1. What are the major growth drivers for the Cardless ATM Market market?

Factors such as are projected to boost the Cardless ATM Market market expansion.

+1 2315155523

Cardless ATM Market

Cardless ATM Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

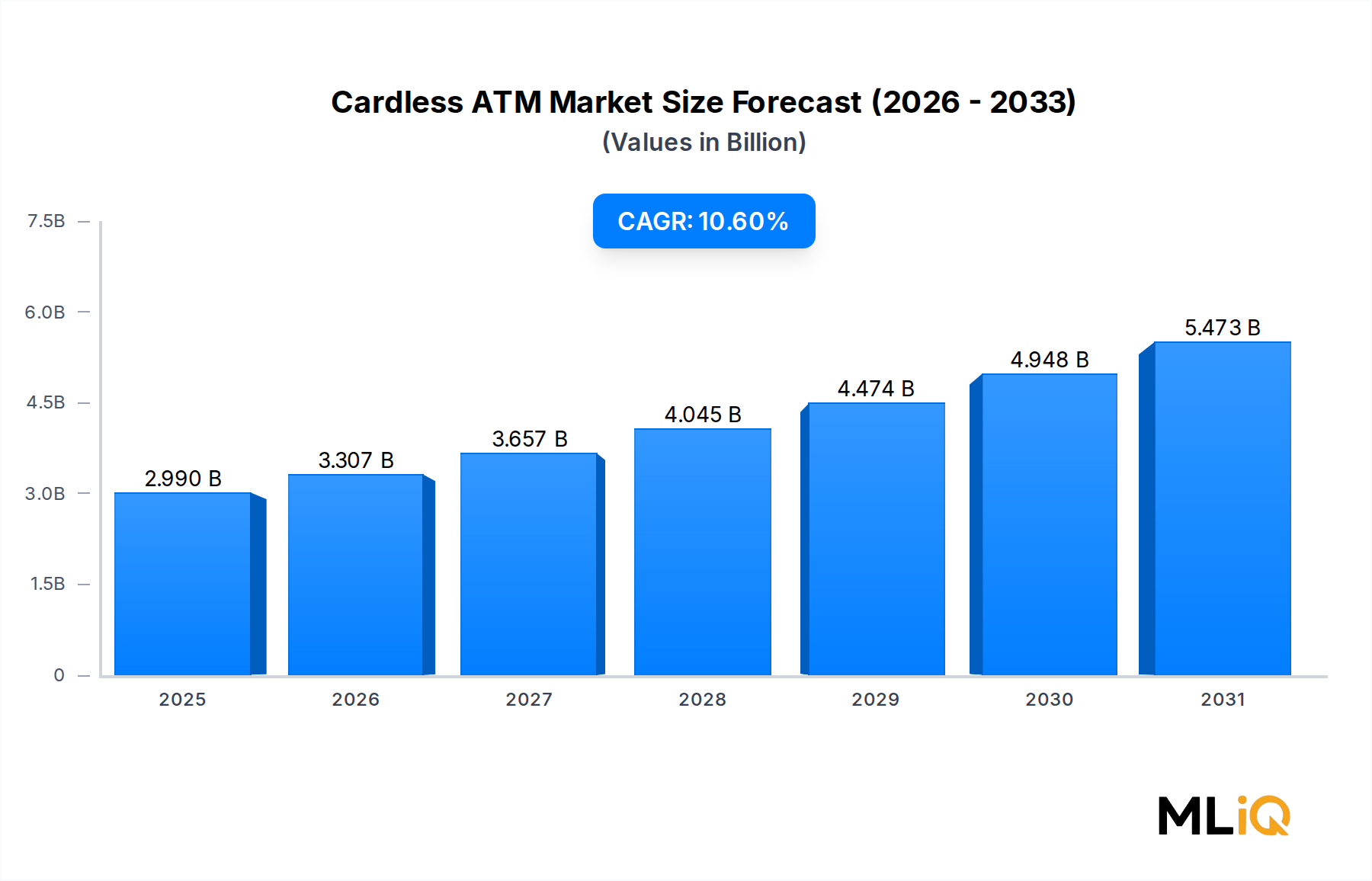

The global Cardless ATM Market is valued at $2.99 billion as of the base assessment period and is projected to expand at a compound annual growth rate (CAGR) of 10.6% through 2033, reflecting a robust structural shift in how consumers access cash and banking services without the need for a physical debit or credit card. This market sits at the intersection of rising smartphone penetration, accelerating digital banking adoption, and intensifying consumer demand for secure, frictionless financial transactions.

