1. What are the major growth drivers for the Coffee Pod Market market?

Factors such as are projected to boost the Coffee Pod Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

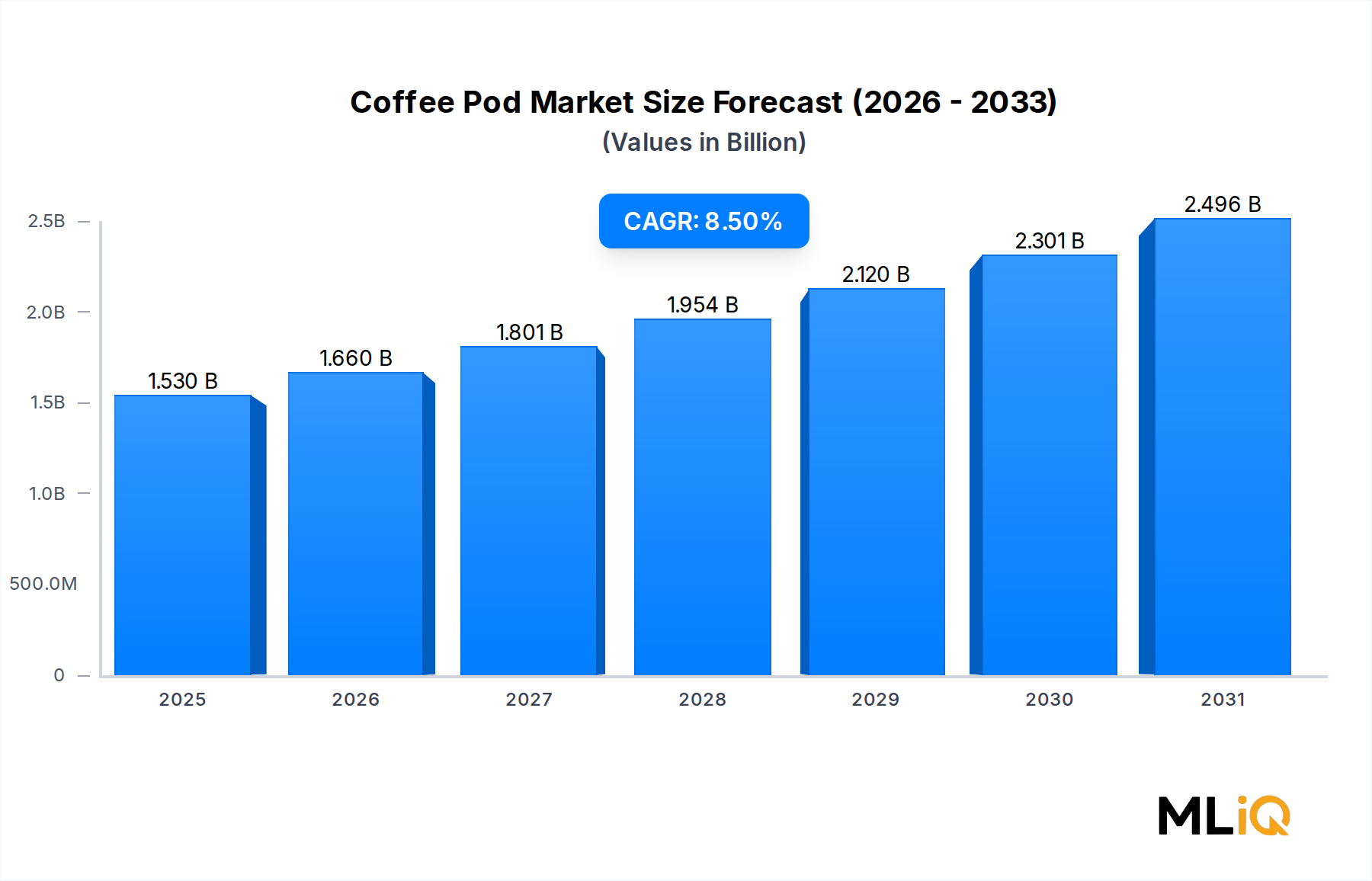

The global Coffee Pod Market was valued at $1.53 billion in the base year and is projected to expand at a compound annual growth rate of 8.5% through 2033, reflecting strong and sustained consumer appetite for convenient, single-serve coffee formats. This trajectory positions the market to more than double its current valuation over the forecast horizon, driven by a convergence of lifestyle shifts, premiumization trends, and expanding retail infrastructure across both mature and emerging economies.

