1. What are the major growth drivers for the Lens Cleaning Cloths Market market?

Factors such as are projected to boost the Lens Cleaning Cloths Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

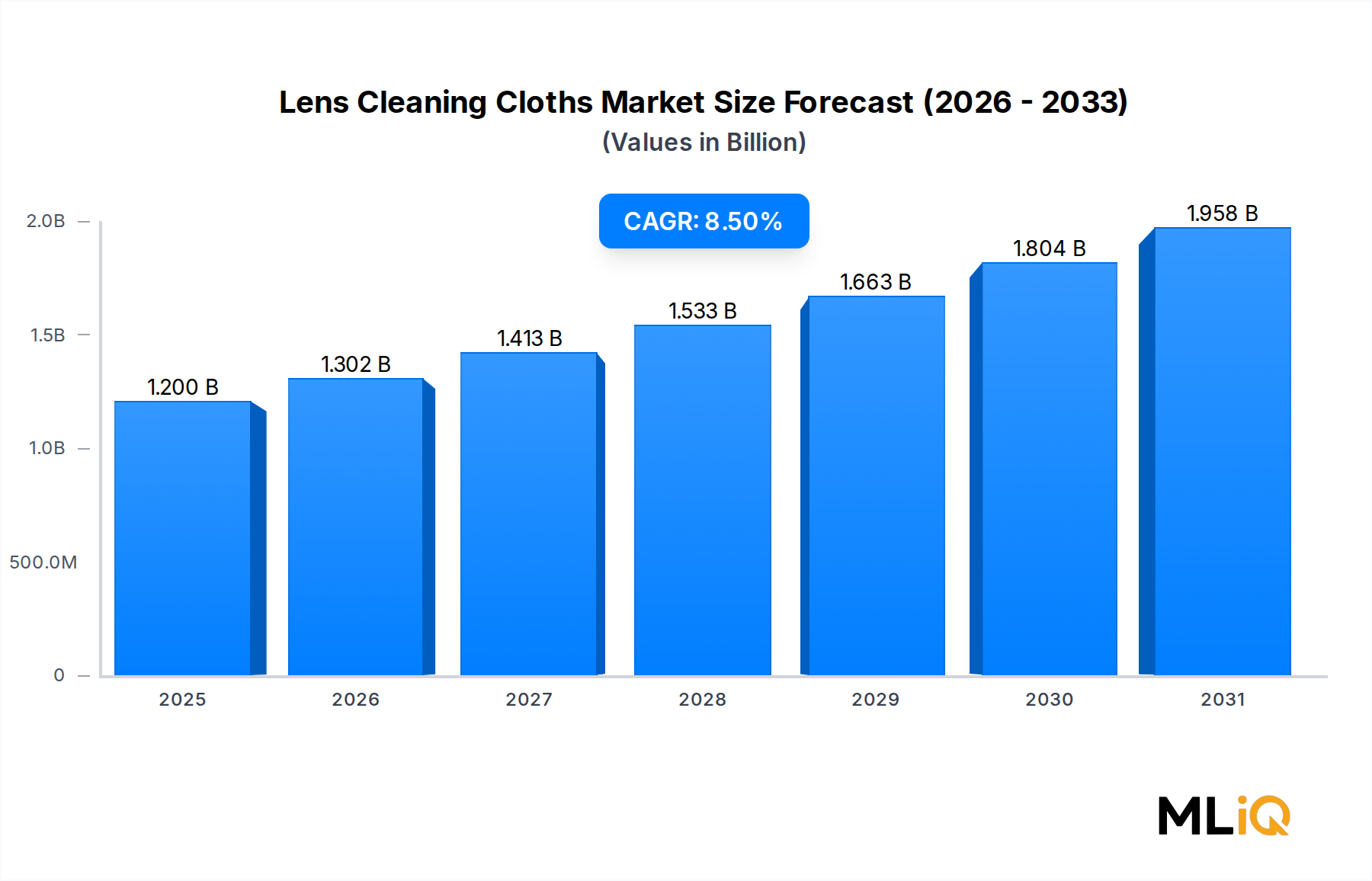

The global Lens Cleaning Cloths Market was valued at $1.2 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 8.5% through 2033, reflecting robust consumer and institutional demand for precision optical hygiene solutions. This trajectory implies the market will approach approximately $2.3 billion by the end of the forecast period, driven by a confluence of demographic, technological, and behavioral factors reshaping how individuals and professionals care for optical surfaces.

A primary macro tailwind is the global rise in vision correction adoption. The World Health Organization estimates that over 2.2 billion people worldwide experience near or distance vision impairment, with a significant proportion relying on prescription eyewear — a direct end-user base for lens cleaning products. Simultaneously, surging screen time across all age groups, particularly among Gen Z and millennial consumers, is generating persistent demand for screen and lens hygiene solutions that minimize visual fatigue and maintain optical clarity.

