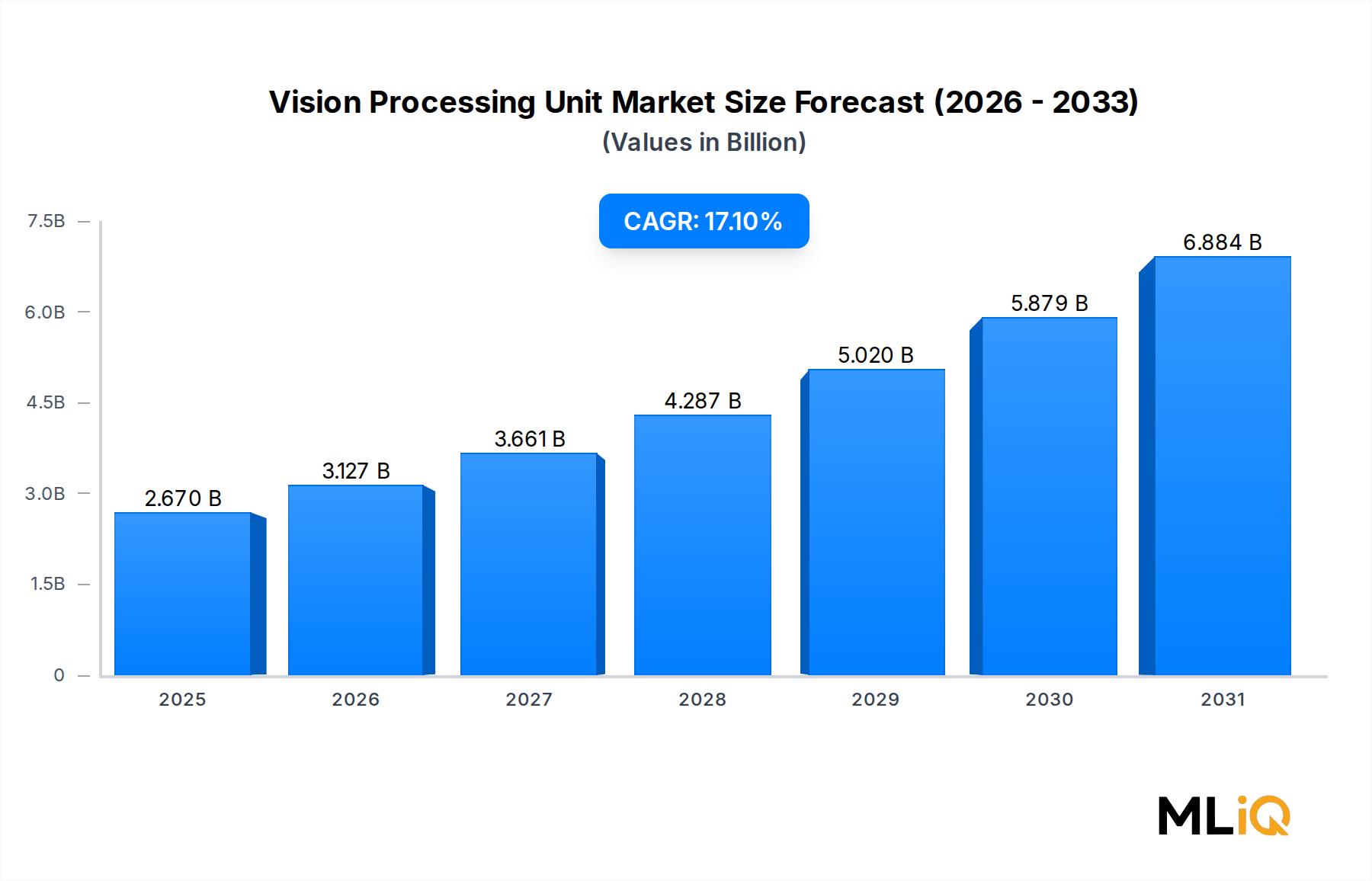

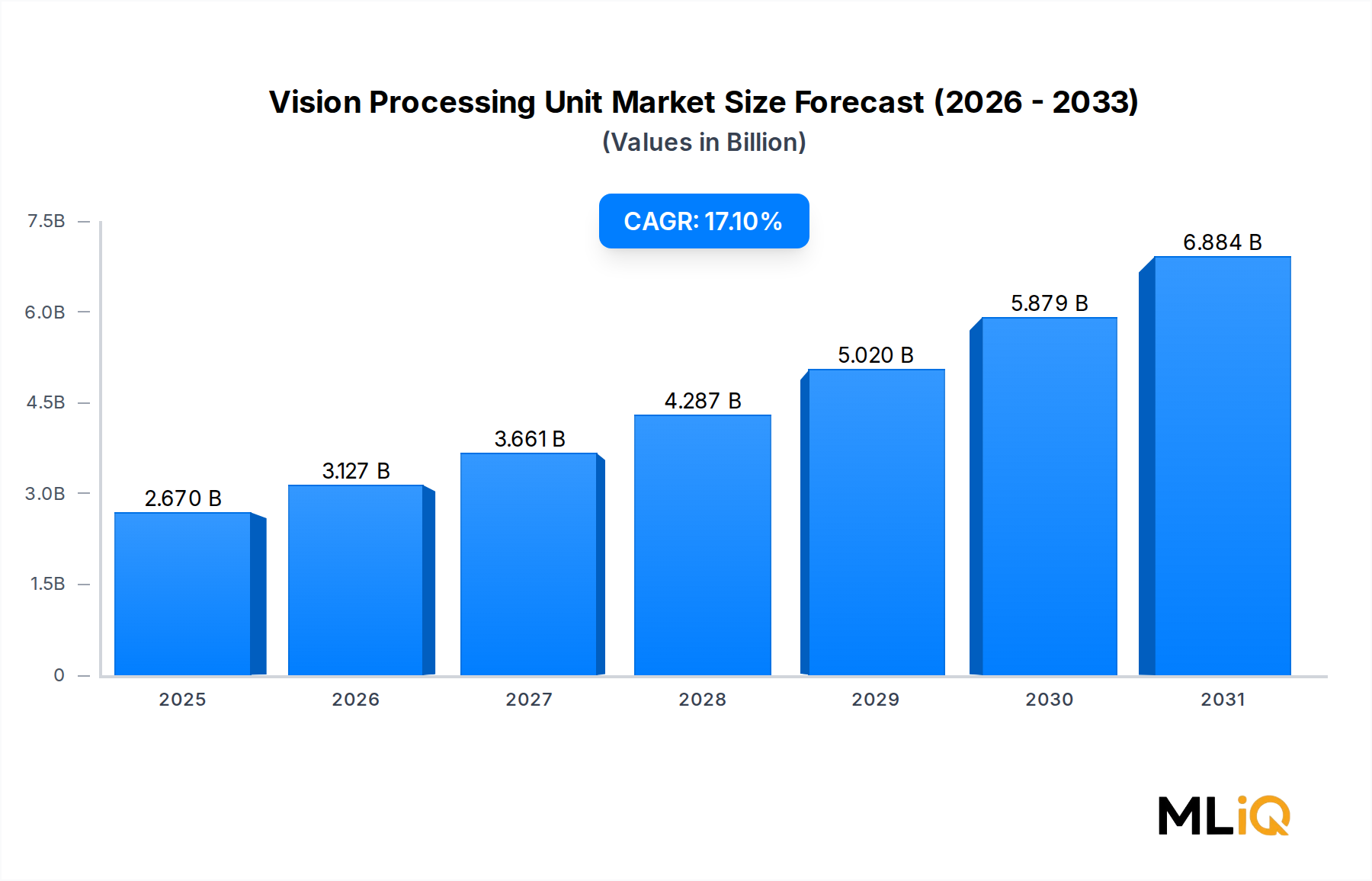

The global Vision Processing Unit Market is valued at $2.67 billion in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 17.1% through 2033, reaching an estimated $9.8 billion by the end of the forecast period. This exceptional growth trajectory positions vision processing units (VPUs) among the fastest-scaling semiconductor sub-segments globally, underpinned by converging demand from autonomous systems, artificial intelligence workloads, and edge-deployed imaging pipelines.

The core value proposition of a VPU lies in its ability to execute dense parallel visual inference tasks — object detection, semantic segmentation, optical flow estimation, and feature extraction — at significantly lower power envelopes than general-purpose CPUs or even GPUs. As AI inference migrates from the cloud to the device edge, the hardware efficiency advantages of dedicated vision processors become architecturally decisive, accelerating design wins across smartphones, automotive platforms, surveillance nodes, drones, and extended reality headsets.

Macro tailwinds reinforcing this outlook include the proliferation of multi-camera arrays in flagship smartphones, regulatory mandates expanding ADAS adoption across major automotive markets, and the rapid build-out of intelligent video analytics in urban infrastructure. The global installed base of AI-capable edge devices is expected to surpass 20 billion units by 2030, with visual perception remaining the primary sensory modality for most intelligent endpoint applications. This structural dependency on real-time image understanding translates directly into sustained VPU silicon demand.

Investment flows have intensified correspondingly. Semiconductor companies, cloud hyperscalers with custom silicon programs, and automotive Tier-1 suppliers are all channeling R&D budgets into proprietary or licensed VPU architectures. The competitive landscape is evolving from general-purpose neural network accelerators toward domain-specific silicon optimized for visual workloads — incorporating dedicated hardware for image signal processing (ISP), stereo depth engines, and sparse tensor computation.