The primary demand drivers include the global proliferation of mobile wallets, near-field communication (NFC) infrastructure investments by major financial institutions, and the expanding deployment of QR code-based authentication frameworks across emerging economies. Macro tailwinds such as post-pandemic hygiene consciousness, growing fraud prevention mandates from central banks, and increasing government-led financial inclusion programs are also reinforcing market momentum.

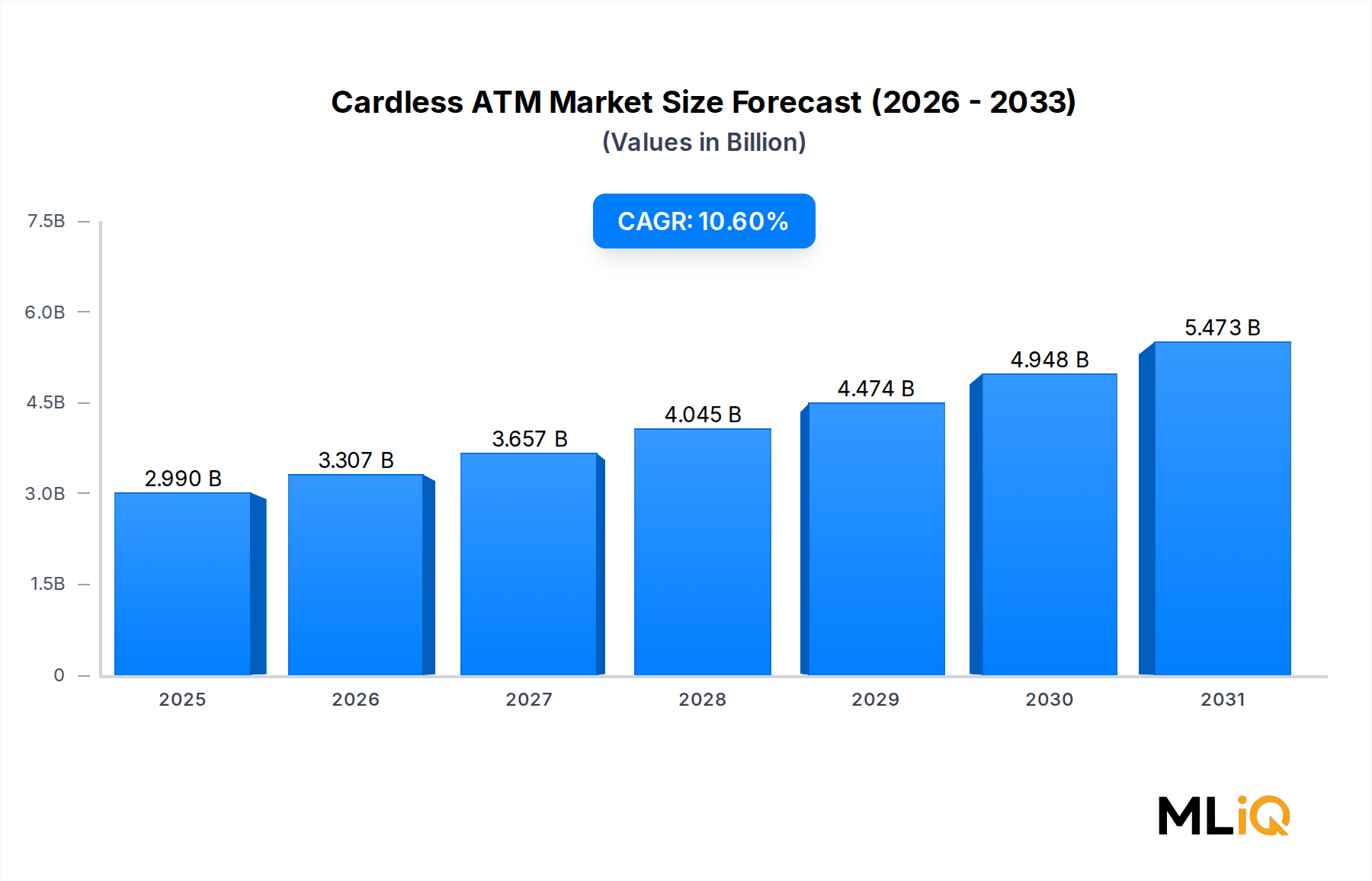

North America currently leads in absolute revenue terms, driven by early technology adoption among Tier-1 banks and the presence of major ATM deployers who have already integrated interoperable cardless access into their networks. Asia Pacific, however, is emerging as the fastest-growing regional segment, propelled by smartphone-first banking populations in China, India, and Southeast Asia. These geographies benefit from a leapfrog dynamic where consumers bypass traditional card-based banking altogether.

