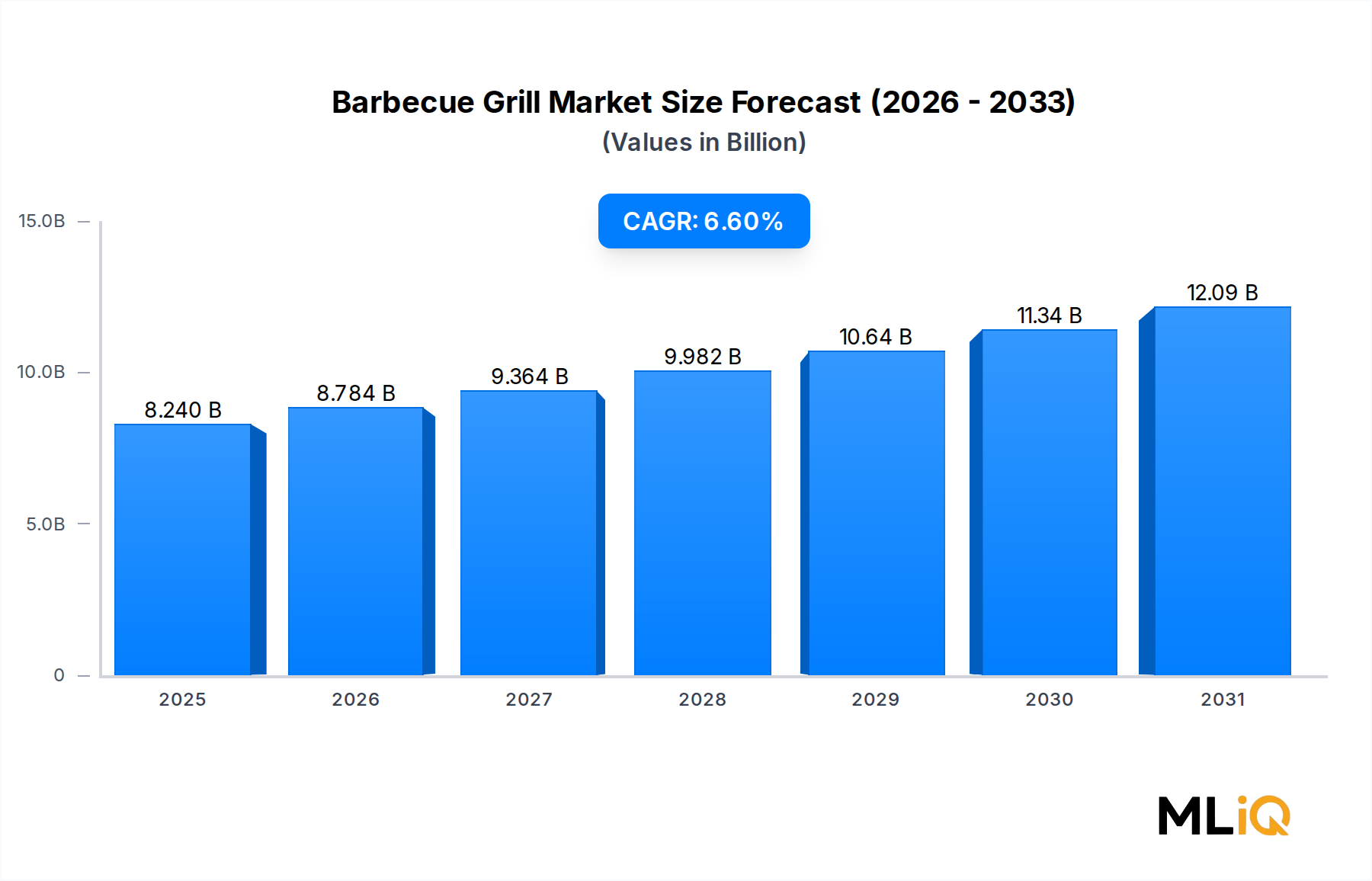

The global Barbecue Grill Market was valued at $8.24 billion and is projected to expand at a compound annual growth rate (CAGR) of 6.6% through the forecast horizon. This sustained trajectory reflects a confluence of evolving consumer lifestyles, increased discretionary spending on outdoor leisure, and rapid product innovation spanning fuel types, connectivity features, and materials engineering.

