1. What are the major growth drivers for the Baby Safety Gadgets Market market?

Factors such as are projected to boost the Baby Safety Gadgets Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

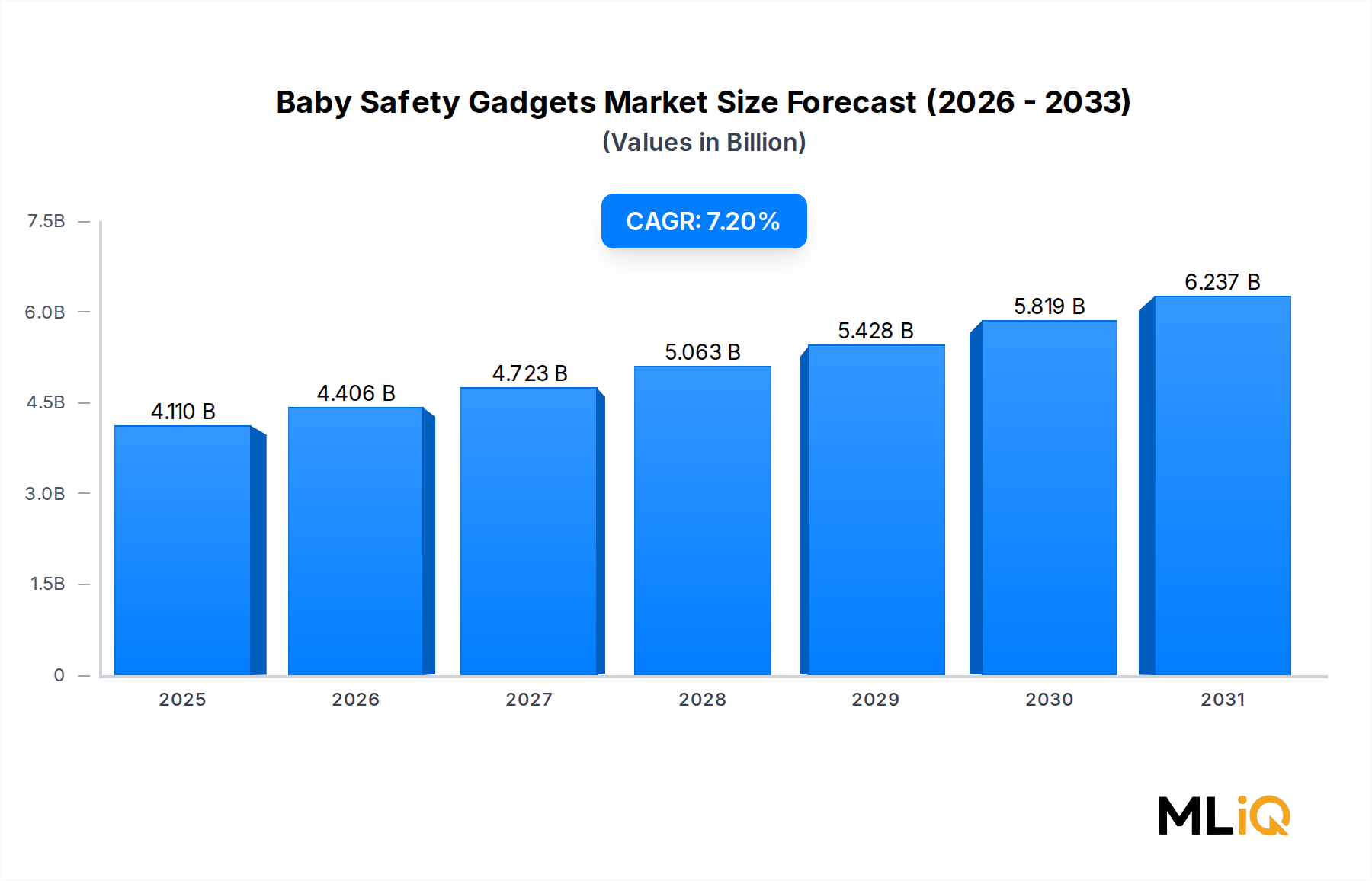

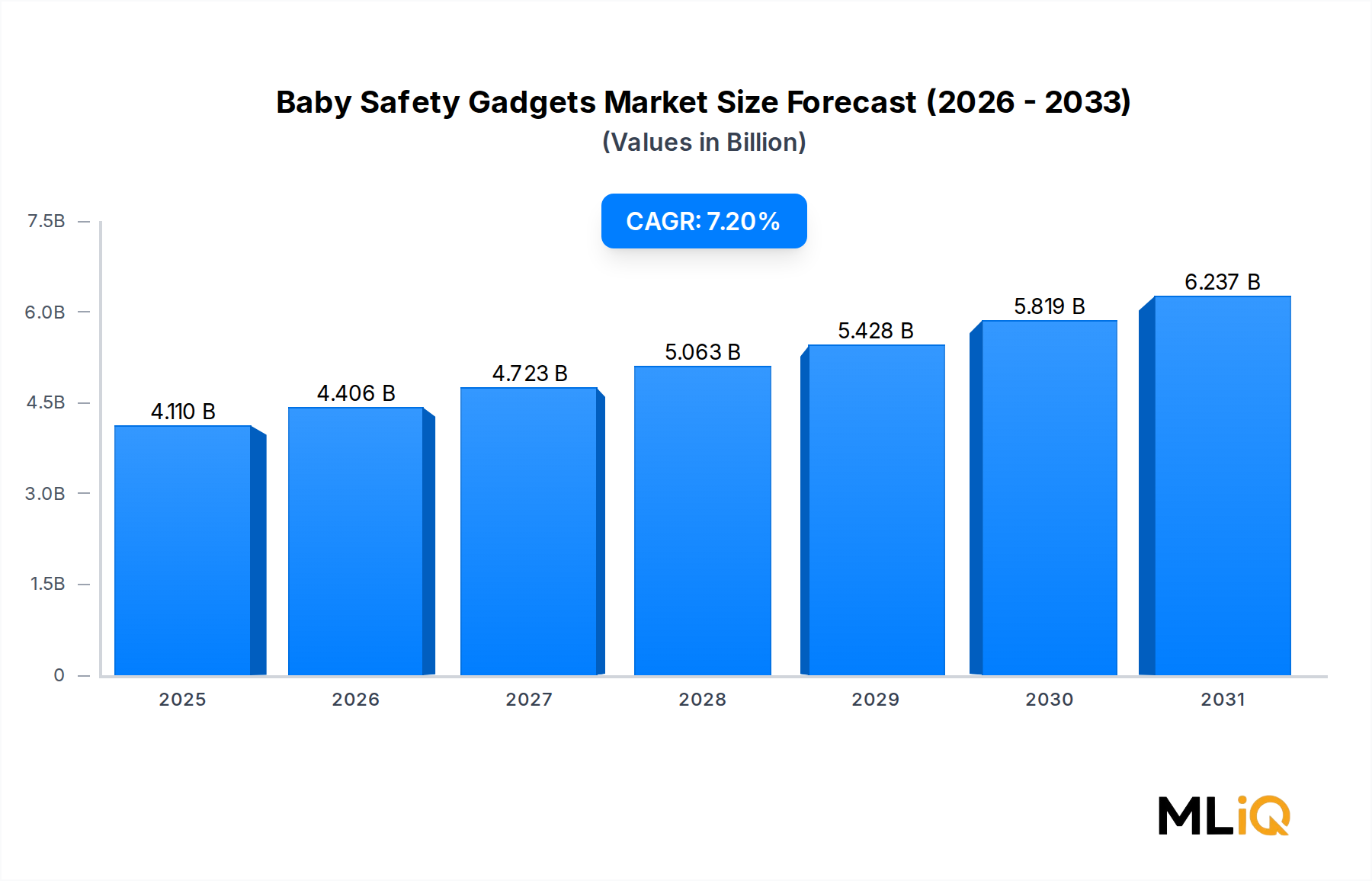

The global Baby Safety Gadgets Market is valued at $4.11 billion in the base year and is projected to expand at a compound annual growth rate of 7.2% through the forecast period of 2025 to 2033. This trajectory reflects sustained momentum driven by rising parental awareness, increasing disposable incomes across emerging economies, and the accelerating integration of smart connectivity into infant care products.

