1. What are the major growth drivers for the Liquid Lipstick Market market?

Factors such as are projected to boost the Liquid Lipstick Market market expansion.

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

Liquid Lipstick Market

Liquid Lipstick Market+1 2315155523

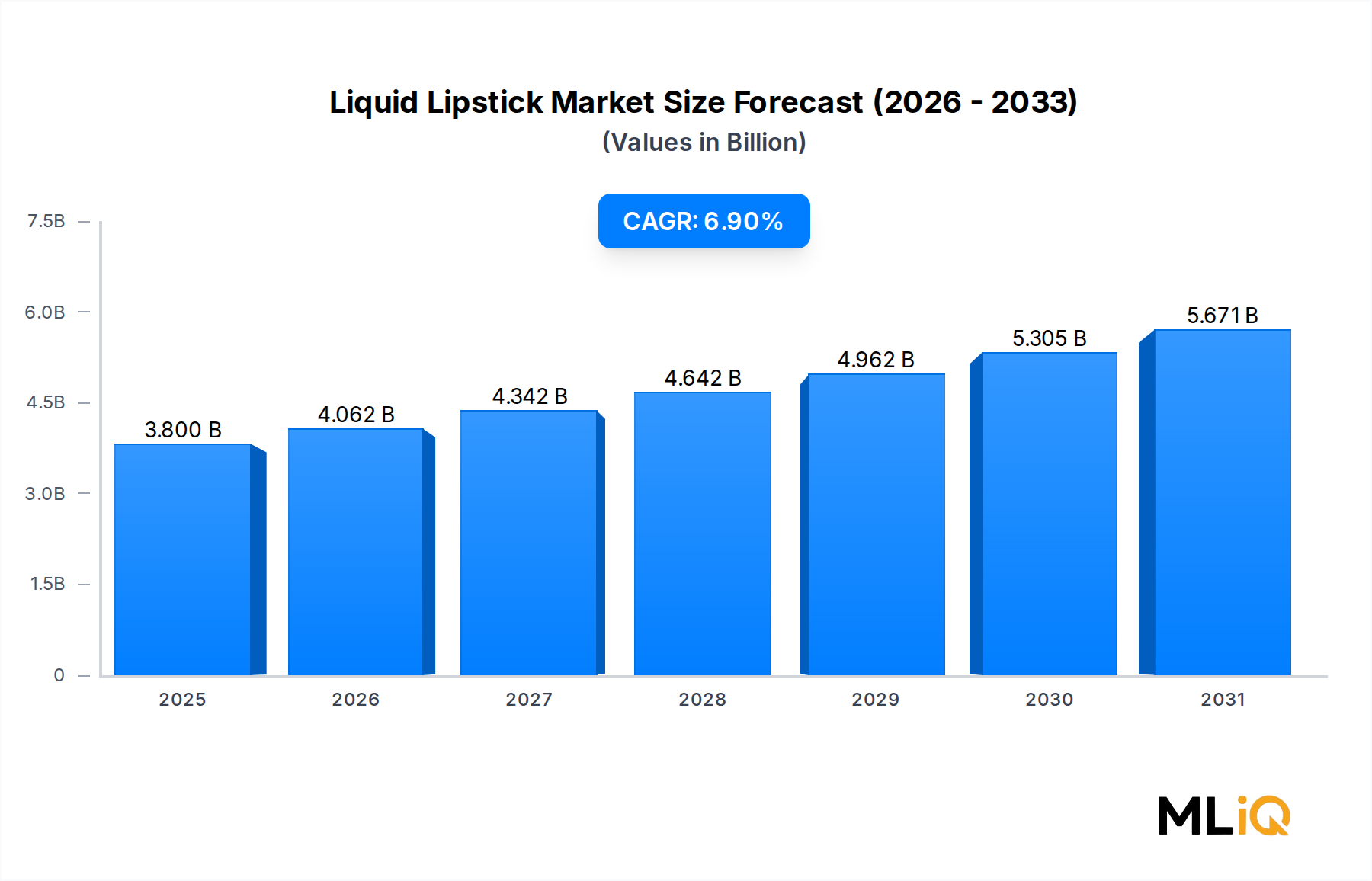

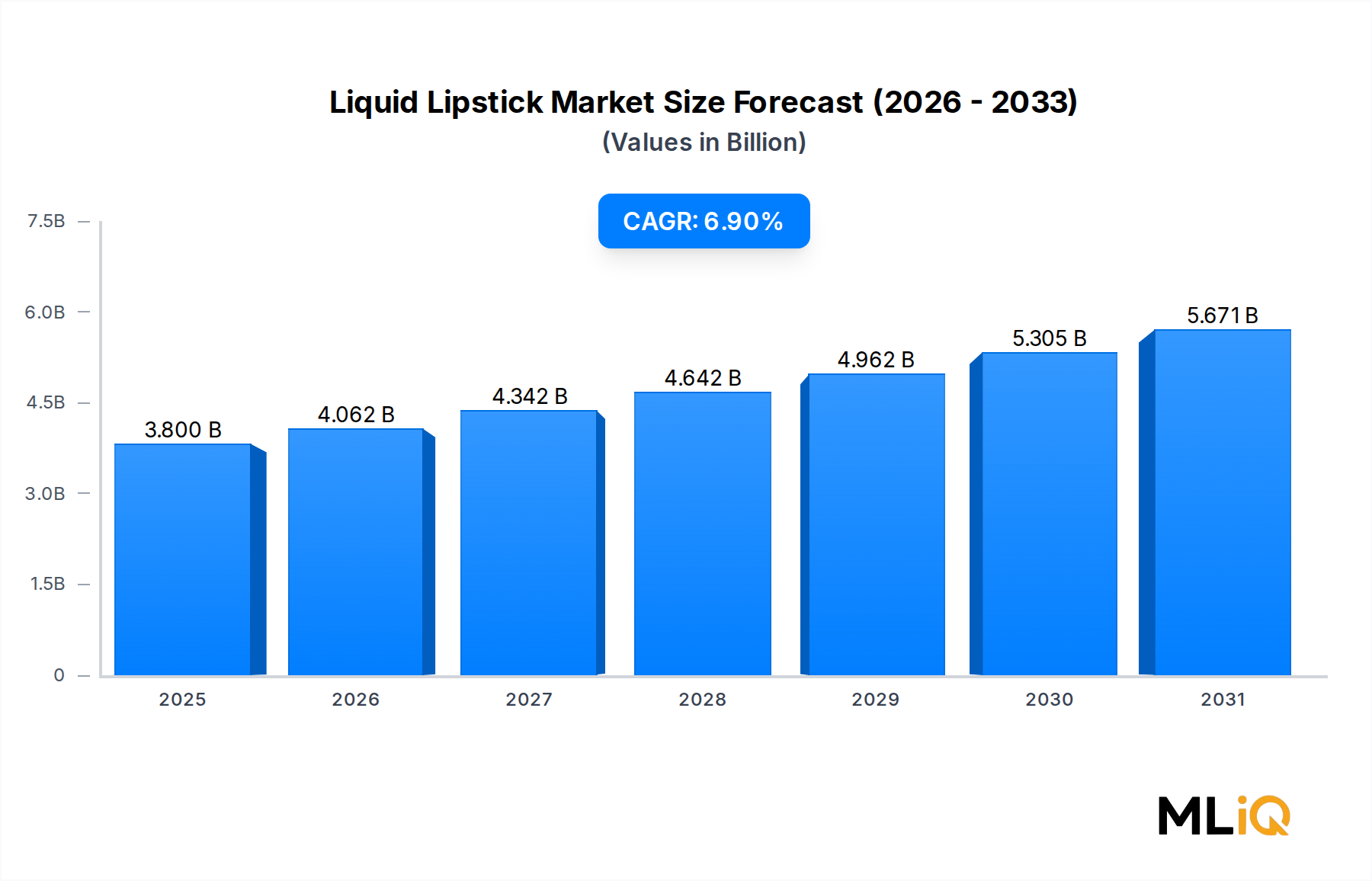

The global Liquid Lipstick Market is valued at $3.8 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 6.9% through 2033, reflecting robust consumer demand for long-wear, high-pigment lip color solutions across both established and emerging economies. This growth trajectory underscores a sustained shift in consumer preferences away from traditional bullet lipsticks toward fluid formulations that offer superior color payoff, extended wear, and versatile finish options including matte, glossy, and glitter variants.

Several macro tailwinds are actively propelling market expansion. First, the global rise in disposable income — particularly across Asia Pacific and Latin America — is enabling broader consumer access to premium cosmetic products. Second, social media and influencer culture continue to amplify awareness and adoption of new liquid lipstick launches, compressing the typical product discovery-to-purchase cycle. Platforms such as Instagram, TikTok, and YouTube have become central to product marketing, with beauty influencers commanding millions of followers and driving measurable spikes in product sales within 24 to 48 hours of a featured post.