Several macro tailwinds are reinforcing the market's upward momentum. The post-pandemic normalization of home-centered entertainment has proven structurally durable rather than transient; consumers who upgraded their outdoor cooking setups during 2020–2022 are now cycling into premium or technologically differentiated replacement units. Simultaneously, urbanization patterns in emerging economies are expanding the addressable consumer base, with apartment-friendly electric and compact charcoal units opening new demographic corridors that were previously inaccessible to traditional propane or wood-fired product lines.

Demand drivers extend well beyond North America's historically dominant grilling culture. Europe's outdoor leisure sector, particularly in the United Kingdom, Germany, and the Nordic nations, has embraced premium gas and ceramic kamado-style grills as lifestyle statements. In Asia Pacific, rising middle-class incomes and Western culinary influence are accelerating adoption in China, India, South Korea, and the ASEAN bloc, where both residential and commercial end-users are contributing to volume growth.

From a segmentation perspective, the conventional fuel segment — encompassing charcoal, gas, and wood-pellet configurations — commands the majority of revenue, driven by consumer preference for authentic flavor profiles that electric alternatives struggle to fully replicate. However, the electric segment is the fastest-growing sub-category by volume, powered by urban regulatory restrictions on open-flame combustion and increasing environmental awareness among millennial and Gen Z purchasers.

Distribution dynamics are also shifting materially. Online sales channels have captured an expanding share of unit volumes, with direct-to-consumer platforms enabling brands such as Traeger and Weber-Stephen Products LLC to build loyalty ecosystems through subscription accessories, proprietary rubs, and firmware-updated smart controllers. Specialty stores retain relevance for high-ticket purchases requiring tactile evaluation, while supermarkets and hypermarkets continue to serve the value and mid-range segments effectively.

Looking forward, the convergence of IoT connectivity, app-based temperature management, and sustainability-oriented biomass fuel innovation positions the Barbecue Grill Market for continued premiumization. Brands investing in smart features and eco-friendly materials are expected to capture disproportionate margin expansion relative to commodity competitors. The market outlook through the end of the decade remains constructive, supported by robust product pipelines, expanding geographic footprints, and resilient consumer engagement with outdoor culinary culture.

Within the Barbecue Grill Market, the conventional segment — encompassing gas (liquid propane and natural gas), charcoal, and wood-pellet grills — represents the single largest revenue-generating category by a substantial margin. This dominance is rooted in deeply ingrained cultural behaviors, superior flavor performance, and a broad product portfolio that spans entry-level kettle grills retailing below $50 to bespoke built-in outdoor kitchen islands priced above $10,000.

Charcoal grills have historically served as the entry point for new consumers, offering low upfront cost and high-heat searing capability that resonates strongly in markets where grilling is a communal ritual rather than a solitary cooking method. In North America and South America — particularly Brazil, home to the iconic churrasco tradition — charcoal remains the default fuel type despite the operational convenience advantages offered by gas alternatives. The Charcoal and Briquettes Market is therefore tightly coupled with this segment's performance, with branded premium charcoal products such as lump hardwood and restaurant-grade briquettes generating meaningful cross-sell revenue for grill manufacturers.

Gas grills occupy the premium-to-mainstream middle ground, delivering the convenience of instant ignition, precise temperature control, and reduced cleanup time that time-pressed suburban consumers prioritize. Weber-Stephen Products LLC, W.C. Bradley Co., and Wolf Steel Ltd have invested heavily in this sub-category, differentiating through multi-burner configurations, integrated side burners, infrared searing zones, and rotisserie systems. The Gas Grill Market has become a battleground for stainless steel quality differentiation, with 304-grade and 430-grade alloys defining perceived durability tiers and corresponding price positioning.

