1. What are the major growth drivers for the Camping Coolers Market market?

Factors such as are projected to boost the Camping Coolers Market market expansion.

+1 2315155523

Camping Coolers Market

Camping Coolers Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

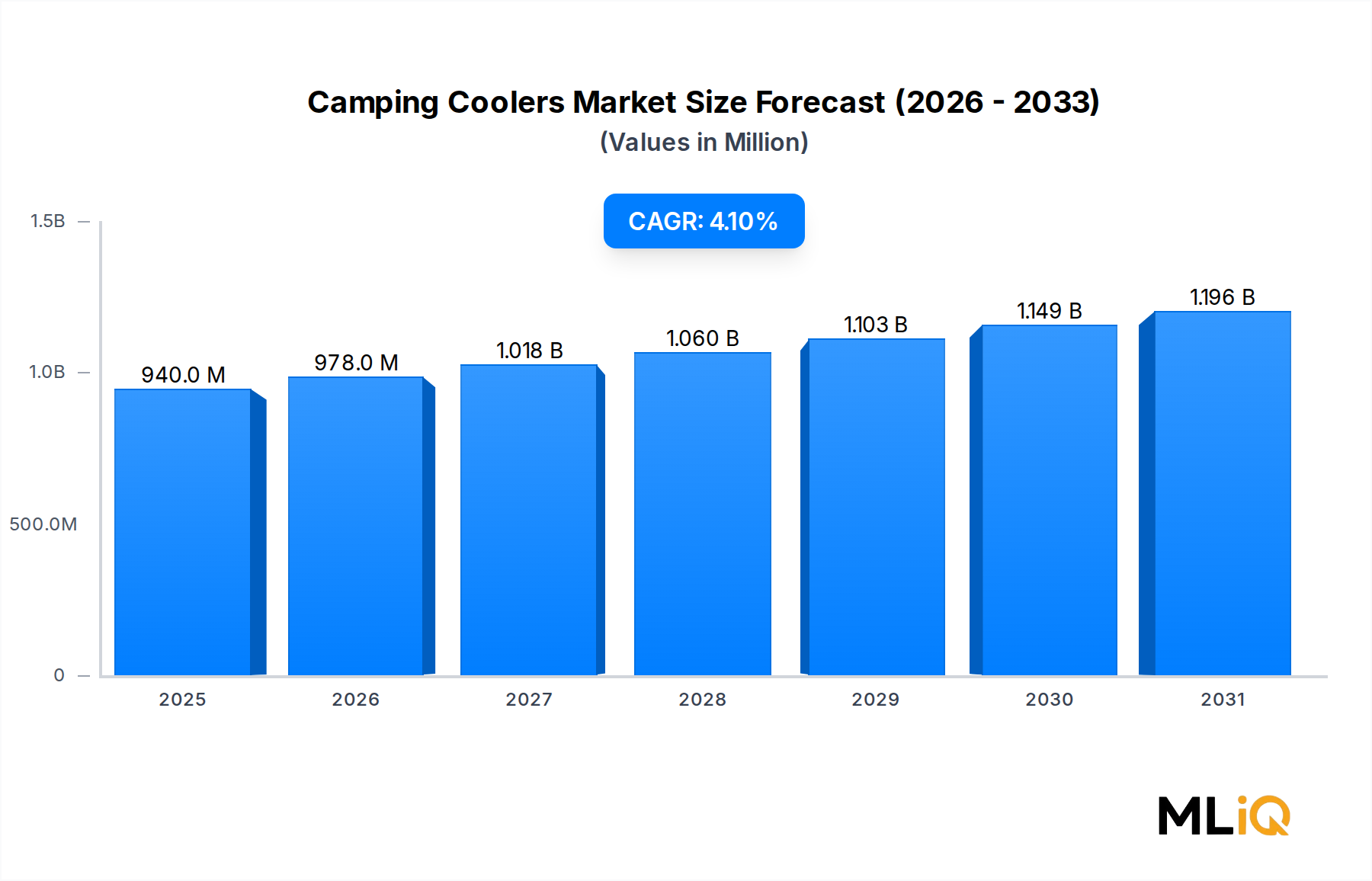

The global camping coolers market is valued at $939.51 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 4.1% through 2033, driven by a convergence of rising outdoor recreation participation, product premiumization trends, and escalating consumer demand for extended ice retention and portability. The market's trajectory reflects a broadening consumer base that spans weekend campers, professional overlanders, tournament anglers, and tailgating enthusiasts, each placing distinct performance and durability requirements on their cooler purchases.