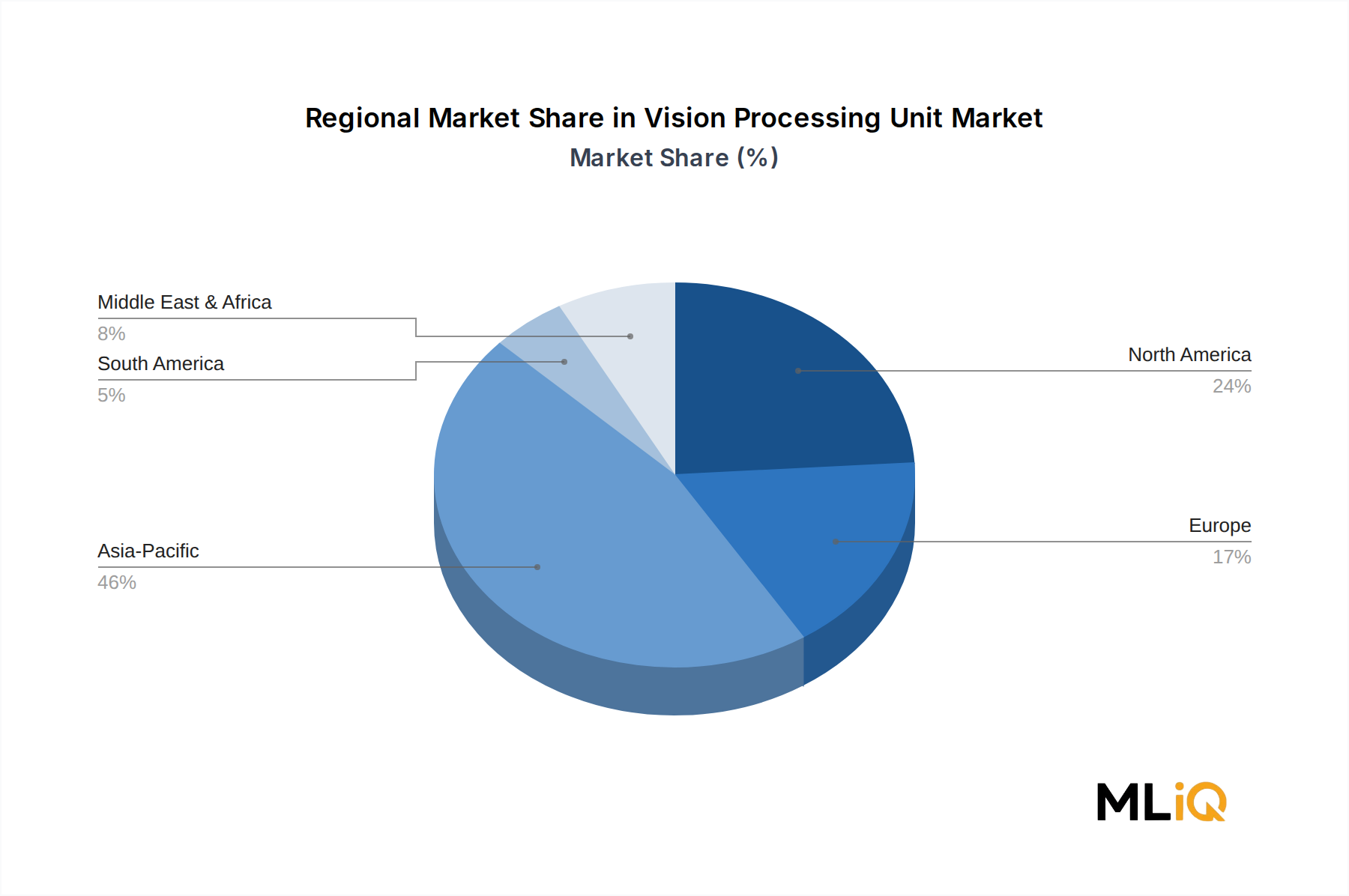

From a regional standpoint, Asia Pacific dominates production and consumption volume simultaneously, while North America leads in design innovation and software ecosystem depth. Europe's automotive-driven demand is accelerating, particularly as the region enforces increasingly stringent active safety standards.

The forward-looking outlook through 2033 is one of structural demand compounding: each successive generation of autonomous, connected, and extended-reality devices embeds a higher count of visual intelligence endpoints, each requiring a dedicated or integrated VPU core. Supply chain resilience — particularly around advanced process nodes at 5nm and below — will be the primary variable moderating the pace at which this demand is fulfilled.