The wood-pellet grill sub-category represents the most dynamic growth vector within the conventional segment. Traeger, Inc. pioneered the category and continues to hold the largest share, but Green Mountain Grills LLC, NOMAD Grills LLC, and Middleby Corporation have entered with competitive hardware and proprietary pellet formulations. The appeal of pellet grills lies in their ability to deliver authentic smoke flavor with push-button digital control, effectively democratizing barbecue techniques that previously required years of skill development. The Pellet Grill Market has attracted significant venture and strategic capital, reflecting investor conviction in its long-term consumer adoption curve.

Key players in the conventional segment are consolidating their positions through vertical integration strategies — acquiring pellet suppliers, building out accessories ecosystems, and deploying subscription services that generate recurring revenue beyond the initial hardware sale. Weber-Stephen Products LLC's investment in its Weber Connect smart grilling hub exemplifies this platform strategy, transforming a hardware transaction into an ongoing digital relationship. Similarly, Traeger's software ecosystem — spanning guided cook programs, recipes, and remote monitoring — deepens customer lock-in and elevates switching costs.

The conventional segment's share is not merely holding; it is expanding in absolute dollar terms as premiumization drives up average selling prices. Even as unit volumes in mature markets plateau, revenue per unit has increased steadily as consumers trade up from entry-level kettle charcoal grills to mid-range gas configurations and, increasingly, to pellet or hybrid multi-fuel platforms. This premiumization trend is expected to sustain the segment's dominant position through the forecast period, reinforcing its role as the primary growth engine of the broader Barbecue Grill Market.

Several quantifiable forces are actively shaping demand trajectories and competitive dynamics within the Barbecue Grill Market. Understanding both the accelerants and the impediments is essential for accurate forecasting and strategic positioning.

On the demand-acceleration side, the outdoor living real estate investment trend is a primary structural driver. U.S. homeowners allocated an estimated $52 billion to outdoor living improvements in recent years, with dedicated grilling and outdoor kitchen infrastructure representing one of the highest-return remodeling categories by resale value. This macro investment cycle sustains replacement demand and upgrades across the residential segment. The Residential Outdoor Living Market is a direct feeder channel for barbecue grill unit economics, particularly in the premium and luxury tiers.

Healthier cooking perception is a secondary demand driver. Consumer research consistently indicates that grilling is associated with lower-fat cooking methods compared to pan-frying or deep-frying, aligning with wellness trends that have materially reshaped food preparation behavior. This perception reinforces purchase intent among health-conscious demographics and supports premium pricing for grills marketed with precision temperature features.

The Smart Kitchen Appliances Market represents an adjacent innovation vector with direct implications for barbecue grills. Wi-Fi and Bluetooth-enabled grill controllers, integrated meat probes with cloud connectivity, and AI-driven cook cycle automation are migrating from premium to mid-range price tiers. This connectivity diffusion broadens the addressable market for smart grills beyond early adopters, adding a technology upgrade cycle on top of the traditional replacement cycle.

On the constraint side, raw material cost volatility poses a persistent challenge. Stainless steel, cast iron, and aluminum — the primary structural materials — are subject to significant price fluctuation tied to global commodity markets. The Stainless Steel Components Market experienced pronounced cost inflation between 2021 and 2023, compressing margins for manufacturers unable to pass through full cost increases to price-sensitive consumers. Supply chain normalization has partially alleviated this pressure, but geopolitical trade risks maintain elevated uncertainty.

Seasonal demand concentration is an operational constraint that limits annual revenue predictability. In North America and Europe, approximately 60–70% of annual grill sales occur in the spring-summer window, creating inventory management complexity and limiting the leverage of fixed manufacturing and distribution overhead.

The competitive landscape of the Barbecue Grill Market is characterized by a mix of legacy hardware manufacturers, digitally native disruptors, and diversified consumer goods conglomerates. Key participants are profiled below.