The proliferation of premium eyewear brands and high-index lens coatings — including anti-reflective, blue-light filtering, and hydrophobic treatments — has elevated consumer sensitivity to cleaning material quality. Standard paper tissues or synthetic cloths risk micro-scratching delicate coatings, accelerating the shift toward purpose-engineered microfiber and specialty wet wipe formats. This premiumization trend is sustaining above-average unit price growth even as competitive pressures intensify in mass-market retail channels.

The camera photography and professional optics segment is contributing incremental demand, with DSLR, mirrorless, and cinema-grade lens ownership rising in both hobbyist and commercial markets. Laboratory and healthcare environments further reinforce adoption, as regulatory and safety standards increasingly mandate contamination-free optical instruments.

E-commerce penetration is a structural enabler. Leading platforms are democratizing access to specialty cleaning cloths previously limited to optical retail or professional supply chains. Subscription-based dispensing models and bundled cleaning kits are emerging as high-margin growth vectors for both established brands and direct-to-consumer entrants.

Geographically, Asia Pacific represents the fastest-growing regional market, underpinned by rising middle-class eyewear adoption in China and India, while North America maintains the largest absolute revenue share. Europe continues to benefit from stringent optical quality standards in both consumer and professional segments.

Looking ahead, product innovation centered on antimicrobial treatments, biodegradable fiber composition, and nanotextile engineering will serve as key differentiators. Brands that align sustainability credentials with functional performance are positioned to capture outsized share in environmentally-conscious consumer cohorts.

Among the two primary product type segments — wet wipes and dry wipes — the dry wipes sub-segment has historically commanded the largest revenue share within the Lens Cleaning Cloths Market, a position that continues to consolidate as product engineering sophistication increases and consumer preference for reusable, low-waste solutions gains momentum.

Dry lens cleaning cloths, predominantly constructed from ultra-fine microfiber blends of polyester and polyamide, dominate for several structural reasons. First, they are inherently multi-use, offering consumers a cost-per-clean advantage that disposable wet wipes cannot match. A single high-quality microfiber cloth can withstand hundreds of wash cycles while maintaining its fiber density and electrostatically charged surface architecture — the mechanism by which it lifts oils, particulates, and smear residue without chemical assistance. This reusability aligns powerfully with growing sustainability mandates in European and North American retail markets.

Second, dry wipes avoid the regulatory complexity associated with wet wipes, which contain preservatives, surfactants, and biocidal agents subject to cosmetic and chemical product regulations across multiple geographies. This regulatory simplicity accelerates dry cloth product launches and retail approvals, reducing time-to-market for both established players and emerging brands.

Third, compatibility with high-value lens coatings is a decisive factor. Anti-reflective, hydrophobic, and oleophobic coatings on premium eyewear lenses are vulnerable to chemical degradation from alcohol or surfactant-laden wet wipes when used repeatedly. Opticians and optical retail staff consistently recommend dry microfiber cloths for daily maintenance, reinforcing a professional endorsement ecosystem that drives consumer trust and repeat purchases.

Key players competing most aggressively in the dry wipes segment include Toray, a Japanese advanced materials manufacturer whose ultra-fine fiber technology sets the performance benchmark in both OEM supply and branded retail; Zeiss wipes (operating under the broader Zeiss optical brand umbrella), which leverages its heritage in precision optics to command premium shelf positioning; and E-cloth, whose sustainability narrative resonates with eco-conscious retail buyers in Western markets.

Velda and Nordex are notable mid-market participants offering competitively priced dry cloth solutions to institutional purchasers such as optical chains, laboratories, and educational institutions. Atlas Graham and Waldron serve the professional and healthcare-adjacent cleaning segment, where contamination control requirements overlap with lens hygiene applications.

The dry wipes segment's share is not merely stable — it is expanding. Consumer research consistently shows growing willingness to pay a premium for cloths marketed with technical fiber specifications (e.g., fiber diameter below 0.5 denier), wash durability certifications, and brand co-endorsements from optical manufacturers. Bundling strategies — wherein premium eyewear brands include a branded microfiber cloth at point of sale — are effectively subsidizing consumer trial and building brand-loyal repeat purchasers.

Product differentiation is intensifying around antimicrobial fiber treatments, with several manufacturers incorporating silver-ion or zinc-oxide nanotechnology into fiber matrices to address hygiene concerns amplified by the COVID-19 pandemic. Color-coding systems for multi-surface use (separate cloths for lenses, screens, and camera optics) are gaining traction in professional and household segments alike, expanding average order value per customer.

Wholesale distribution through optical chains, camera retailers, and laboratory supply companies remains the dominant channel for dry wipes, though e-commerce is rapidly narrowing the gap, particularly in Asia Pacific where platform-based discovery drives significant trial among first-time buyers.

