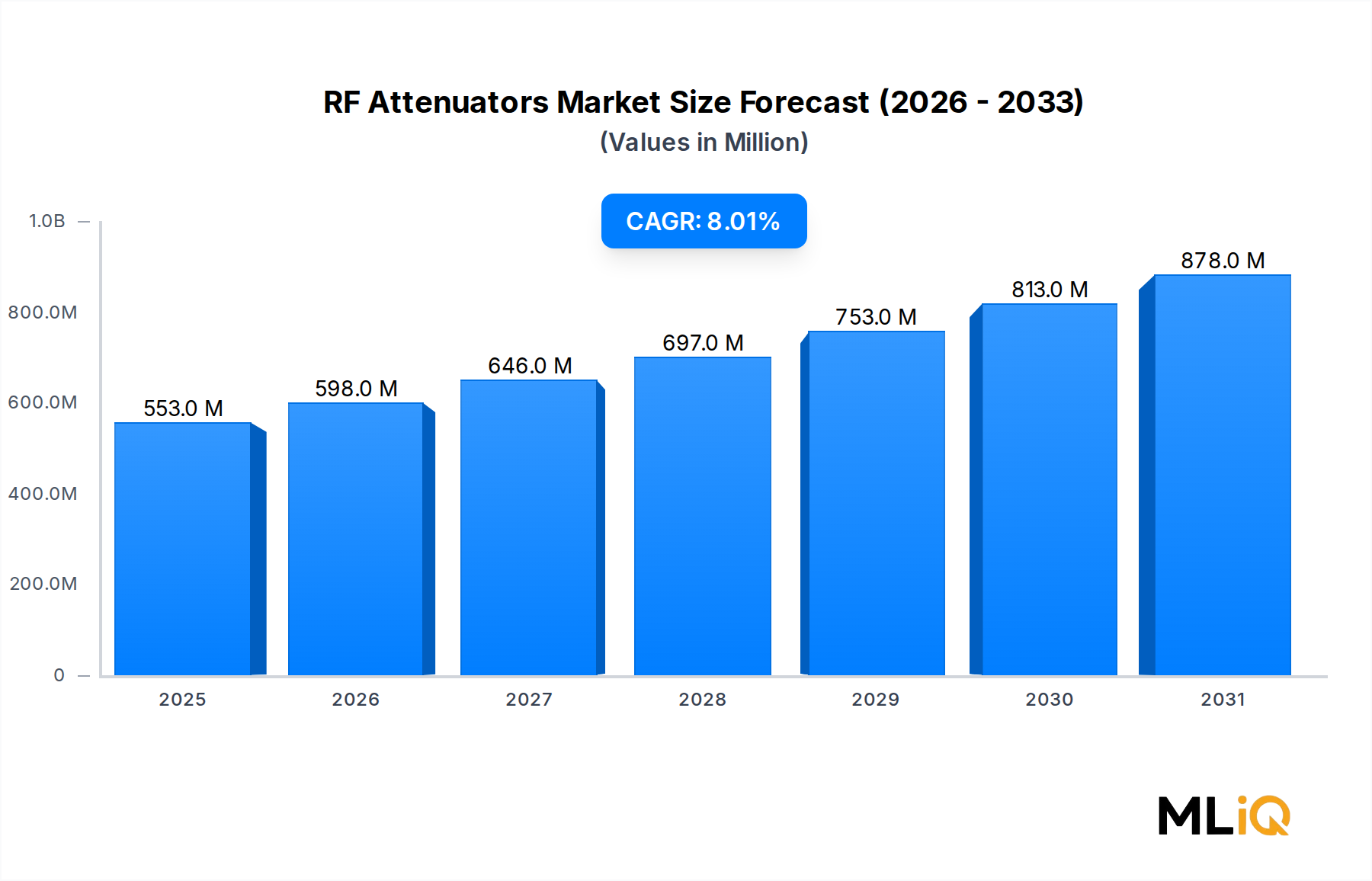

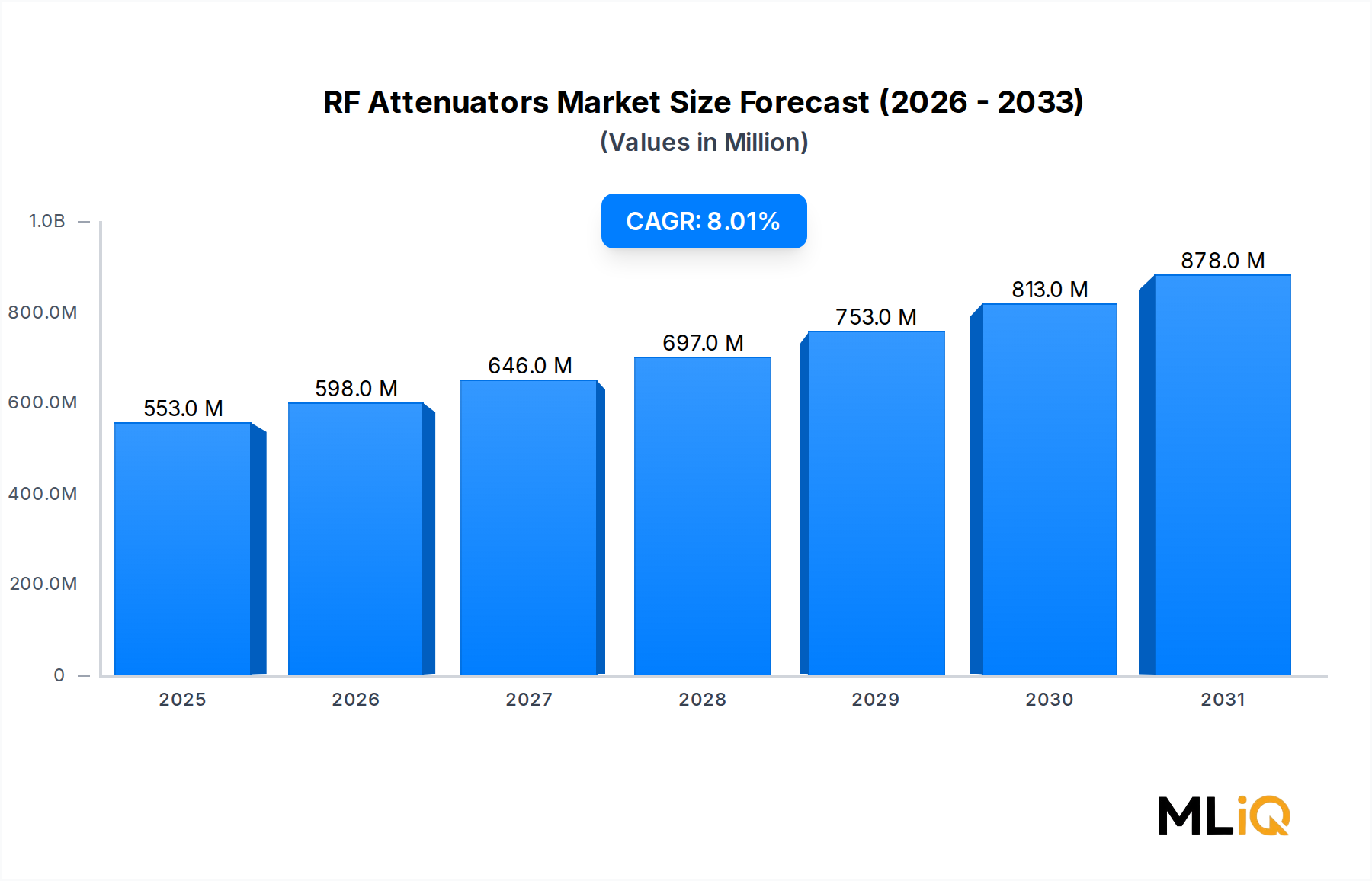

The global RF Attenuators Market is valued at $553.47 million in 2025 and is projected to expand at a compound annual growth rate (CAGR) of 8% through 2033, reaching an estimated $1,024 million by the end of the forecast period. This robust growth trajectory reflects accelerating demand across telecommunications infrastructure, aerospace and defense systems, scientific research instrumentation, and consumer electronics platforms. RF attenuators — passive components that reduce signal amplitude without distorting the waveform — are increasingly mission-critical as system designers grapple with higher frequency bands, denser spectral environments, and more stringent signal integrity requirements.

Macroeconomic tailwinds underpinning this expansion include the global rollout of 5G networks, which demands precision signal management components at millimeter-wave frequencies; escalating defense modernization budgets in the United States, Europe, and Asia-Pacific; and the proliferation of connected devices in the Internet of Things ecosystem. The migration toward higher frequency bands — particularly sub-6 GHz and mmWave 5G — creates direct demand for attenuators capable of managing signal power levels across broader bandwidths with minimal insertion loss variation.

From a segmentation standpoint, the market is bifurcated across operating type (fixed, switched, variable), physical type (chip-based, coaxial, waveguide), connector type (Type N, SMA, TNC, DIN, and others), application direction (unidirectional and bidirectional), and end-use industry (science research, consumer electronics and musical instruments, broadcasting and networking, aerospace and defense, and others). Each segmentation axis carries unique growth characteristics, with aerospace and defense and telecommunications infrastructure commanding the highest revenue premiums due to stringent performance specifications.