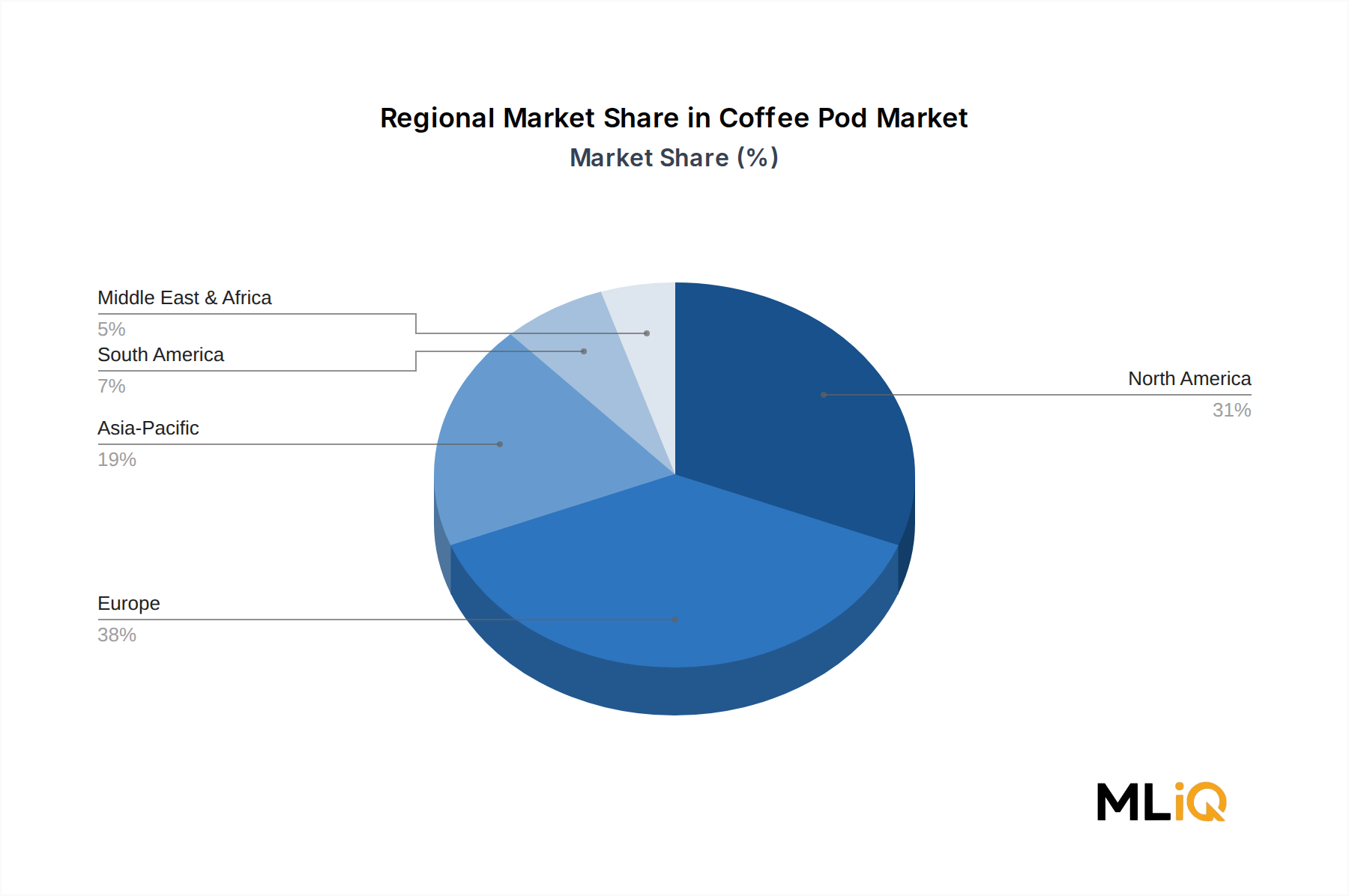

At its core, the Coffee Pod Market is being propelled by the accelerating "at-home café" culture, which gained decisive momentum during the global pandemic and has since become a durable behavioral shift. Consumers who previously relied on foodservice channels for specialty espresso and flavored coffee beverages have invested heavily in home brewing equipment, creating a reinforcing cycle of machine penetration and pod consumption. This dynamic is particularly pronounced in North America and Western Europe, where single-serve brewing systems now account for a substantial share of household coffee equipment.

Demand segmentation reveals that caffeinated pods continue to dominate volumetrically, though decaffeinated variants are growing at an above-average pace as health-conscious consumers seek to moderate stimulant intake without sacrificing the ritual of coffee consumption. Flavor innovation — spanning caramel, hazelnut, and dark chocolate profiles — is a primary lever through which manufacturers are differentiating their product lines and capturing premium price points.

From a distribution standpoint, the online channel has emerged as a structurally important growth vector. Subscription-based pod delivery services have demonstrated strong customer retention metrics and allow brands to collect granular consumption data, enabling targeted flavor launches and loyalty programs. Hypermarkets and supermarkets retain the highest absolute revenue share, but their growth rate is being eclipsed by e-commerce platforms.

Macro tailwinds supporting the 8.5% CAGR include rising disposable incomes in Asia Pacific markets, urbanization-driven demand for quick-preparation beverages, and the proliferation of compact espresso systems in smaller living spaces. Simultaneously, the market faces headwinds from sustainability scrutiny — single-use plastic and aluminum pods are under increasing regulatory and consumer pressure, compelling manufacturers to accelerate investment in compostable and recyclable formats.