Weber-Stephen Products LLC: The market's most recognized brand, Weber commands premium shelf placement across all distribution channels and has invested aggressively in its connected grilling platform, integrating hardware with digital cook guidance to deepen consumer loyalty.

Traeger, Inc.: The defining innovator of the modern wood-pellet grill category, Traeger combines proprietary pellet fuel, app-based temperature management, and a robust culinary content ecosystem to create a differentiated lifestyle brand that commands strong pricing power.

Wolf Steel Ltd: Operating under the Napoleon brand, Wolf Steel Ltd targets the premium and luxury outdoor kitchen segment with high-gauge stainless steel construction, multi-fuel versatility, and an expansive dealer network across North America and Europe.

W.C. Bradley Co.: The parent company of the Char-Broil brand, W.C. Bradley Co. focuses on accessible price points and mass-market distribution, leveraging TRU-Infrared cooking technology as a differentiating feature across its mid-range gas grill lineup.

Middleby Corporation: A diversified commercial and residential cooking equipment manufacturer, Middleby Corporation has expanded its outdoor cooking portfolio through strategic acquisitions, targeting the premium residential and commercial foodservice segments simultaneously.

Green Mountain Grills LLC: A specialist pellet grill brand known for its Wi-Fi-enabled controllers and value-to-performance positioning, Green Mountain Grills LLC competes directly against Traeger in the connected pellet segment with a strong independent dealer channel.

NOMAD Grills LLC: Focused on portable and adventure-oriented grilling hardware, NOMAD Grills LLC addresses the compact outdoor recreation segment with rugged, lightweight designs suitable for camping, tailgating, and travel use cases.

SharkNinja Operating LLC: Leveraging its expertise in countertop cooking appliances, SharkNinja Operating LLC has entered the outdoor grill space with electric and hybrid products targeting urban consumers constrained by balcony regulations or limited outdoor space.

Newell Brand Inc.: Through its Coleman and other outdoor brands, Newell Brand Inc. addresses the portable and recreational grill segment, distributing through mass retail and outdoor specialty channels with competitively priced entry-level hardware.

Spectrum Brands Holdings, Inc: Operating the George Foreman and other grill brands, Spectrum Brands Holdings, Inc focuses on electric and contact grill categories, competing in indoor-outdoor crossover applications with high household penetration.

Transform SR Brands LLC: The operator of the Kenmore and DieHard brands through Sears-derived retail infrastructure, Transform SR Brands LLC maintains a value-tier gas grill presence distributed through e-commerce and remaining brick-and-mortar outlets.

Empire Comfort Systems: A manufacturer of gas heating and outdoor cooking products, Empire Comfort Systems serves the built-in and commercial segment with durable, specification-grade burner systems integrated into outdoor kitchen cabinetry.

RH Peterson Co.: A premium outdoor gas grill and burner manufacturer, RH Peterson Co. markets under the Fire Magic and American Outdoor Grill brands, targeting the luxury residential and hospitality installation segment.

Portable Kitchens, Inc.: Specializing in modular outdoor cooking stations, Portable Kitchens, Inc. addresses the commercial catering and event services segment with transportable, high-output grill systems.

Landmann USA, LLC: A U.S. subsidiary of the German Landmann group, Landmann USA LLC distributes charcoal, gas, and wood-pellet grills through mass retail, combining European design heritage with competitive domestic pricing.

January 2023: Weber-Stephen Products LLC launched the Weber Connect 2.0 smart grilling hub with expanded Bluetooth mesh connectivity, supporting multi-device pairing and a redesigned mobile application with step-by-step guided cook programs.

March 2023: Traeger, Inc. introduced the Traeger Timberline XL with dual-sided grilling grates, a built-in pellet sensor, and integration with Amazon Alexa voice commands, reinforcing its leadership in the connected pellet grill category.