At its core, the market addresses a fundamental human need: ensuring the safety and well-being of infants and toddlers in domestic, transit, and recreational environments. As dual-income households become the global norm, demand for remote monitoring and automated alert systems has surged, repositioning baby safety gadgets from luxury accessories to household essentials. Parents increasingly seek real-time data on vital signs, ambient conditions, and physical proximity, fueling adoption of cloud-connected devices across all income brackets.

Macro tailwinds reinforcing this growth include expanding middle-class populations in Asia Pacific, Latin America, and the Middle East, where urbanization is driving demand for modern childcare solutions. In North America and Europe, regulatory tightening around infant product safety standards has catalyzed product innovation, pushing manufacturers toward sensor-grade precision and certified materials. These regulatory mandates not only raise the quality floor but also create barriers to entry that favor established brands with compliance infrastructure.

Technological convergence is a defining theme. The integration of artificial intelligence, machine learning-based anomaly detection, and edge computing into baby safety devices has dramatically elevated the functional ceiling of the market. Products that once offered passive monitoring now deliver predictive insights — alerting caregivers before distress escalates rather than after. This shift from reactive to proactive safety paradigms is attracting premium-tier spending, with consumers willing to pay significantly above the market average for clinically validated solutions.

E-commerce expansion has also played a transformative role. Online sales channels now account for a growing plurality of total market revenue, enabling global brands to reach consumers in tier-2 and tier-3 cities that lack specialty retail infrastructure. Direct-to-consumer models are compressing distributor margins while simultaneously enabling richer post-purchase engagement through subscription-based monitoring services.

Looking ahead to 2033, the Baby Safety Gadgets Market is expected to be shaped by further miniaturization of biosensors, the mainstreaming of 5G-enabled real-time streaming, and the proliferation of interoperable smart home ecosystems. The convergence of infant safety with broader connected home platforms will blur traditional category boundaries, creating cross-selling opportunities for manufacturers with diversified product portfolios. Investment activity — both in venture capital and strategic M&A — is anticipated to intensify as incumbents seek to acquire AI and sensor competency to defend market position.

Among all product segments within the Baby Safety Gadgets Market, the Baby Monitor segment commands the largest revenue share and continues to consolidate its leadership position. This dominance stems from a combination of high purchase frequency, broad demographic appeal, recurring software and subscription revenue streams, and continuous innovation cycles that sustain consumer upgrade behavior.

Baby monitors represent the most universally adopted category of infant safety technology. Unlike smart car seats or pool alarms — which serve situational or lifestyle-specific needs — a baby monitor is regarded as a standard component of nursery infrastructure across virtually all socioeconomic cohorts. The category spans a wide price spectrum, from entry-level audio monitors retailing below $30 to AI-powered, HD video platforms exceeding $400, making it accessible to both economical and premium segments simultaneously.

The technological evolution of the baby monitor segment has been particularly rapid. First-generation RF audio monitors have given way to Wi-Fi-connected HD cameras with two-way audio, night vision, temperature sensing, and motion detection. The latest generation of monitors incorporates dedicated biosensor modules that track infant breathing patterns, heart rate, and blood oxygen levels — capabilities that were previously confined to clinical neonatology environments. This clinical-grade functionality has been the primary driver of average selling price inflation within the segment, with premium tier products growing faster than the broader category.