Looking ahead to 2033, the competitive landscape is expected to consolidate around brands that can credibly combine premium sensory quality with credible environmental stewardship. The intersection of specialty roasting heritage and scalable pod technology will define the next generation of market leaders.

Among all segmentation dimensions analyzed within the Coffee Pod Market, the caffeinated segment under the caffeine concentration axis commands the largest revenue share, and its dominance is reinforced by deeply entrenched consumer preferences, physiological demand patterns, and the global cultural centrality of caffeine as a functional ingredient in daily coffee rituals.

Caffeinated pods account for the overwhelming majority of total units sold across all distribution channels and geographies. This is not merely a function of habit — it reflects the foundational value proposition of coffee as an alertness-enhancing, performance-supporting beverage. In commercial end-use environments such as offices, hotels, and foodservice establishments, caffeinated pods are essentially the default specification, as operators prioritize alignment with the expectations of the broadest possible consumer demographic.

Within the caffeinated segment, flavor sub-segmentation is the primary battleground for market share. Caramel-flavored pods have demonstrated particularly strong traction in North America, where sweet, dessert-adjacent coffee profiles enjoy broad consumer acceptance. Chocolate-infused pods perform robustly in European markets, especially in Germany, France, and Italy, where confectionery-coffee hybrids have deep cultural resonance. Hazelnut remains a perennial top-seller globally, benefiting from its association with premium Italian-style café experiences.