Third, growing consumer interest in clean beauty and sustainably sourced formulations is compelling manufacturers to reformulate legacy products while launching new SKUs with natural or organic claims. This is creating a bifurcated product landscape where mass-market and premium segments coexist and grow simultaneously, driven by distinct but overlapping consumer bases.

From a demand perspective, the individual end-user segment continues to dominate revenue contribution, fueled by the democratization of beauty through affordable e-commerce channels. The commercial segment — comprising beauty parlors, salons, and makeup artist services — is registering measurable upticks as the professional beauty services industry rebounds and expands post-pandemic.

Looking ahead to 2033, the market is expected to be shaped by innovations in long-wear polymer technology, transfer-proof formulations, and hybrid skincare-cosmetic products that blend lip treatment benefits with color. Brands investing in personalization technologies — including custom shade-matching via AI and augmented reality — are likely to capture disproportionate market share. Sustainability commitments, including refillable packaging and biodegradable applicators, will increasingly serve as competitive differentiators rather than optional add-ons. Overall, the Liquid Lipstick Market presents a compelling investment thesis grounded in demographic expansion, premiumization, and product innovation dynamics.

Among all finish types within the Liquid Lipstick Market — including glossy, matte, glitter, and others — the matte segment commands the largest revenue share and has consistently maintained this leadership position since approximately 2018. Matte liquid lipsticks are characterized by a flat, non-reflective finish with high pigment concentration, typically delivered through a doe-foot applicator that enables precise application. Their dominance is rooted in several intersecting factors spanning consumer preference, formulation advancement, and cultural influence.

From a consumer behavior standpoint, matte liquid lipsticks are perceived as more sophisticated, long-lasting, and transfer-resistant compared to glossy alternatives. This perception has strong empirical backing: matte formulations typically incorporate film-forming polymers such as trimethylsiloxysilicate and acrylates copolymers that create a semi-flexible, adherent film on the lips — delivering wear times frequently exceeding 8 hours without significant fading or feathering. For working professionals and individuals who require low-maintenance beauty solutions, this functional superiority translates directly into purchasing decisions.

Cultural and media dynamics have further entrenched matte dominance. The mid-2010s social media era catalyzed a global matte lip trend driven by celebrity adoption and viral beauty content. Although the broader beauty industry periodically cycles back toward glossy aesthetics, matte liquid lipsticks have retained a structurally elevated baseline demand level that insulates the sub-segment from significant cyclical erosion.

