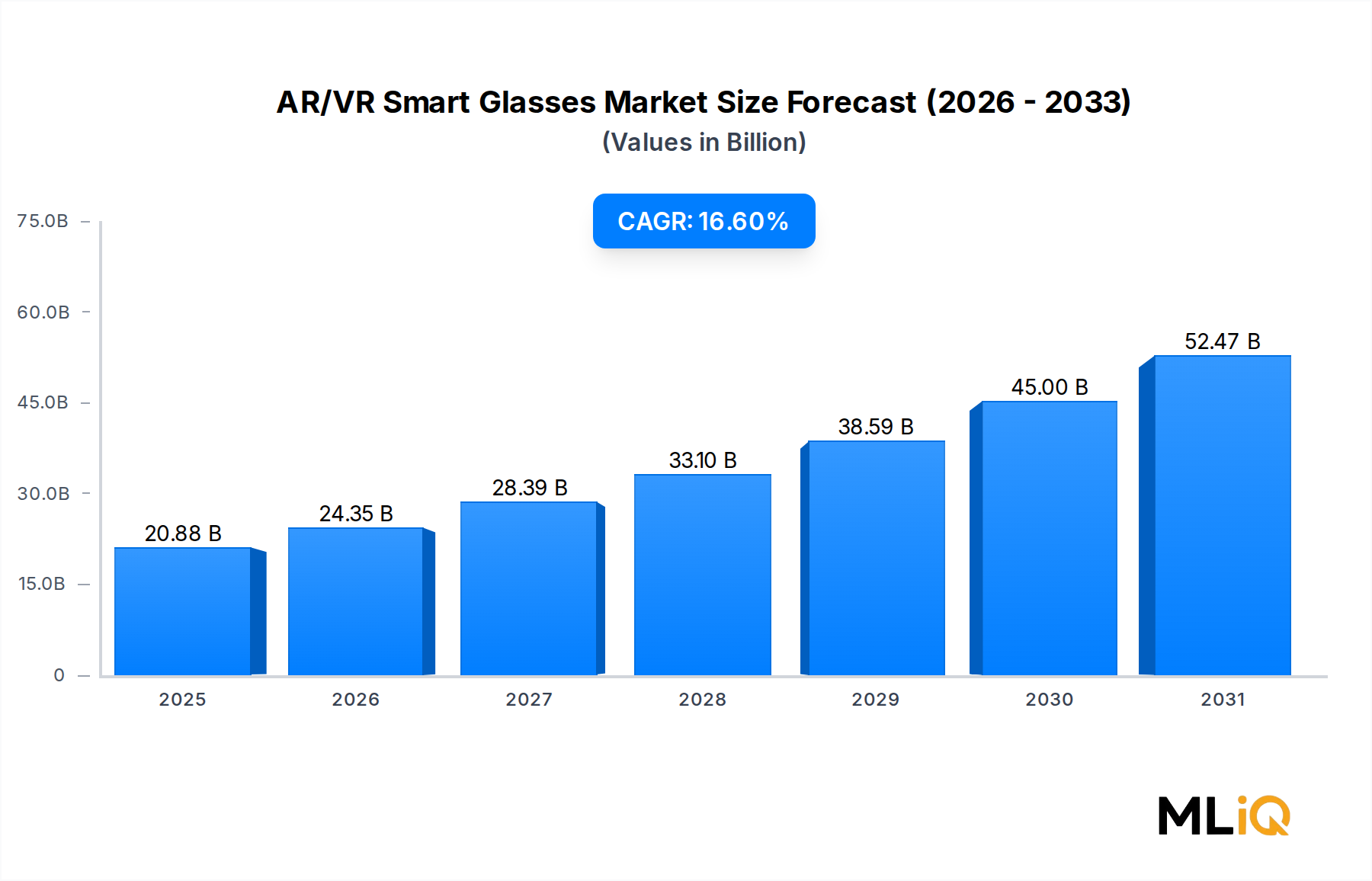

The global AR/VR Smart Glasses Market is positioned at the forefront of a profound technological inflection point. Valued at $20.88 billion as of the base assessment period, the market is projected to expand at a compound annual growth rate (CAGR) of 16.6% over the forecast horizon, reflecting robust structural demand across enterprise, consumer, healthcare, and defense verticals. This trajectory places the market among the fastest-scaling segments within the broader Semiconductor and Electronics category.

Several macro tailwinds are converging to accelerate adoption. Enterprise digital transformation initiatives are driving organizations to deploy smart glasses for remote assistance, field maintenance, warehouse operations, and real-time data overlay applications. Meanwhile, the proliferation of 5G infrastructure is removing latency constraints that previously impaired the immersive experience, enabling cloud-rendered AR content to be streamed reliably to lightweight form-factor devices. The miniaturization of high-performance processors, optical waveguide assemblies, and eye-tracking modules has significantly improved device ergonomics, making smart glasses viable for extended daily use.