Key players anchoring the caffeinated segment include illycaffè S.p.A., whose mono-origin and single-estate caffeinated pod lines command significant premium positioning, and Lavazza Group, which leverages its century-long roasting heritage to market caffeinated pods as an authentic Italian espresso experience in convenient format. Caffe Borbone S.r.l. and Kimbo S.p.A. have both invested heavily in expanding their caffeinated pod portfolios to address the mid-market segment, where value-for-money without quality compromise is the dominant purchase driver.

The caffeinated segment's share is not merely holding steady — it is consolidating. As pod machines proliferate in lower-income household tiers, the entry of price-sensitive consumers into the category skews volume toward standard caffeinated offerings rather than premium decaffeinated or specialty variants. Private-label caffeinated pods, distributed through hypermarkets and supermarkets, have grown significantly in Western Europe, pressuring branded players to invest in quality differentiation and packaging premiumization to justify price premiums.

Commercial end-use accounts for a disproportionate share of caffeinated pod consumption relative to its unit count, as foodservice and office operators purchase in higher volumes and at more regular intervals than residential consumers. This channel dynamic makes commercial accounts strategically critical for major players, who often deploy dedicated salesforces and machine-plus-pod bundling strategies to secure long-term supply agreements.

From an innovation standpoint, the caffeinated segment is seeing increasing activity around intensity gradation — pods are now marketed across a spectrum from mild to extra-strong, allowing consumers to calibrate their caffeine intake with precision. This granularity of choice is particularly appealing to millennial and Gen Z consumers who engage with coffee as a lifestyle category rather than merely a functional morning ritual.

The caffeinated flavor segment's dominance is therefore structural rather than cyclical, and its growth trajectory is expected to remain positive throughout the forecast period to 2033, even as decaffeinated and functional variants carve out expanding niches.

The Coffee Pod Market is subject to a well-defined set of demand drivers and structural constraints, each of which can be quantified against observable market and macroeconomic data.

The primary driver is the global surge in at-home coffee consumption. Single-serve brewing machine penetration in the United States exceeded 35% of coffee-drinking households by the mid-2020s, creating a large and captive installed base that generates recurring pod demand. Each machine owner represents an annualized pod consumption rate that is measurably higher than that of drip or French press users, given the format's encouragement of multi-cup daily usage.

Rising urbanization in Asia Pacific is a second material driver. With urban populations in China, India, and Southeast Asia growing by tens of millions annually, the addressable market for coffee pod consumption is expanding at a pace that is structurally disconnected from traditional coffee-drinking regions. Pod formats are particularly well-suited to urban Asian consumers because of their compact footprint, minimal preparation time, and alignment with aspirational Western lifestyle aesthetics.

Premiumization represents a third identifiable driver. Average selling prices for coffee pods in the specialty and single-origin sub-segments have risen by a meaningful margin over the past five years, as consumers demonstrate willingness to pay for certified organic, rainforest alliance, and direct-trade provenance claims. This pricing power supports revenue growth that is additive to volume growth, amplifying the CAGR trajectory.

On the constraint side, environmental regulation is the most material headwind. The European Union's Single-Use Plastics Directive and corresponding national-level packaging regulations in Germany, France, and the UK are imposing compliance costs and reformulation timelines on pod manufacturers that rely on conventional polypropylene or multi-layer aluminum-plastic constructions. Non-compliance risks include retail de-listing and reputational damage among ESG-sensitive consumer cohorts.

Raw material cost volatility is a second constraint. Coffee bean commodity prices are subject to climatic and geopolitical disruption, and aluminum — a primary pod material — has experienced significant price swings due to energy cost fluctuations in smelting markets. These input cost pressures compress manufacturer margins and can translate into retail price increases that moderate volume demand.

The competitive landscape of the Coffee Pod Market is characterized by a mix of Italian heritage roasters, multinational food and beverage conglomerates, and specialist single-serve manufacturers. The following profiles outline the strategic positioning of the primary companies active in this space:

Gruppo Gimoka S.p.A.: A leading Italian private-label and branded coffee pod manufacturer with extensive OEM relationships across European retail chains. The company's competitive advantage lies in its high-throughput production capacity and ability to serve both premium and value price tiers simultaneously.