June 2023: SharkNinja Operating LLC entered the outdoor grill segment with the Ninja Woodfire Outdoor Grill, combining electric heating with wood pellet smoke infusion to address urban consumers restricted from gas or charcoal use on residential balconies.

September 2023: Middleby Corporation completed the acquisition of a regional outdoor cooking equipment manufacturer, expanding its residential premium outdoor kitchen portfolio and integrating new cast-iron burner technology into its product line.

February 2024: Green Mountain Grills LLC launched a firmware update enabling predictive temperature algorithms for its Peak Prime Wi-Fi pellet grill, utilizing machine learning models trained on over one million user cook sessions to optimize fuel consumption.

April 2024: The U.S. Consumer Product Safety Commission issued updated guidelines for portable gas grill hose and regulator safety standards, prompting reformulation and recall reviews across several mid-market manufacturers.

July 2024: Wolf Steel Ltd announced an expanded distribution agreement covering 14 European markets through a network of premium kitchen appliance dealerships, targeting the growing European outdoor kitchen installation segment.

October 2024: NOMAD Grills LLC completed a Series A funding round to accelerate product development of a collapsible pellet-compatible travel grill, with commercialization targeted for the outdoor recreation retail channel.

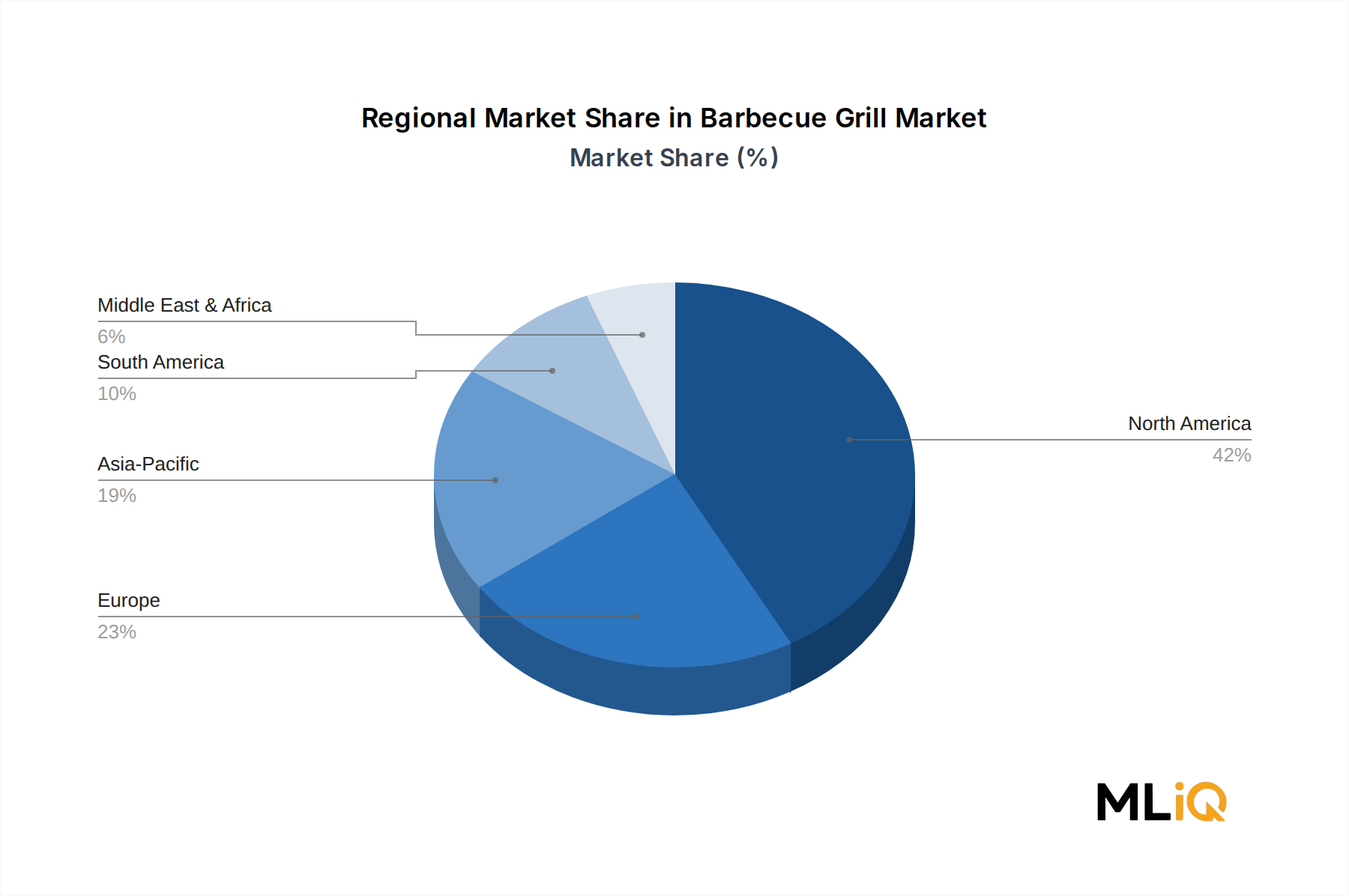

The Barbecue Grill Market exhibits pronounced regional heterogeneity across both growth rates and demand drivers, reflecting divergent cultural relationships with outdoor cooking, income profiles, and regulatory environments.

North America represents the most mature and highest-revenue region, accounting for an estimated 35–40% of global market value. The United States is the single largest national market, underpinned by deeply embedded grilling culture, high homeownership rates, and robust spending on outdoor living improvements. Canada contributes meaningfully through its strong suburban homeownership base and a seasonal grilling culture that mirrors U.S. patterns. Mexico is an emerging contributor within the region, with middle-class urbanization driving adoption of gas grills as aspirational household purchases. North America's regional CAGR is estimated at approximately 5.2%, reflecting the premiumization trajectory of a largely penetrated market.