From a technology perspective, NFC and QR code solutions are the two dominant modalities enabling cardless transactions. NFC-based deployments are favored in markets with mature contactless infrastructure, while QR code solutions offer lower hardware costs and are therefore more prevalent in cost-sensitive emerging markets. Biometric layering is increasingly being added to both modalities, enhancing security without sacrificing transaction speed.

Looking forward, the Cardless ATM Market is expected to benefit significantly from ongoing integration with mobile banking super-apps, open banking application programming interfaces (APIs), and interoperability standards being developed by regional central banks. The convergence of these forces creates a favorable environment for both incumbent financial institutions and independent ATM deployers to capitalize on the growing preference for card-free cash access. By 2033, the market is anticipated to reach a materially higher absolute valuation, with emerging market deployments accounting for an increasing proportion of total global installations and transaction volumes.

Among the deployment types analyzed in the Cardless ATM Market, on-site ATMs — those located within or directly adjacent to bank branches and affiliated financial institution premises — represent the dominant segment by revenue share. This dominance is underpinned by several structural and operational factors that distinguish on-site deployments from off-site and other categories.

First, on-site ATMs benefit from the existing IT and network infrastructure of the parent financial institution. Banks such as JPMorgan Chase & Co., Wells Fargo, and Citigroup Inc. have invested heavily in branch-integrated ATM ecosystems that are tightly coupled to their mobile banking platforms. This integration enables seamless cardless transaction authorization workflows, where a customer initiates a withdrawal via a mobile app and completes the transaction at the ATM using NFC, QR code, or biometric verification — all within a secured, bank-controlled environment.

Second, the regulatory and compliance benefits of on-site deployments are significant. Financial institutions operating on-site ATMs can enforce more granular know-your-customer (KYC) and anti-money laundering (AML) protocols, which are increasingly mandated by central banks and financial regulators globally. This makes on-site ATMs more attractive to large-scale financial institutions seeking to remain compliant while expanding cardless capabilities.

Third, consumer trust levels are measurably higher at on-site ATMs. Survey data consistently shows that customers prefer conducting novel or high-value transactions — such as those using a cardless modality for the first time — in locations they associate with institutional oversight and recourse. This behavioral factor reinforces the revenue dominance of on-site ATMs, particularly in the early adoption phases of cardless technology.

Key players driving growth in the on-site segment include NCR Corporation, which supplies ATM hardware and software to a large portion of global bank branches, and Fujitsu, whose intelligent ATM platforms are deployed across European and Asian banking networks. Barclays Bank PLC and HSBC Bank A.S. have also been active in rolling out NFC-enabled cardless withdrawals exclusively through their on-site branch ATMs before extending capabilities to off-site networks.

The on-site segment's share is currently consolidating, meaning that while it remains the largest segment, its relative share is being incrementally pressured by accelerating off-site deployments in high-traffic retail, transit, and hospitality locations. Independent ATM deployers are increasingly adopting cardless protocols for off-site machines, particularly in Asia Pacific and Latin America, where urban mobility patterns concentrate cash demand in non-branch locations.

Nevertheless, on-site ATMs are expected to retain their revenue leadership through the forecast period ending 2033, particularly as banks expand branch-level ATM functionality to include cardless bill payment, account-to-account transfers, and digital receipt issuance — services that are more difficult to implement in off-site environments without dedicated back-end integration.

The competitive dynamic within the on-site segment is increasingly shaped by software differentiation rather than hardware alone. Vendors offering end-to-end cardless transaction management platforms — encompassing mobile app SDK integration, token issuance, real-time fraud scoring, and session management — are gaining a disproportionate share of new deployment contracts compared to pure hardware suppliers.

The Cardless ATM Market is subject to a well-defined set of growth drivers and structural constraints, each of which can be quantified and contextualized against current market data.

Smartphone penetration is the most consequential demand driver. Global smartphone penetration exceeded 6.8 billion active devices as of 2024, providing the hardware base necessary for cardless ATM authentication. In markets such as India and Indonesia, mobile-first banking populations are growing at double-digit annual rates, directly expanding the addressable user base for cardless ATM services without requiring new physical card issuance infrastructure.

Cybersecurity and card skimming prevention mandates represent a secondary but accelerating driver. ATM fraud globally cost the banking industry an estimated $2 billion annually in recent years, and regulatory pressure to reduce card-present transaction vulnerabilities has incentivized financial institutions to accelerate cardless roadmaps as a fraud mitigation strategy. The elimination of the physical card as an attack vector substantially reduces exposure to skimming, shimming, and card-trapping attack vectors.