Labcaffè S.r.l.: Specializes in compatible pod systems designed to work across multiple machine platforms, giving it broad retail addressability. Its R&D focus on compostable pod materials positions it favorably against tightening European packaging regulations.

Procaffé S.p.A.: An Italian roaster with a strong emphasis on traditional espresso blends packaged in ESE (Easy Serving Espresso) pod format. The company targets the horeca channel as its primary commercial avenue.

Lavazza Group: One of Italy's most globally recognized coffee brands, with a pod portfolio spanning multiple machine-compatible formats. Lavazza's investment in sustainability-certified supply chains and its global distribution network give it significant scale advantages.

Blasercafé AG: A Swiss specialty roaster whose pod offerings occupy the ultra-premium segment. Blasercafé differentiates through single-origin provenance and micro-roast batch programs that appeal to connoisseur consumers.

Segafredo Zanetti S.p.A.: Part of the Massimo Zanetti Beverage Group, Segafredo operates across foodservice and retail channels with a diversified pod portfolio. Its global café franchise network provides a direct-to-consumer feedback loop that informs product development.

Gruppo Izzo S.r.l.: A manufacturer with deep roots in professional espresso machine engineering, whose pod products benefit from technical alignment with commercial machine specifications. This positions Gruppo Izzo strongly in the high-end commercial end-use segment.

Caffe Borbone S.r.l.: One of the fastest-growing Italian pod brands, known for its Neapolitan-style espresso intensity and highly competitive retail pricing. Caffe Borbone has rapidly expanded its e-commerce presence and subscription service infrastructure.

Kimbo S.p.A.: A Naples-based roaster with strong brand equity in Southern Italy that is actively expanding its pod distribution into Northern European and North American markets. Kimbo's marketing strategy emphasizes authenticity and geographic origin.

illycaffè S.p.A.: The global benchmark for premium single-origin espresso pods. illycaffè's vertically integrated supply chain, direct relationships with growers across nine countries, and commitment to research through its university of coffee distinguish it as the quality leader in the segment.

March 2024: Lavazza Group announced the commercial launch of its fully compostable EvoCaps pod line across twelve European markets, marking a significant milestone in the transition away from conventional aluminum pod formats.

June 2024: illycaffè S.p.A. entered a strategic partnership with a major e-commerce logistics provider to expand same-day pod delivery coverage to tier-one cities across Germany, France, and the United Kingdom.

September 2024: Caffe Borbone S.r.l. reported a 40% year-over-year increase in online subscription revenue, validating its strategic pivot toward direct-to-consumer digital channels initiated in 2022.

November 2024: The European Parliament advanced amendments to the Packaging and Packaging Waste Regulation (PPWR) that specifically address multi-layer coffee pod materials, setting a compliance deadline that will require manufacturers to achieve 90% recyclability or compostability by 2030.

January 2025: Kimbo S.p.A. signed a distribution agreement with a North American grocery retail chain, marking its formal entry into the United States market with a dedicated Nespresso-compatible pod range.

April 2025: Blasercafé AG unveiled a blockchain-enabled provenance tracking system for its premium pod range, allowing consumers to trace coffee origin to the individual farm level via QR code on packaging.

May 2025: Gruppo Gimoka S.p.A. completed the acquisition of a Spanish private-label pod manufacturer, expanding its Southern European production footprint and increasing annual capacity by an estimated 25%.

The Coffee Pod Market faces some of the most acute sustainability scrutiny of any consumer packaged goods segment, owing to the single-use nature of its core product format. The environmental debate centers on three interconnected issues: material recyclability, composting infrastructure compatibility, and carbon intensity across the supply chain.