Key players anchoring the Baby Monitor segment include Owlet Care, which has built a differentiated position through its smart sock biosensor platform that integrates oxygen saturation and heart rate monitoring into a consumer-friendly wearable. Nanit has emerged as a formidable competitor with its overhead camera and computer vision-based breathing motion monitoring system, paired with a subscription analytics service that tracks sleep patterns over time. Baby sense has maintained a strong foothold in budget-conscious markets through reliable RF and DECT-protocol audio monitors, while Philips leverages its healthcare brand equity to command trust in hospital-adjacent consumer segments.

The Baby Monitor Market is a directly adjacent and increasingly overlapping category with the Baby Safety Gadgets Market, as monitor-integrated platforms expand their functional scope to include environmental sensing, crib safety alerts, and smart home integrations. This blurring of boundaries means that the Baby Monitor segment effectively anchors the broader market's revenue base while simultaneously acting as a platform for adjacent upsell opportunities.

Distribution dynamics within the baby monitor segment favor online channels heavily. E-commerce platforms enable detailed feature comparisons, user review aggregation, and bundled service promotions — all of which disproportionately benefit technically complex products like smart monitors. Owlet and Nanit in particular have built direct-to-consumer digital ecosystems that generate recurring subscription revenue, improving lifetime customer value and reducing dependence on retail margin-sharing.

Geographically, North America and Western Europe represent the highest-revenue sub-markets for premium baby monitors, driven by high smartphone penetration, robust broadband infrastructure, and strong cultural emphasis on data-driven parenting. However, the fastest growth in monitor adoption is occurring in South Korea, China, and urban India, where rising birth rates among educated urban professionals are creating a new cohort of technology-forward parents willing to invest in premium infant monitoring solutions.

The segment's share within the Baby Safety Gadgets Market is expected to remain dominant through 2033, supported by continuous product refresh cycles, expanding subscription revenue models, and the integration of AI-driven pediatric health insights that deepen consumer lock-in.

Several quantifiable forces are shaping the growth trajectory and structural dynamics of the Baby Safety Gadgets Market, spanning demand stimulants and headwinds that market participants must navigate strategically.

Rising parental safety awareness constitutes the most powerful demand driver. Global surveys consistently indicate that over 70% of new parents in developed markets research infant safety products before their child's birth, and the average household safety gadget expenditure per infant has increased by approximately 15–18% over the past five years. This behavioral shift is reinforced by social media communities where parenting influencers amplify awareness of preventable infant hazards, creating virally driven demand spikes for specific product categories.

Increasing urbanization is a structural macroeconomic driver. As of 2024, over 56% of the global population resides in urban areas, a figure projected to reach 68% by 2050. Urban living environments — characterized by elevated ambient pollution, higher vehicular traffic density, and apartment-scale living — create specific safety demands that Baby Safety Gadgets directly address, including air quality monitors, smart stroller proximity alerts, and compact pool and bath safety sensors.

Regulatory catalysts are driving mandatory adoption in several geographies. The European Union's revised General Product Safety Regulation (GPSR), fully effective from December 2024, imposes stricter conformity assessment requirements on connected baby devices, effectively requiring manufacturers to invest in certified safety testing infrastructure. This regulatory pressure, while initially increasing compliance costs, is accelerating market consolidation around compliant brands and driving replacement cycles as non-compliant legacy products are phased out.

On the restraint side, high price sensitivity in price-elastic emerging markets limits penetration of premium devices. In markets such as India, Indonesia, and Sub-Saharan Africa, where average household incomes remain below thresholds for discretionary infant tech spending, adoption rates for smart baby safety gadgets remain in low single digits relative to total birth cohorts. This structural affordability gap constrains total addressable market expansion in otherwise high-volume demographic geographies.

Data privacy concerns represent an emerging constraint. Connected baby monitors that continuously stream audio and video data to cloud servers have been subject to high-profile security breach incidents, eroding consumer trust in specific brands. Regulatory attention to children's data protection — including COPPA in the United States and GDPR Article 8 provisions in Europe — is adding compliance complexity for IoT-connected baby device manufacturers.