Macroeconomic tailwinds remain supportive. Post-pandemic behavioral shifts have institutionalized outdoor leisure as a mainstream lifestyle segment rather than a niche hobby. National park visitor statistics, RV shipment volumes, and camping gear expenditure data all corroborate sustained engagement with outdoor activities well into the mid-2020s. This structural demand underpins consistent revenue growth across all cooler typologies, from entry-level soft-sided units to premium rotomolded hard-shell variants commanding retail price points exceeding $400.

Product innovation is a primary competitive differentiator. Manufacturers are integrating advanced insulation chemistries, antimicrobial liner technologies, and ergonomic hardware to justify premium pricing and expand addressable consumer segments. The convergence of the Portable Coolers Market and smart device connectivity—through embedded temperature sensors and Bluetooth monitoring—represents an emerging frontier that is beginning to attract venture-backed startups and corporate R&D investment alike.

On the supply side, raw material dynamics tied to the Polyurethane Foam Insulation Market and the High-Density Polyethylene Market continue to influence manufacturing cost structures. Petrochemical price volatility, observed acutely during 2022 and 2023, compressed margins for mid-tier manufacturers, incentivizing vertical integration strategies and nearshoring of production assets, particularly within North America.

Geographically, North America retains the largest revenue share, anchored by deep camping culture, high per-capita disposable income, and mature retail distribution infrastructure. However, Asia Pacific is registering the fastest growth momentum, propelled by expanding middle-class outdoor recreation participation in China, India, and across ASEAN markets.

Looking forward to 2033, the market is expected to benefit from continued growth in e-commerce penetration, sustainable materials adoption, and the premiumization of the Outdoor Leisure Products Market. Brands capable of delivering verifiable performance credentials—validated by third-party ice retention certifications—alongside compelling sustainability narratives will be best positioned to capture incremental share in an increasingly crowded competitive landscape.

The hard cooler segment represents the single largest revenue-generating category within the camping coolers market, accounting for a commanding share of total market value in 2025. This dominance is attributable to multiple reinforcing factors: superior thermal performance, structural durability, brand prestige associations, and the segment's strong alignment with high-expenditure consumer profiles such as serious anglers, hunters, overlanding enthusiasts, and expedition campers.

Hard coolers are defined by their rigid outer shell, typically constructed from rotationally molded polyethylene or injection-molded plastic, filled with thick-wall polyurethane foam insulation. Leading premium variants within this segment deliver ice retention performance ranging from 5 to 10 days under controlled conditions, a specification that has become a de facto industry benchmark and a key purchase decision criterion for performance-oriented buyers. This capability gap versus soft-sided alternatives sustains the hard cooler's pricing premium and its disproportionate contribution to total market revenue despite unit volume competition from lower-priced soft coolers.

The Rotomolded Coolers Market, a premium sub-segment within hard coolers, has been one of the fastest-growing product categories over the past five years. Rotomolded construction—where molten resin is cast in a rotating mold to produce a single-piece, seamless shell—virtually eliminates structural weak points and delivers superior insulation continuity. Brands including Yeti Coolers, ORCA, Grizzly Coolers, Pelican Coolers, and K2 Coolers have built their entire brand equity around rotomolded hard cooler technology, successfully positioning these products as aspirational purchases within the broader Outdoor Recreation Equipment Market.

Yeti Coolers pioneered the premiumization of this segment when it introduced its Tundra line to North American consumers, effectively creating a new product category that redefined consumer expectations for cooler performance and price tolerance. Competitors subsequently invested heavily in rotomolded manufacturing capabilities and comparable engineering specifications, intensifying competition across the $200–$500 price tier. Igloo Coolers and Coleman Coolers, historically dominant in the value-oriented hard cooler segment, have responded by launching premium sub-brands and extending their product lines into the rotomolded category to defend market share against the influx of performance-focused challengers.

The 25–100 quart capacity range within hard coolers constitutes the highest-volume sub-segment by units sold, offering a practical balance between carrying capacity and physical manageability for typical camping party sizes of two to six individuals. This capacity tier accommodates multi-day food and beverage storage requirements without exceeding the portability threshold at which two-person carry handles and wheeled chassis configurations become necessary.

Material innovation within the hard cooler segment continues to evolve. Manufacturers are experimenting with co-molded composite shells incorporating glass fiber reinforcement, titanium-infused liner coatings for antimicrobial performance, and recycled post-consumer resins to meet growing sustainability mandates from retail partners and environmentally conscious consumers. These material innovations intersect with dynamics in both the High-Density Polyethylene Market and the Polyurethane Foam Insulation Market, where bio-based feedstock research is beginning to yield commercially viable substitutes for petroleum-derived inputs.

The hard cooler segment's share is consolidating rather than growing at the expense of soft coolers, as the overall market benefits from category expansion. However, within hard coolers, the premium rotomolded tier is gaining share relative to standard injection-molded units, reflecting the broader consumer trade-up behavior visible across outdoor gear categories.