Conventional pods — whether constructed from polypropylene plastic or aluminum-foil laminates — present significant end-of-life challenges. Consumers in most markets lack access to industrial composting facilities capable of processing certified compostable pods within the required timeframes, meaning that even technically compliant "compostable" products frequently end up in landfill. This infrastructure gap is forcing pod manufacturers to reassess their sustainability claims and engage with municipal waste authorities to advocate for expanded composting collection programs.

The EU's PPWR and the UK's Extended Producer Responsibility (EPR) framework are imposing measurable financial obligations on pod manufacturers operating in European markets. EPR fees, which are calibrated to material recyclability scores, are creating direct cost incentives to reformulate pod materials. Companies that delay reformulation face escalating fee structures that could reach tens of millions of euros annually at scale.

ESG investor pressure is amplifying regulatory mandates. Institutional investors applying Environmental, Social, and Governance screening criteria are increasingly scrutinizing the packaging practices of companies in the Single Serve Coffee Market and the broader Hot Beverage Market. Annual sustainability reports that lack quantified reduction targets for pod material waste are receiving negative scoring from major ESG rating agencies, affecting cost of capital for publicly listed players.

In response, the industry is investing in three primary solution pathways: (1) certified industrially compostable biopolymer pods, (2) aluminum pods with closed-loop recycling take-back programs, and (3) reusable refillable pod systems that eliminate single-use waste entirely. The third pathway has gained notable traction in the Food Packaging Market more broadly, and its adoption within the pod category is being monitored closely by retailers who face their own scope-3 emissions reporting obligations.

The Biodegradable Packaging Market is directly implicated in these developments, as pod manufacturers are among the highest-volume buyers of next-generation biodegradable film and barrier materials. The performance requirements for coffee pods — oxygen impermeability, moisture resistance, and compatibility with high-temperature brewing — remain technically demanding, and the premium cost of biodegradable alternatives continues to suppress widespread adoption among value-tier pod brands.

The Coffee Pod Market is at an inflection point driven by three technology vectors that are simultaneously disrupting incumbent manufacturing models and creating new sources of competitive differentiation.

The first and most commercially advanced technology is precision nitrogen-flush sealing, which extends the shelf-stable freshness window of pods significantly beyond conventional atmospheric sealing methods. By displacing oxygen within the pod chamber with an inert gas at the point of sealing, manufacturers can guarantee aromatic integrity for up to 24 months post-production — a meaningful commercial advantage for brands operating long international distribution chains. Investment in nitrogen-flush sealing lines has increased substantially across Italian pod manufacturing clusters, and the technology is now considered table stakes for premium pod positioning. The Espresso Machine Market has directly responded to this trend, with machine manufacturers engineering brew chambers optimized for the specific pressure profiles generated by nitrogen-flushed pods.

The second disruptive technology is smart pod integration — embedding machine-readable data matrices or RFID tags directly into pod packaging to enable dynamic brewing parameter adjustment. When a pod is inserted into a compatible machine, the system reads the pod's embedded data and automatically configures water temperature, pressure, and extraction time for optimal results. This technology, currently in early commercial deployment, creates powerful lock-in effects that reinforce the proprietary Coffee Capsule Market dynamics that have historically characterized closed-system brewing platforms. R&D investment in smart pod systems is estimated to be accelerating at a double-digit annual rate among tier-one manufacturers.

The third technology vector is AI-driven flavor personalization at scale. Using purchase history data collected through connected machines and subscription platforms,

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Coffee Pod Market market expansion.

Key companies in the market include Gruppo Gimoka S.p.A., Labcaffè S.r.l., Procaffé S.p.A., Lavazza Group, Blasercafé AG, Segafredo Zanetti S.p.A., Gruppo Izzo S.r.l., Caffe Borbone S.r.l., Kimbo S.p.A., illycaffe S.p.A..

The market segments include Flavor, Distribution Channel, Caffeine Concentration, End Use.

The market size is estimated to be USD 1.53 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Coffee Pod Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Coffee Pod Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.