The rapid evolution of the Mobile Banking Market and its deep integration with ATM networks is also amplifying demand. As mobile banking applications incorporate real-time cardless withdrawal initiation features, the friction cost for the end user drops materially, driving adoption velocity.

On the constraint side, interoperability limitations represent a significant inhibitor. Most cardless ATM ecosystems are currently closed-loop — a customer of Bank A typically cannot use Bank A's mobile app to initiate a cardless withdrawal at Bank B's ATM. This fragmentation limits the network utility of cardless systems and suppresses adoption among consumers who regularly use multi-bank ATM networks. Standardization efforts are underway but adoption timelines remain uncertain.

Infrastructure costs pose a further constraint, particularly for independent ATM deployers. Retrofitting existing ATMs with NFC readers, camera arrays for QR code scanning, and secure element hardware requires per-unit capital expenditure that may not be immediately recoverable through transaction fee revenues in low-volume locations.

The competitive landscape of the Cardless ATM Market is characterized by a blend of established ATM hardware manufacturers, large global banks deploying proprietary cardless solutions, and emerging fintech-adjacent software providers. The following profiles outline the strategic positioning of key participants:

Fujitsu: A leading ATM hardware manufacturer with a strong presence in Asia Pacific and Europe, Fujitsu has developed intelligent ATM platforms that support NFC and QR code-based cardless authentication, positioning the company as a preferred hardware partner for banks undergoing cardless transition programs.

Wells Fargo: One of the earliest large-scale adopters of cardless ATM technology in North America, Wells Fargo enabled NFC-based withdrawals across its network using mobile wallet integration, establishing a blueprint that other regional banks have since followed.

Barclays Bank PLC: Barclays has integrated cardless cash withdrawal capabilities into its mobile banking application across its UK branch ATM network, leveraging its digital banking infrastructure to reduce reliance on physical card issuance and associated fraud vectors.

GRG Banking: A major ATM manufacturer based in China, GRG Banking supplies cardless-capable ATM hardware to a significant share of the Asia Pacific market, with deployments spanning commercial banks and independent deployers across Southeast Asia.

NCR Corporation: As one of the world's largest ATM technology companies, NCR Corporation provides both hardware and software platforms that enable cardless transaction processing, offering bank clients end-to-end deployment capabilities from ATM management software to consumer-facing mobile SDK toolkits.

Citigroup Inc.: Citigroup has deployed cardless ATM capabilities across multiple geographies, leveraging its global banking network to offer consistent cardless withdrawal experiences to its international customer base through NFC-enabled handset authentication.

ICICI Bank Ltd.: Among the most technologically advanced banks in India, ICICI Bank Ltd. has pioneered cardless ATM withdrawals using both OTP-based and mobile app-authenticated methods, making it a benchmark institution in emerging market cardless deployment.

Santander Group: Santander has rolled out cardless ATM functionality across its Latin American and European retail banking networks, integrating cardless features with its broader digital transformation strategy focused on reducing branch operational costs.

JPMorgan Chase & Co.: With one of the largest ATM networks in the United States, JPMorgan Chase & Co. has deployed NFC-enabled cardless withdrawals through its Chase Mobile app, citing both security enhancement and customer experience improvement as primary rationale.

HSBC Bank A.S.: HSBC has introduced cardless cash withdrawal services in select markets, using mobile app-generated tokens that expire within a short authentication window to minimize transaction fraud exposure.

March 2024: NCR Corporation announced an expanded partnership with a consortium of North American credit unions to deploy cardless-capable ATM firmware updates across more than 12,000 machines, representing one of the largest single-phase cardless rollouts in the region.

June 2024: ICICI Bank Ltd. reported that cardless ATM transactions on its network surpassed 50 million cumulative transactions since the feature's launch, marking a significant adoption milestone in the Indian retail banking segment.

September 2024: GRG Banking unveiled a next-generation ATM series with integrated dual-mode cardless support — combining NFC and QR code readers in a single unit — targeting deployment in mixed-infrastructure markets across Southeast Asia.

November 2024: Barclays Bank PLC expanded its cardless withdrawal limit from £250 to £500 per transaction following positive fraud performance data collected over an 18-month monitoring period, reflecting growing institutional confidence in cardless security protocols.

January 2025: JPMorgan Chase & Co. announced integration of its Chase Mobile cardless ATM feature with third-party digital wallet platforms, extending cardless access beyond proprietary app users to a broader authenticated customer base.

March 2025: Santander Group completed a pilot program in Brazil enabling cardless ATM withdrawals via biometric facial recognition on a cohort of 500 ATMs, with plans to scale to 5,000 units by year-end 2025.