Key players actively competing in the matte liquid lipstick space include L'Oreal, whose Infallible Pro-Matte line commands shelf space across mass-market retail channels globally; Estee Lauder Companies, whose MAC Cosmetics division offers a premium matte liquid portfolio with a strong professional makeup artist following; and Revlon Inc., which has historically leveraged its accessible price points to capture value-seeking consumers. Christian Dior SE competes in the ultra-premium tier with formulations that incorporate skincare-adjacent ingredients alongside the matte finish, justifying significant price premiums. Coty Inc. targets mid-market segments through its portfolio of licensed and owned brands.

Geographically, matte liquid lipstick demand is strongest in North America and Western Europe, where consumer familiarity with the format is highest and retail infrastructure supports extensive product trial. However, the fastest adoption growth for matte variants is currently observed in Southeast Asia and India, where younger demographic cohorts are consuming beauty content at scale through mobile platforms and translating this engagement into purchasing behavior via e-commerce.

In terms of market share trajectory, the matte segment's dominance is consolidating rather than eroding. Glossy formats are experiencing a moderate renaissance driven by Y2K aesthetic trends popular among Generation Z consumers, but glossy growth is coming largely from entirely new or lapsed consumers rather than from matte segment defectors. As formulators increasingly develop hybrid finishes — such as satin-matte or moisturizing matte — the matte segment's definitional boundaries are expanding to absorb adjacent preference profiles, further reinforcing its structural primacy within the broader Liquid Lipstick Market.

The Liquid Lipstick Market is shaped by a precise set of quantifiable drivers and constraints that collectively determine its growth velocity and competitive intensity.

Driver 1: E-commerce Channel Expansion. Online beauty retail has grown from a supplemental channel to a primary revenue driver for liquid lipstick brands. E-commerce platform sales now represent a significant and expanding distribution share, with mobile commerce accounting for the majority of online beauty transactions in Asia Pacific. The frictionless product discovery enabled by algorithmic recommendation engines, combined with virtual try-on tools, has materially reduced purchase hesitation for new lip color products. This channel shift is compressing geographic market segmentation, enabling small and indie brands to achieve global distribution without proportional brick-and-mortar investment.

Driver 2: Premiumization and Willingness to Pay. Consumer surveys across North America and Europe consistently indicate rising willingness to allocate larger per-unit budgets to lip color products that carry premium positioning signals — including clean ingredient lists, sustainable packaging, and dermatologist-tested claims. This premiumization trend is pushing average selling prices upward, supporting revenue growth even in markets where volume growth is moderate.

Driver 3: Social Commerce and Influencer Marketing ROI. Influencer-driven campaigns for liquid lipstick products generate documented return-on-investment multiples that justify significant marketing budget allocation. Brands reporting influencer marketing as a core channel have seen new product launch sell-through rates improve by measurable double-digit percentages compared to traditional advertising-only campaigns.

Constraint 1: Raw Material Price Volatility. Key inputs including castor oil, synthetic waxes, and petroleum-derived polymers are subject to commodity price fluctuations that can compress gross margins, particularly for mid-market manufacturers with limited pricing power. This constraint is analyzed in greater depth in the supply chain section below.

Constraint 2: Regulatory Complexity Across Markets. Liquid lipstick formulations are subject to varying regulatory standards across the European Union, United States, and Asia Pacific, creating compliance costs and product reformulation requirements that can delay market entry and erode first-mover advantages.

Constraint 3: Sustainability-Related Reformulation Costs. The transition toward clean beauty formulations — avoiding parabens, phthalates, and certain synthetic colorants — imposes research and development costs and occasionally requires acceptance of shorter shelf lives or modified texture profiles, creating near-term margin pressure.

The Liquid Lipstick Market is served by a diversified competitive landscape spanning multinational conglomerates, specialized cosmetics companies, and emerging indie brands. The following profiles capture the strategic positioning of key participants:

L'Oreal: The world's largest beauty company by revenue leverages its multi-brand architecture — spanning L'Oreal Paris, Maybelline, NYX, and Lancôme — to compete across mass, masstige, and premium liquid lipstick segments simultaneously, enabling comprehensive consumer coverage and retail shelf domination.