Several quantifiable forces are shaping the demand and supply trajectory of the camping coolers market through 2033.

Driver 1: Outdoor Recreation Participation Growth. U.S. outdoor recreation participation reached record levels following 2020, with the Outdoor Industry Association reporting over 160 million Americans engaging in outdoor activities annually by 2022. Camping specifically registered a 72 million participant base in the United States alone, directly correlating with cooler purchase intent across all product tiers. Internationally, camping participation metrics in Germany, Australia, Japan, and South Korea have shown year-over-year increases of 3–7%, broadening the global addressable market.

Driver 2: Premiumization and Willingness to Pay. Consumer willingness to invest in high-performance outdoor gear has been validated by Yeti's consistent revenue growth, which surpassed $1.6 billion in annual net sales by 2022, with coolers and equipment representing a meaningful share. This validates the existence of a large, price-inelastic consumer segment prioritizing performance over cost, supporting sustained average selling price (ASP) expansion across the market.

Driver 3: E-commerce Channel Expansion. Direct-to-consumer and marketplace e-commerce channels have materially lowered barriers to market entry for challenger brands and have expanded geographic reach for established players. Online penetration within the broader Outdoor Leisure Products Market now exceeds 30% in North America, enabling brands like AO Coolers and Polar Bear Coolers to compete nationally without proportional brick-and-mortar infrastructure investment.

Constraint 1: Raw Material Cost Volatility. The Polyurethane Foam Insulation Market experienced significant price inflation during 2021–2022 due to MDI and polyol supply disruptions, raising input costs for insulated container manufacturers by an estimated 15–25%. Manufacturers without long-term supply agreements faced margin compression that limited R&D reinvestment capacity.

Constraint 2: Market Saturation in Premium Tiers. The rotomolded cooler segment now features over 20 credible brands competing on near-identical performance specifications, creating commoditization pressure that threatens to erode brand premium over time and intensify promotional discounting.

The competitive landscape of the camping coolers market is fragmented at the value tier and oligopolistic at the premium tier, with a small cluster of performance brands commanding disproportionate consumer mindshare and retail shelf space.

Yeti Coolers: The defining premium brand in the rotomolded cooler category, Yeti has successfully expanded from a product company into a lifestyle brand, deploying ambassador marketing, limited-edition colorways, and cross-category product extensions to maintain aspirational positioning and defend its commanding market share premium.

Coleman Coolers: As one of the most recognized names in outdoor equipment globally, Coleman dominates the value and mid-range hard cooler segment, leveraging expansive mass-market retail distribution through Walmart, Target, and Amazon to maintain category leadership by unit volume despite modest ASP positions.

Igloo Coolers: A heritage brand with decades of manufacturing experience, Igloo has pursued a dual-track strategy of defending its core value-oriented consumer base while launching premium lines including the IMX and Trailmate series to compete in the performance segment occupied by Yeti and ORCA.

ORCA: Headquartered in Tennessee and manufacturing domestically, ORCA differentiates through its made-in-USA value proposition and lifetime warranty, appealing to patriotic consumer sentiment and professional users in hunting and fishing verticals who demand maximum durability and brand accountability.

Pelican Coolers: Leveraging Pelican's institutional credibility in professional protective case solutions for military and law enforcement, Pelican Elite Coolers carry a trusted performance halo into the consumer camping segment, commanding premium price points with strong brand credibility among technically oriented buyers.

Grizzly Coolers: A rotomolded cooler specialist targeting serious hunters, anglers, and outdoor professionals, Grizzly competes primarily on ice retention performance and structural toughness, backed by a bear-resistant certification that resonates strongly with backcountry and wilderness camping consumers.

Engel Coolers: Known for both passive hard coolers and thermoelectric refrigeration units, Engel serves a dual segment spanning traditional camping coolers and 12V powered refrigeration for overlanding and marine applications, providing broader product line coverage than most single-category competitors.

AO Coolers: Specializing in high-performance soft-sided coolers, AO Coolers has carved a distinctive niche in the Soft-Sided Coolers Market, delivering near-hard-cooler ice retention in flexible, packable form factors that appeal to backpackers, kayakers, and weight-conscious travelers.

K2 Coolers: A Texas-based premium rotomolded cooler brand, K2 competes in the direct challenger tier against Yeti through aggressive pricing-to-performance positioning and regional brand affinity, particularly strong in the Southern United States hunting and fishing demographic.

Polar Bear Coolers: Focused exclusively on soft-sided thermal carriers, Polar Bear Coolers targets the lunch bag, day-trip, and soft cooler segments with TPU-lined products offering superior flexibility and cleanability versus traditional fabric-and-foam competitors.