April 2025: The Reserve Bank of India issued updated guidelines encouraging all scheduled commercial banks to deploy interoperable cardless ATM capabilities by Q4 2026, significantly accelerating the policy tailwind for the market in one of its highest-growth geographies.

The Cardless ATM Market exhibits pronounced regional heterogeneity in terms of adoption maturity, infrastructure readiness, and regulatory tailwinds.

North America is the most mature regional market, accounting for the largest revenue share globally. The United States leads within this region, driven by early institutional investment from top-tier banks and high smartphone penetration among banked populations. The region benefits from well-established NFC infrastructure, with contactless payment terminals already deployed at scale across retail and banking environments. Growth in North America is steady but moderating relative to earlier adoption phases, with the CAGR in this region estimated in the mid-to-high single digits through 2033.

Asia Pacific is the fastest-growing regional segment, with a regional CAGR estimated above the global average of 10.6%, potentially reaching the low-to-mid teens in markets such as India, China, and Vietnam. The driver here is the convergence of large unbanked and underbanked populations gaining first-time access to formal financial services through smartphone-based banking, combined with government mandates in countries like India that are pushing interoperability standards for cardless ATM access. China's domestic banking infrastructure, led by major state-owned banks and ATM manufacturers such as GRG Banking, is also contributing significantly to volume growth.

Europe represents a moderately mature market with strong regulatory alignment. The European Banking Authority's frameworks on strong customer authentication (SCA) under PSD2 have inadvertently created a compliance environment that is well-suited for cardless ATM adoption, as the multi-factor authentication requirements of SCA align naturally with mobile-app-plus-ATM authentication workflows. The United Kingdom, Germany, and the Nordics are the leading sub-regions by deployment density.

Middle East & Africa is an emerging but rapidly evolving segment. The GCC countries — particularly the UAE and Saudi Arabia — are investing in smart banking infrastructure that includes cardless ATM capabilities as part of broader national digital transformation agendas. South Africa leads the Sub-Saharan portion of the region, with several commercial banks already offering OTP-based cardless withdrawals.

South America is gaining traction, particularly in Brazil and Argentina, where mobile banking penetration is high and demand for secure, card-free cash access is growing in tandem with financial inclusion initiatives.

Regulatory frameworks are playing an increasingly determinative role in the trajectory of the Cardless ATM Market, both as accelerators and, in some cases, as structural constraints requiring compliance investment.

In the European Union, the Payment Services Directive 2 (PSD2) and its strong customer authentication requirements have established a de facto standard for multi-factor authentication that aligns closely with cardless ATM transaction flows. Banks operating in the EU are required to authenticate high-value transactions using at least two independent factors, making mobile app-based token generation a compliant and preferred method for cardless ATM access.

In the United States, the Consumer Financial Protection Bureau (CFPB) and the Federal Financial Institutions Examination Council (FFIEC) have issued guidance on authentication standards for digital banking channels that is increasingly being applied to ATM interfaces. While no dedicated cardless ATM regulation exists at the federal level, the interplay of anti-fraud mandates and accessibility requirements is nudging banks toward broader deployment.

India's Reserve Bank has been among the most proactive regulators in this space. Its mandate for interoperable cardless ATM functionality — requiring all scheduled commercial banks to enable Unified Payments Interface (UPI)-based cardless withdrawals — represents the most explicit government-driven deployment target globally, with a compliance deadline of Q4 2026.

In the GCC, central banks in the UAE and Saudi Arabia have incorporated cardless banking capabilities into their respective national fintech strategies, offering regulatory sandboxes and accelerated licensing pathways for institutions deploying innovative authentication-based ATM solutions.

Standardization bodies, including the EMV Co. consortium and ISO's TC68 financial services technical committee, are actively developing interoperability specifications that would allow cardless ATM transactions to function across institutions and networks, addressing one of the market's most significant structural constraints. Progress in these standards bodies is expected to unlock material market expansion by reducing the closed-loop limitation that currently constrains multi-bank cardless ATM utility.

The end-user landscape of the Cardless ATM Market is divided into two primary procurement segments: banks and financial institutions, and independent ATM deployers (IADs). These two segments differ substantially in their purchasing criteria, price sensitivity

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.6% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Cardless ATM Market market expansion.

Key companies in the market include Fujitsu, Wells Fargo, Barclays Bank PLC, GRG Banking, NCR Corporation, Citigroup Inc., ICICI Bank Ltd., Santander Group, JPMorgan Chase & Co., HSBC Bank A.S..

The market segments include Type, Technology, Quick Response, End User.

The market size is estimated to be USD 2.99 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3570, USD 5730, and USD 9600 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Cardless ATM Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Cardless ATM Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.