Avon Products Inc.: Operating primarily through a direct-selling model with a global network of independent representatives, Avon targets value-conscious consumers in emerging markets including Latin America, Eastern Europe, and Africa, where its catalog-based and social selling approach maintains strong brand affinity.

Coty Inc.: Through a portfolio that includes CoverGirl, Rimmel, and licensed luxury brands, Coty competes across multiple price tiers in the liquid lipstick space, with recent strategic emphasis on digital marketing transformation and e-commerce channel acceleration.

Amorepacific Corporation: South Korea's leading cosmetics conglomerate, Amorepacific has successfully exported Korean beauty (K-beauty) liquid lip products globally through brands such as Laneige and IOPE, capitalizing on international consumer fascination with K-beauty formulation philosophies that blend skincare benefits with color.

Shiseido Company Ltd.: Japan's oldest cosmetics company competes in the premium and luxury tiers, emphasizing scientific formulation credentials, minimalist packaging aesthetics, and distribution through selective retail channels including department stores and specialty beauty retailers.

Oriflame Holding AG: Operating on a direct sales model similar to Avon, Oriflame focuses on natural ingredient positioning and sustainability claims to differentiate its liquid lipstick portfolio, targeting health-conscious consumers primarily in European and Asian emerging markets.

Christian Dior SE: Competing exclusively in the luxury segment, Dior's liquid lip products command significant price premiums through brand heritage, couture associations, and prestige retail placement, with the Dior Addict Lip Tattoo line representing a key innovation platform.

Estee Lauder Companies: Through MAC Cosmetics, Clinique, and its namesake brand, Estee Lauder addresses professional makeup artists, skincare-conscious consumers, and aspirational luxury buyers across a comprehensive liquid lip product range.

Unilever plc: Primarily engaged in adjacent personal care categories, Unilever's cosmetics presence in the liquid lipstick space is more limited but strategically relevant through select brand acquisitions and sustainability-driven reformulation initiatives.

Revlon Inc.: A legacy mass-market brand navigating financial restructuring while maintaining consumer brand recognition, Revlon's liquid lipstick range emphasizes accessible pricing and broad retail distribution as core competitive levers.

Procter and Gamble: While not a primary liquid lipstick specialist, Procter and Gamble's presence in the broader beauty category and its distribution infrastructure provide a strategic foundation from which it can extend into adjacent cosmetic segments.

January 2025: L'Oreal announced the launch of a new transfer-proof liquid lipstick line under the Infallible brand umbrella, featuring an updated polymer matrix designed to extend wear duration to 12 hours while incorporating moisturizing hyaluronic acid derivatives, signaling the brand's dual-functionality strategy.

March 2025: Amorepacific Corporation expanded its Laneige lip product distribution into 15 new international markets across Southeast Asia and the Middle East, supported by localized influencer campaigns tailored to regional beauty standards and skin tone diversity.

May 2025: Coty Inc. announced a partnership with a leading augmented reality technology provider to integrate virtual lip try-on functionality across its brand websites, aiming to reduce e-commerce return rates and improve conversion metrics for its liquid lipstick SKUs.

July 2025: Shiseido Company Ltd. unveiled a biodegradable liquid lipstick applicator system under its Shiseido brand, representing one of the first commercially viable sustainable applicator launches in the premium cosmetics tier, targeting environmentally conscious consumers in European markets.

September 2025: Revlon Inc. completed a product portfolio rationalization initiative, discontinuing 23 underperforming liquid lipstick SKUs while reinvesting resources into reformulating its core bestsellers with clean beauty-aligned ingredient profiles.

November 2025: Estee Lauder Companies reported that MAC Cosmetics' limited-edition liquid lipstick collaborations with global celebrity artists achieved sell-out status within 48 hours of launch across e-commerce channels, validating the brand's influencer co-creation strategy.