The Baby Safety Gadgets Market features a moderately fragmented competitive landscape in which global consumer electronics brands, specialized infant safety companies, and agile direct-to-consumer startups coexist and compete across product tiers and regional markets.

Baby sense: A well-established brand in the infant monitor and movement sensing category, Baby sense focuses on under-mattress breathing movement monitors and offers products distributed widely across European and Asian retail channels, competing primarily on clinical credibility and pediatric endorsement.

Owlet Care: Owlet Care has differentiated its market position through FDA-cleared biosensor wearable technology, with its smart sock product offering pulse oximetry monitoring for infants. The company operates a subscription-based health insights platform that generates recurring revenue beyond hardware sales.

Nanit: Nanit competes at the premium end of the baby monitor sub-segment by combining overhead HD camera hardware with proprietary computer vision algorithms that track infant sleep quality and breathing motion, paired with a subscription analytics membership that deepens long-term customer engagement.

babymoov group: babymoov group is a France-based company offering a broad portfolio of nursery products including video baby monitors, sound machines, and infant safety accessories, with particularly strong retail penetration across Western Europe and growing e-commerce presence globally.

Safe-o-Kia (Baby Safety Inc.): Safe-o-Kia positions itself as a specialist in passive and active home safety solutions for infants, including cabinet locks, stair gates, and outlet covers, targeting budget-conscious and first-time parent demographics in North American and Asian markets.

Philips: Philips leverages its global healthcare brand and extensive consumer electronics distribution network to offer baby monitors and nursing accessories that carry a premium trust premium, with product lines marketed through both retail pharmacy and specialty baby store channels.

Summer Infant Inc: Summer Infant Inc is a comprehensive infant product company offering safety gates, monitors, and feeding accessories, with a strong retail presence in North American mass-market channels and a growing digital commerce footprint.

BT: BT, operating in the baby monitor segment under its consumer electronics division, offers DECT-protocol digital audio and video monitors primarily for the United Kingdom market, competing on channel heritage and affordable pricing.

Munchkin, Inc: Munchkin, Inc operates across multiple infant product categories including safety gadgets, bathing accessories, and feeding products, using broad retailer relationships and aggressive product innovation cadences to maintain shelf presence in competitive mass-market environments.

Sunza: Sunza is an emerging direct-to-consumer brand specializing in smart baby safety devices including AI-integrated monitors and environmental sensors, gaining traction through digital marketing channels and competitive pricing strategies targeting millennial and Gen Z parents.

January 2025: Owlet Care received expanded FDA clearance for its third-generation smart sock, extending pediatric monitoring capabilities to infants up to 18 months of age and enabling integration with hospital discharge monitoring programs.

March 2025: Nanit announced a strategic partnership with a leading U.S. pediatric health network to integrate its AI sleep analytics platform into post-natal care protocols, marking the company's first clinical channel distribution arrangement.

May 2025: The European Commission published updated safety testing guidelines under GPSR specifically addressing connected infant monitoring devices, requiring all IoT-enabled baby safety products to undergo mandatory cybersecurity certification before EU market placement.

July 2024: babymoov group launched its next-generation Yoo-Feel premium baby monitor featuring integrated air quality sensing, temperature and humidity monitoring, and cloud-connected parent app, targeting the growing demand for multi-function nursery safety hubs.

September 2024: Summer Infant Inc announced the discontinuation of its legacy analog baby monitor product line, completing its portfolio transition to fully digital and Wi-Fi-connected devices in response to shifting consumer preferences and regulatory pressure.

November 2024: A major venture capital consortium announced a $45 million Series B investment in an AI-powered infant biosensor startup, signaling continued investor conviction in the clinical-grade consumer baby safety technology segment.

February 2025: Munchkin, Inc unveiled a new line of smart bathroom safety gadgets integrating water temperature alerts and bath overflow sensors, expanding its safety gadget footprint beyond its core feeding accessories heritage.