March 2023: Yeti Coolers announced the expansion of its direct-to-consumer e-commerce infrastructure with enhanced customization capabilities, allowing consumers to personalize hard coolers with monogramming and custom colorways, driving ASP increases of approximately 8–12% on personalized SKUs.

June 2023: Igloo Coolers launched its first fully recycled-content cooler line, incorporating 100% post-consumer recycled plastic in the outer shell, responding directly to retailer ESG mandates and consumer sustainability expectations intensifying across the outdoor gear category.

September 2022: Pelican Products completed a strategic expansion of its cooler production capacity at its U.S. manufacturing facility, increasing annual output capability to address growing demand in both consumer and professional end-use segments.

January 2023: Coleman Coolers introduced a new wheeled hard cooler series featuring an upgraded sealing gasket system and ergonomic telescoping handle, targeting the family camping segment with a retail price point positioned between its value core line and the premium rotomolded tier.

April 2022: ORCA expanded its retail distribution agreements with Bass Pro Shops and Cabela's, significantly increasing its brick-and-mortar shelf presence across more than 200 additional retail locations in North America.

November 2022: Engel Coolers released an updated 12V thermoelectric refrigeration unit with Bluetooth temperature monitoring capability, positioning the product at the intersection of the Thermoelectric Cooling Devices Market and the connected outdoor gear trend.

February 2024: Grizzly Coolers introduced a new limited-edition collaboration with a major waterfowl hunting organization, reinforcing its vertical market penetration strategy in the hunting segment and generating measurable social media engagement metrics.

North America commands the largest regional revenue share of the global camping coolers market, estimated at approximately 42–45% of total market value in 2025. The United States alone represents the deepest single-country market, supported by a mature camping culture, high rates of RV ownership (approximately 11.2 million RVs registered domestically), and an established premium retail ecosystem spanning specialty outdoor retailers, mass merchandisers, and direct e-commerce channels. Canada and Mexico contribute incremental volume, with Canada showing particular strength in hard cooler categories aligned with hunting and fishing activity concentrations. The North American market is the most mature region, characterized by relatively modest incremental growth in the 3.5–4.0% CAGR range, with growth increasingly driven by premiumization and product replacement cycles rather than first-time category purchases.

Europe represents the second-largest regional market, with Germany, the United Kingdom, France, and the Nordics comprising the dominant revenue contributors. European consumers demonstrate strong preference for premium, sustainably manufactured products, aligning well with the category's premiumization trajectory. Regional CAGR is estimated at 3.0–3.5%, moderated by a more developed camping infrastructure and cultural preference for cabin and structured campsite accommodation over improvised backcountry camping styles that require extended cold storage solutions.

Asia Pacific is the fastest-growing regional market, projected at a CAGR of 5.5–6.5% through 2033. China, India, Japan, South Korea, and ASEAN markets are all registering accelerating outdoor recreation participation driven by rising disposable incomes, urban-to-outdoor lifestyle aspirations among millennials and Gen Z cohorts, and aggressive marketing investment from both global and domestic outdoor gear brands. The Insulated Containers Market in Asia Pacific is benefiting from infrastructure investment in camping and glamping resort development, creating demand for both consumer-owned and facility-provided cooler solutions.

South America, led by Brazil and Argentina, presents a developing but high-potential market growing at approximately 4.5–5.0% CAGR, driven by expanding fishing tourism, beach camping culture, and growing middle-class outdoor recreation participation. The Middle East and Africa region, while currently representing a smaller revenue share, is showing above-average growth momentum in GCC countries where outdoor adventure tourism investment and premium consumer goods consumption are both accelerating.

The consumer base of the camping coolers market stratifies into several discrete segments with meaningfully different purchasing criteria, price sensitivities, and procurement channel preferences.

The performance enthusiast segment—comprising serious anglers, hunters, overlanders, and expedition campers—represents the highest-value customer cohort. These buyers prioritize technical specifications, specifically ice retention duration, structural durability, and bearing capacity certifications such as bear-resistant ratings from the Interagency Grizzly Bear Committee. Price sensitivity in this segment is low; buyers routinely invest $300–$500 or more in premium rotomolded units and demonstrate strong brand loyalty with repeat purchase rates that sustain

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Camping Coolers Market market expansion.

Key companies in the market include Engel Coolers, AO Coolers, ORCA, Igloo Coolers, Yeti Coolers, Grizzly Coolers, Coleman Coolers, K2 Coolers, Pelican Coolers, Polar Bear Coolers.

The market segments include Type, Material, Capacity.

The market size is estimated to be USD 939.51 million as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in million and volume, measured in .

Yes, the market keyword associated with the report is "Camping Coolers Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Camping Coolers Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.