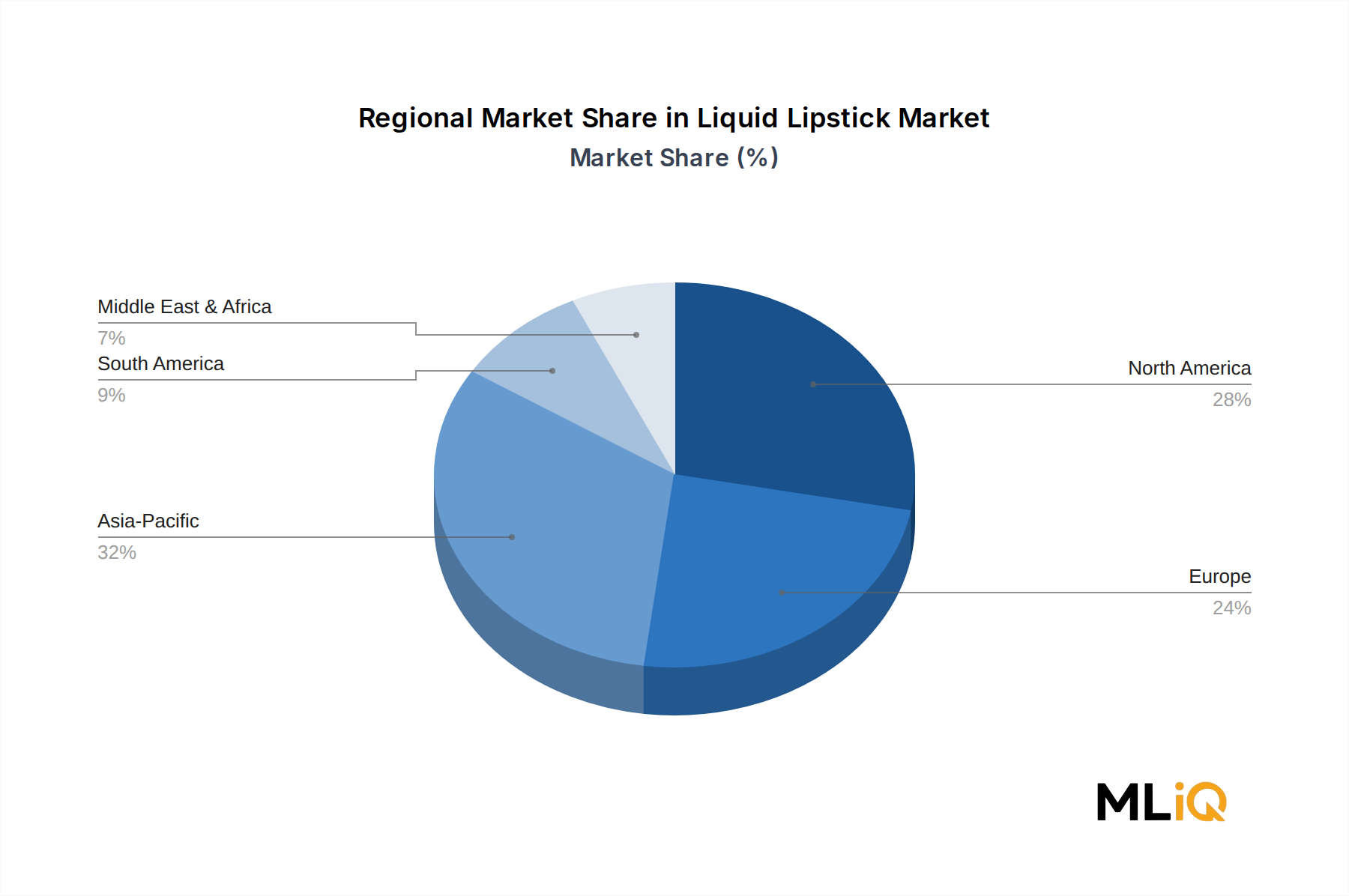

The Liquid Lipstick Market exhibits meaningful regional variation in growth rates, maturity levels, and demand drivers, reflecting divergent demographic profiles, retail infrastructure development, and cultural beauty norms.