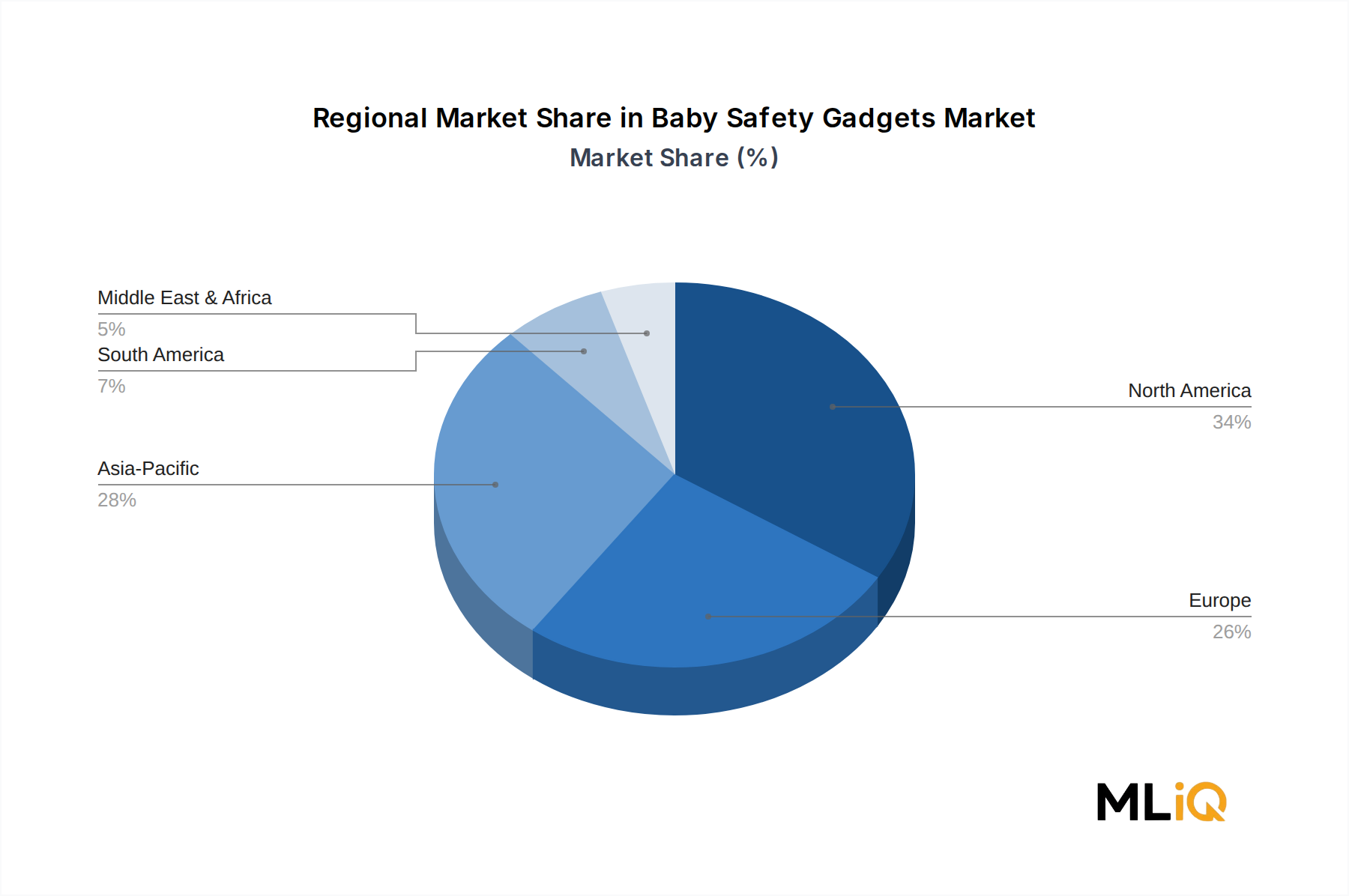

The global Baby Safety Gadgets Market exhibits meaningful regional differentiation across revenue concentration, growth velocity, and dominant product preferences, reflecting divergent income profiles, regulatory environments, and consumer behavior patterns.