The Lens Cleaning Cloths Market is governed by a set of quantifiable drivers and material constraints that analysts must weigh carefully when constructing demand forecasts.

On the demand side, global eyewear market growth is the single most significant driver. The international eyewear industry exceeded $160 billion in 2024 and is projected to grow at approximately 7% annually through 2030, directly expanding the installed base of lens-bearing devices requiring regular maintenance. Each pair of prescription glasses, sunglasses, or safety eyewear sold represents a recurring cleaning cloth demand unit, given average replacement cycles of three to six months for daily-use cloths.

The proliferation of personal electronic devices is a secondary but rapidly appreciating driver. Global smartphone shipments exceeded 1.2 billion units in 2024, and each device features a glass or coated screen surface that users habitually clean with available cloths — frequently repurposing lens cloths for this function. This behavioral overlap expands the effective addressable market beyond traditional optical segments.

In professional verticals, laboratory and medical imaging equipment operators represent an institutional demand layer with low price sensitivity and high frequency requirements. Healthcare facility procurement standards increasingly specify approved cleaning materials, routing institutional spend toward certified optical-grade cloths.

Constraints include raw material price volatility, particularly for polyester and polyamide fibers — the primary input for microfiber cloths. Petrochemical feedstock disruptions, as observed during 2021–2023, can compress manufacturer margins and delay product launches when fiber costs escalate by 15–25% over short intervals. Suppliers with vertically integrated fiber production, such as Toray, are better insulated from this risk than pure assemblers.

Fragmentation in distribution represents a structural headwind. The market contains hundreds of regional and private-label producers, creating significant price competition in mid-market retail segments and compressing margins for smaller branded players lacking the scale to negotiate favorable shelf placements or e-commerce algorithm positioning.

Consumer mis-education — specifically, the continued use of paper tissues and clothing fabric for lens cleaning — remains a latent constraint on addressable market penetration, particularly in emerging economies where optical retail infrastructure is underdeveloped.

The competitive landscape of the Lens Cleaning Cloths Market is moderately fragmented, with a mix of global optical brands, specialty textile manufacturers, and diversified cleaning product companies.

Velda: A specialized optical accessories manufacturer with a strong European retail footprint, Velda competes on product range breadth and private-label manufacturing partnerships with optical chains.

E-cloth: Positions itself as the sustainability leader in premium microfiber cleaning, leveraging third-party environmental certifications and a direct-to-consumer e-commerce model to command above-average price points.

Toray: A global advanced materials leader, Toray supplies ultra-fine microfiber substrates to numerous branded cloth manufacturers while maintaining its own branded optical cleaning product line in select Asian markets.

Zeiss wipes: Operating as an extension of the Carl Zeiss precision optics brand, Zeiss wipes occupies the premium-to-luxury tier, benefiting from the parent brand's optical credibility to justify elevated retail pricing in optical specialty retail.

Euro: A pan-European cleaning products distributor with diversified category exposure, Euro competes on pricing and distribution network depth across retail chains and institutional supply contracts.

Game: Targets the consumer electronics cleaning segment, frequently bundling cleaning cloths with screen protectors and device accessories through electronics retail channels.

CMA: A mid-tier institutional supplier serving laboratory, education, and professional photography segments, CMA differentiates on bulk packaging formats and volume pricing programs.

Atlas Graham: A professional cleaning textile specialist with deep roots in the hospitality and healthcare cleaning sectors, Atlas Graham applies its industrial textile expertise to optical-grade cloth manufacturing.

Medline: A major healthcare supply company, Medline's presence in lens cleaning cloths is anchored in medical facility procurement channels where validated cleaning material specifications are mandatory.

Aqua Star: Competes primarily in the wet wipe segment, offering pre-moistened optical cleaning solutions to retail pharmacy and consumer electronics channels.

Dish Cloths: Primarily a household cleaning brand that has extended into multi-surface cleaning cloths, including optical applications, targeting value-oriented consumer segments.

Scotch-Brita: A recognized cleaning brand leveraging brand equity in surface care to offer optical cleaning cloth variants in mass retail environments.

Waldron: Focuses on OEM and private-label dry cloth manufacturing, supplying optical retailers and eyewear brands seeking co-branded or house-brand cleaning accessories.

Nordex: A textile manufacturing group active in the technical fabrics space, Nordex supplies specialty microfiber rolls and pre-cut cloths to optical and electronics assembly industries.

Unger: A professional cleaning equipment company whose microfiber product range includes optical-grade cloths marketed through janitorial supply and facilities management channels.

ERC: A regional cleaning products distributor with niche strength in laboratory and precision optics cleaning supply, ERC serves scientific instrument manufacturers and academic research institutions.