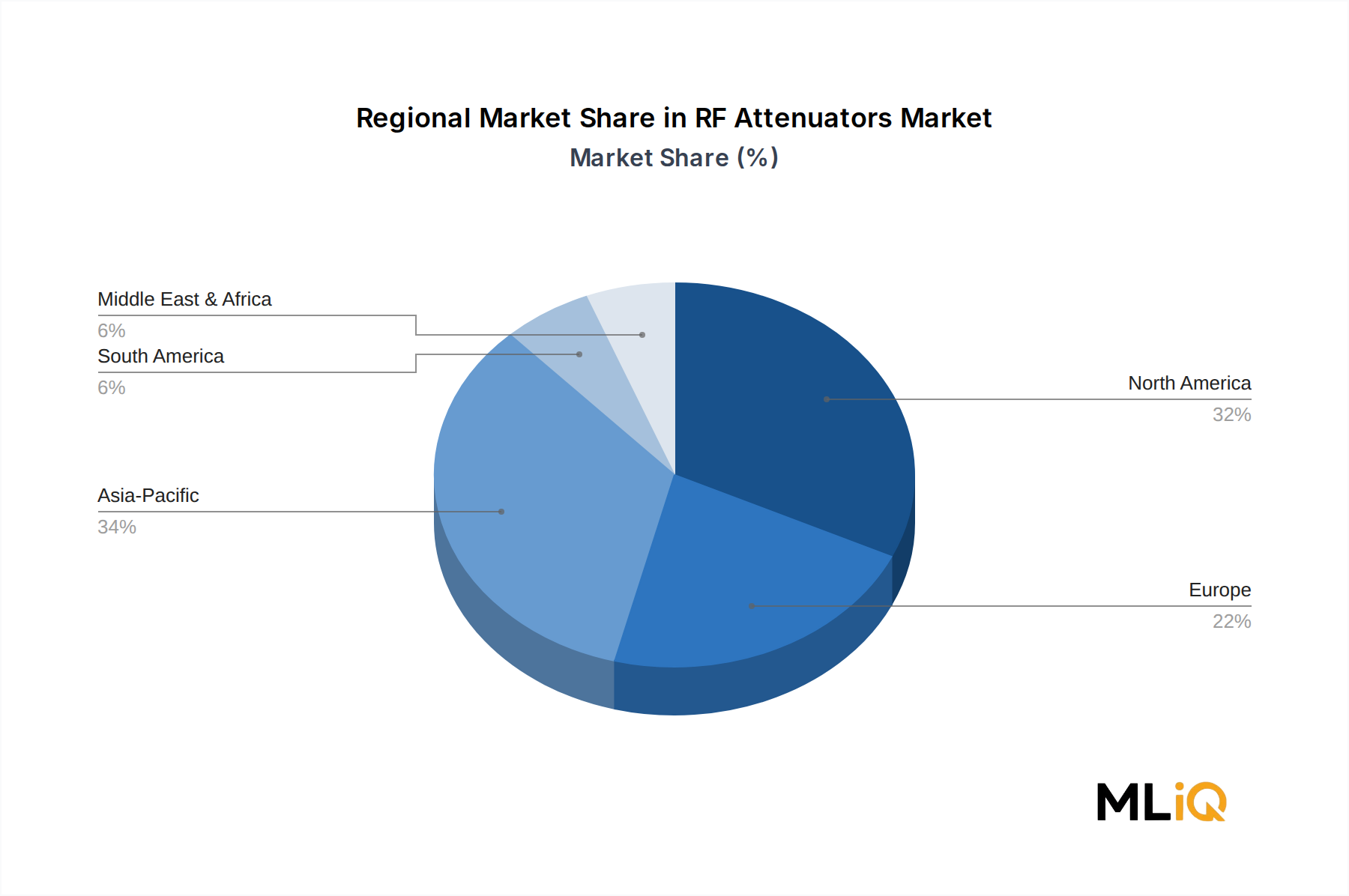

Geographically, North America retains the largest revenue share, driven by substantial defense procurement and hyperscaler data center investments. Asia-Pacific represents the fastest-growing regional market, fueled by aggressive 5G deployment in China, South Korea, and Japan, alongside burgeoning electronics manufacturing ecosystems. Europe maintains steady demand anchored by industrial automation and automotive radar applications, while Latin America, the Middle East, and Africa (LAMEA) are emerging as incremental growth pockets.

Key forward-looking themes include miniaturization of chip-based attenuator architectures to sub-millimeter form factors, integration of digitally controlled variable attenuation within RF front-end modules, and increasing adoption of surface-mount technology (SMT) compatible designs in high-volume consumer electronics. The convergence of these vectors positions the RF Attenuators Market as one of the more structurally resilient segments within the broader passive RF components landscape over the 2025–2033 horizon.