Among all product type segments, the blood glucose sensor patch sub-segment commands the largest revenue share within the sensor patch market, and its dominance is both structural and self-reinforcing. The global burden of diabetes — affecting approximately 537 million adults as of 2021 and forecast to reach 783 million by 2045 according to International Diabetes Federation data — creates an essentially captive and expanding addressable market that no other sensor modality can currently match in scale or clinical urgency.

Blood glucose sensor patches, particularly those enabling continuous glucose monitoring (CGM), represent the most commercially mature form factor in the broader product landscape. Unlike episodic fingerstick glucometry, CGM-enabled patches deliver interstitial glucose readings at intervals as frequent as every 1–5 minutes, generating dense longitudinal datasets that support both individual glycemic management and population-level clinical insights. This clinical superiority over traditional methods has driven rapid adoption among both Type 1 and Type 2 diabetic populations, as well as pre-diabetic individuals engaged in metabolic health monitoring.

The Continuous Glucose Monitoring Market, of which CGM-enabled sensor patches form the core hardware component, has seen particularly aggressive investment, with device approval timelines shortening materially as regulatory bodies in the United States, European Union, and Asia Pacific have developed dedicated pathways for wearable glucose monitoring technologies. The U.S. Food and Drug Administration's designation of certain CGM devices as integrated CGM (iCGM) systems has further catalyzed adoption by enabling interoperability with insulin pumps and automated insulin delivery systems.

DexCom, Inc. is arguably the benchmark competitor in this segment, with its G7 platform achieving a 10-day wear duration and a MARD (mean absolute relative difference) of approximately 8.2%, setting a high bar for accuracy in ambulatory settings. Abbott Laboratories has emerged as a formidable challenger through its FreeStyle Libre platform, which leverages a flash CGM architecture — eliminating the need for calibration fingersticks — and has achieved particularly strong penetration in European markets due to favorable reimbursement dynamics.

Medtronic PLC, leveraging its integrated diabetes management ecosystem, competes through sensor-augmented pump therapy, positioning its CGM patches as components of closed-loop systems rather than standalone diagnostics. This systems-integration strategy differentiates Medtronic's offering in hospital and endocrinology clinic channels where comprehensive diabetes management platforms are preferred.

The blood glucose segment's revenue share is consolidating rather than fragmenting, driven by the high cost of regulatory compliance and the clinical data requirements necessary to achieve reimbursement. This creates substantial barriers to entry for new market participants, even as it validates the established players' competitive moats. The segment is also benefiting from the broader growth of the Wearable Medical Devices Market, with glucose patches increasingly marketed to wellness-conscious consumers alongside clinical diabetic populations.

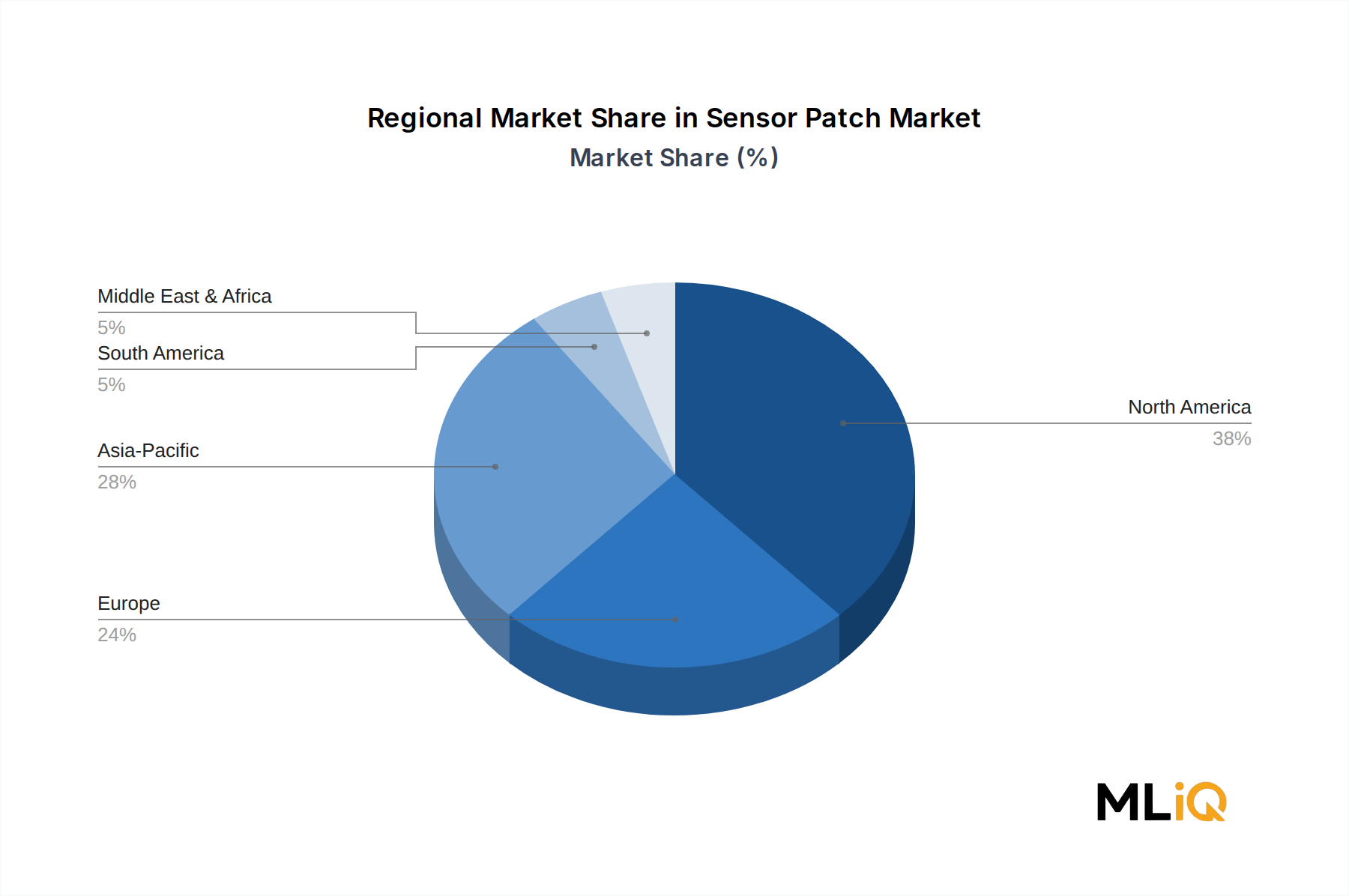

Geographically, North America accounts for the majority of blood glucose patch revenues, attributable to the high prevalence of diabetes, strong reimbursement coverage under Medicare and private insurance for CGM devices, and a well-developed digital health infrastructure. However, Asia Pacific is emerging as the fastest-growing sub-regional market, particularly in China and India, where the diabetes epidemic is expanding at alarming rates and healthcare systems are actively investing in remote monitoring capabilities to reduce hospitalization costs.

The segment's trajectory indicates that its share within the overall sensor patch market will remain dominant through at least 2028, after which ECG and multi-parameter patches may begin to erode its relative share as those technologies achieve comparable clinical maturity.