On the consumer side, the gaming industry continues to generate headline demand, with next-generation mixed reality headsets and smart glasses enabling spatial gaming experiences that transcend traditional flat-screen paradigms. Healthcare and education verticals are emerging as high-value end-use segments, with clinical training simulations, surgical guidance overlays, and immersive learning environments demonstrating measurable productivity and outcomes benefits.

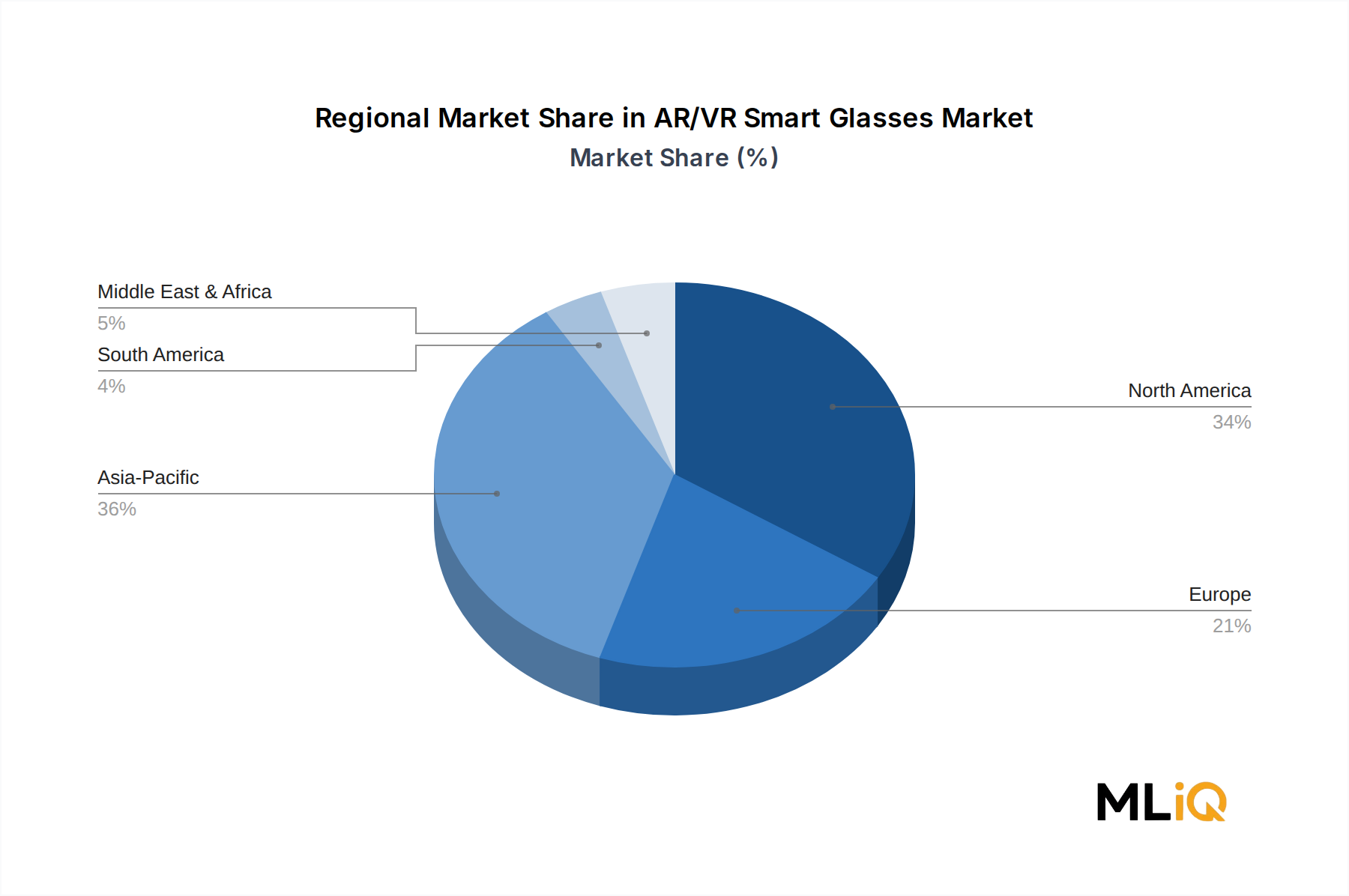

Geographically, North America holds the largest revenue share, underpinned by the concentration of leading technology developers and early enterprise adopters. Asia Pacific is the fastest-growing region, driven by aggressive technology manufacturing investment in China, South Korea, and Japan, alongside a rapidly maturing consumer electronics base in India and ASEAN nations.

From a competitive standpoint, the landscape is defined by a mix of vertically integrated technology giants and specialized optical hardware innovators. Companies such as Vuzix, Kopin Corporation, and Lumus Ltd. are competing on optical subsystem performance, while platform ecosystems are increasingly differentiating market positions.

Looking forward, the convergence of generative AI with spatial computing interfaces is expected to unlock a new class of context-aware smart glasses capable of real-time environment interpretation, object recognition, and natural language interaction. This positions the AR/VR Smart Glasses Market as a foundational layer for the next generation of human-computer interaction, with commercialization momentum accelerating through 2026 and beyond.