North America: North America represents the most mature regional market, contributing an estimated 32% of global revenue in 2025. The United States is the primary revenue engine, characterized by high per-capita cosmetic spending, sophisticated omnichannel retail infrastructure, and a highly brand-literate consumer base. Regional CAGR is projected at approximately 5.4% through 2033, reflecting a market growing steadily from a large base rather than accelerating rapidly. The primary demand driver is premiumization and the clean beauty movement, with consumers actively trading up to natural-ingredient and cruelty-free liquid lipstick formulations.

Europe: Europe accounts for approximately 24% of global market value, with the United Kingdom, Germany, and France serving as the core demand centers. Regulatory rigor under EU cosmetics directives shapes formulation standards and has accelerated the transition toward compliant clean beauty formulations. Regional CAGR is estimated at 5.8%, supported by strong independent beauty retail and pharmacy channel penetration alongside growing e-commerce adoption.

Asia Pacific: Asia Pacific is both the largest and fastest-growing regional market, expected to register a CAGR of 8.7% through 2033. China, India, South Korea, and ASEAN economies collectively drive outsized growth fueled by an expanding middle class, rising beauty consciousness among younger demographics, and the pervasive influence of K-beauty trends on regional product preferences. China alone is estimated to account for the largest single-country market share within the region.

Middle East and Africa: This region is emerging as a high-potential growth frontier, with a regional CAGR projected at 7.2%. Gulf Cooperation Council countries exhibit notably high per-capita cosmetic spending relative to regional income averages, supported by cultural emphasis on personal grooming and strong demand for long-wear formulations compatible with warm climate conditions. Turkey and South Africa serve as key distribution hubs for broader regional penetration.

South America: Brazil and Argentina anchor South American demand, with a regional CAGR of approximately 6.3%. Brazil's large and beauty-engaged population, combined with a robust direct-selling channel infrastructure historically cultivated by companies such as Avon Products Inc. and Natura, provides a resilient demand foundation even amid macroeconomic volatility.

The Liquid Lipstick Market is upstream-dependent on a specific set of raw materials whose price volatility and sourcing geography introduce meaningful supply chain risk. Understanding these dynamics is essential for both manufacturers managing margin exposure and investors evaluating operational resilience.

Key raw material inputs include castor oil, a primary carrier ingredient in many liquid lipstick formulations, sourced predominantly from India and Brazil. Castor oil prices have demonstrated historical volatility correlated with monsoon season variability in India's Gujarat region, with price swings of 15–30% recorded in certain crop years. This upstream exposure is particularly acute for manufacturers with limited inventory hedging capabilities or single-source supplier relationships.

Synthetic waxes — including polyethylene wax and carnauba wax — serve as structural components in liquid-to-matte formulations. Carnauba wax, sourced almost exclusively from northeastern Brazil, has experienced tightening supply in recent cycles due to climate pattern disruptions affecting palm leaf harvests, creating upward price pressure and motivating manufacturer interest in synthetic substitutes.

Petroleum-derived polymers including acrylates copolymers and trimethylsiloxysilicate — critical for long-wear film formation — are subject to

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.9% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Liquid Lipstick Market market expansion.

Key companies in the market include L’Oreal, Avon Products Inc., Coty Inc., Amorepacific Corporation, Shiseido Company Ltd., Oriflame Holding AG, Christian Dior SE, Estee Lauder Companies, Unilever plc, Revlon Inc., Procter and Gamble.

The market segments include Type, Distribution Channel, End User.

The market size is estimated to be USD 3.8 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Liquid Lipstick Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Liquid Lipstick Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.