North America remains the most mature and highest-revenue regional market, accounting for an estimated 34–36% of global Baby Safety Gadgets Market revenue. The United States is the primary contributor, driven by high per-capita infant safety expenditure, robust e-commerce infrastructure, and strong brand ecosystems built around companies such as Owlet Care, Nanit, and Summer Infant Inc. Canada and Mexico represent secondary markets with growing demand, particularly in urban centers. The North American market is characterized by premium-tier dominance, regulatory-driven product upgrades, and high repeat purchase rates as parents upgrade to next-generation connected devices. The regional CAGR for North America is estimated at 5.8–6.2% through 2033.

Europe represents the second-largest regional market, with an estimated revenue share of 26–28% and a CAGR of approximately 6.5%. Germany, the United Kingdom, and France anchor European demand, with strong retail channels through specialty baby stores and pharmacy chains. The implementation of GPSR and stringent EN-standard safety certifications has elevated product quality benchmarks, creating a compliance-driven competitive moat for established brands including Philips and babymoov group. The Nordic countries exhibit particularly high per-household infant safety gadget penetration, supported by high disposable incomes and parental leave culture.

Asia Pacific is the fastest-growing regional market, projected to achieve a CAGR of 9.1–9.8% through 2033, significantly outpacing the global average. China, India, Japan, and South Korea collectively drive regional volume, with China and India contributing the most incremental growth due to their large annual birth cohorts and rapidly expanding urban middle classes. South Korea exhibits the highest technology adoption intensity, with AI-enabled monitors achieving mainstream penetration. The region's growth is further supported by government child welfare programs in India and China that are beginning to incorporate infant safety technology awareness campaigns.

South America is an emerging market with a CAGR of approximately 7.4%, led by Brazil and Argentina. Rising middle-class formation and expanding e-commerce logistics infrastructure are the primary growth catalysts. The Middle East and Africa region presents uneven development, with GCC countries — particularly Saudi Arabia and the UAE — demonstrating strong premium-tier demand, while Sub-Saharan Africa remains at nascent adoption stages. The GCC's high expatriate population density and high household income concentration support above-average per-unit spending on infant safety devices.

The supply chain underpinning the Baby Safety Gadgets Market is complex and geographically concentrated, with significant upstream dependencies on a small number of critical input categories whose availability and pricing directly influence product economics and margin profiles.

Semiconductors constitute the most strategically critical input. Baby safety gadgets — particularly smart monitors, biosensor wearables, and IoT-connected detectors — rely on microcontrollers, application processors, wireless communication chipsets (Wi-Fi, Bluetooth, Zigbee), and analog front-end sensor ICs. The 2021–2023 global semiconductor shortage demonstrated the acute vulnerability of this supply chain, with multiple baby gadget manufacturers reporting product launch delays of 6–12 months and average chip procurement cost increases of 30–45% during peak shortage periods. While supply has partially normalized, geopolitical risks related to Taiwan Strait tensions and U.S.-China export controls continue to create latent vulnerability for manufacturers relying on TSMC and MediaTek for core chipsets.

Lithium-ion battery cells represent the second major input risk. Rechargeable baby devices — including wearable biosensors and portable monitors — depend on lithium-

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Baby Safety Gadgets Market market expansion.

Key companies in the market include Baby sense, Owlet Care, Nanit, babymoov group, Safe-o-Kia (Baby Safety Inc.), Phillips, Summer Infant Inc, BT, Munchkin, Inc, Sunza.

The market segments include Product type, Price Range, Distribution Channel.

The market size is estimated to be USD 4.11 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Baby Safety Gadgets Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Baby Safety Gadgets Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.