Europe is the second-largest region by revenue, with the United Kingdom and Germany serving as the primary volume markets. The UK's strong outdoor entertaining culture, combined with Germany's tradition of garden parties (Grillabend), sustains consistent annual demand. France, Spain, and Italy are growing contributors as outdoor kitchen integration in residential properties accelerates. The Nordic countries show disproportionately high per-capita premium grill ownership. Europe's estimated regional CAGR stands at 5.8%, with growth driven by premiumization and the adoption of pellet and kamado-style grills displacing entry-level charcoal units.

Asia Pacific is the fastest-growing region, with an estimated CAGR of 8.4%. China, India, South Korea, and the ASEAN markets are the primary growth engines, driven by rising disposable incomes, Western culinary influence disseminated through social media, and expanding modern retail infrastructure. Japan maintains a distinctive yakitori and teppanyaki grilling culture that supports a premium tabletop and specialty grill sub-segment. The commercial foodservice channel — encompassing restaurants, hotels, and outdoor dining venues — is a particularly active demand source across ASEAN. The Commercial Foodservice Equipment Market in Asia Pacific is directly catalyzing institutional barbecue grill procurement at a scale not seen in previous decades.

South America, anchored by Brazil's world-renowned churrasco culture, represents a culturally significant and structurally resilient regional market. Brazil's per-capita charcoal grill ownership is among the

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.6% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Barbecue Grill Market market expansion.

Key companies in the market include Wolf Steel Ltd, Landmann USA, LLC, SharkNinja Operating LLC., Traeger, Inc., Spectrum Brands Holdings, Inc, W.C. Bradley Co., RH Peterson Co., Weber-Stephen Products LLC, Newell Brand Inc., Portable Kitchens, Inc., Transform SR Brands LLC, Green Mountain Grills LLC, NOMAD Grills, LLC., Middleby Corporation, Empire Comfort Systems.

The market segments include Type, Application, Distribution Channel.

The market size is estimated to be USD 8.24 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Barbecue Grill Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Barbecue Grill Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.