January 2025: Toray announced the commercial launch of its next-generation ultra-fine polyester microfiber series, featuring fiber diameters below 0.1 denier, targeting premium optical cloth manufacturers seeking enhanced particulate capture performance.

March 2025: E-cloth received OEKO-TEX STANDARD 100 certification renewal for its full optical cleaning cloth range, reinforcing its sustainable product positioning ahead of European eco-labeling regulatory updates expected in 2026.

April 2025: Zeiss wipes expanded its retail distribution partnership network in Southeast Asia, entering agreements with optical retail chains in Vietnam, Thailand, and Indonesia to address accelerating regional demand.

May 2025: Medline introduced a new antimicrobial-treated lens cleaning cloth specifically validated for medical imaging and ophthalmological instrument maintenance, targeting hospital and clinic procurement officers in North America.

June 2025: A leading e-commerce platform in China reported that lens cleaning cloth unit sales grew 42% year-over-year during its mid-year shopping festival, signaling robust consumer demand acceleration in the Asia Pacific region.

August 2025: Unger announced a strategic distribution agreement with a major European facilities management services group, expanding its microfiber optical cloth reach into commercial building maintenance and corporate office segments.

October 2025: The global eyewear retail association published updated lens care guidelines recommending frequency-of-cleaning best practices, implicitly endorsing dedicated microfiber cloths over disposable alternatives — a development expected to lift institutional prescription rates.

Regional demand dynamics for the Lens Cleaning Cloths Market vary substantially across the five primary geographies tracked in this analysis, reflecting differences in optical device penetration, retail infrastructure, institutional procurement maturity, and regulatory standards.

North America remains the largest regional market by absolute revenue, accounting for an estimated 32–35% of global market value in 2025. The United States is the dominant sub-market, driven by high eyewear penetration rates, a mature optical retail infrastructure, and significant institutional demand from the healthcare, laboratory, and education sectors. The regional CAGR is projected at 7.2% through 2033, slightly below the global average, reflecting market maturity rather than demand saturation.

Europe holds the second-largest revenue share, approximately 28–30% of the global market. Germany, the United Kingdom, and France collectively account for the majority of European demand. Stringent optical quality and product safety standards — including CE marking requirements and evolving REACH chemical regulations — favor premium, certified products and support above-average unit pricing. The European market CAGR is estimated at 7.8%, with sustainability-oriented product lines growing disproportionately faster.

Asia Pacific is the fastest-growing regional market, with a projected CAGR of 10.4% through 2033. China and India are the primary growth engines, reflecting rapidly expanding middle-class populations acquiring prescription eyewear and consumer electronics at accelerating rates. Japan and South Korea maintain premium market characteristics aligned with the global average, while ASEAN markets represent high-growth frontier opportunities currently in the early stages of optical retail formalization.

South America contributes approximately 5–7% of global market value, with Brazil as the dominant sub-market. Growth is constrained by macroeconomic volatility in Argentina and limited optical retail infrastructure outside major urban centers. The regional CAGR is estimated at 6.5%, with e-commerce channels emerging as the primary access point for quality products.

The Middle East and Africa region represents the smallest share at approximately 4–5%, though GCC countries — particularly the UAE and Saudi Arabia — exhibit above-average per-capita spend on premium optical accessories. South Africa serves as the regional hub for sub-Saharan African distribution. The regional CAGR is projected at 7.0%, with growth anchored in urbanizing consumer classes and expanding optical retail networks.

The Lens Cleaning Cloths Market operates within a multi-layered regulatory environment that differs meaningfully between wet and dry product formats and across key geographies.

In the European Union, wet lens cleaning wipes containing preservatives, biocides, or alcohol-based formulations fall under the EU Biocidal Products Regulation (BPR, Regulation 528/2012) and the EU Cosmetics Regulation (EC 1223/2009), depending on the product's marketed function. Manufacturers must demonstrate active ingredient safety and efficacy through structured dossier submissions to national competent authorities. The forthcoming revision of REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) is expected to impose additional restrictions on certain preservative chemistries used in wet wipes, potentially accelerating reformulation timelines for multiple market participants by 2027.

Dry microfiber cloths face fewer direct chemical regulations but are increasingly subject to textile sustainability mandates. The EU's Strategy for Sustainable and Circular Textiles (2022) is driving

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Lens Cleaning Cloths Market market expansion.

Key companies in the market include Velda, E-cloth, Toray, Zeiss wipes, Euro, Game, CMA, Atlas Graham, Medline, Aqua Star, Dish Cloths, Scotch-Brita, Waldron, Nordex, Unger, ERC.

The market segments include Type, Application, Industry Vertical, Distribution Channel.

The market size is estimated to be USD 1.2 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Lens Cleaning Cloths Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Lens Cleaning Cloths Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.