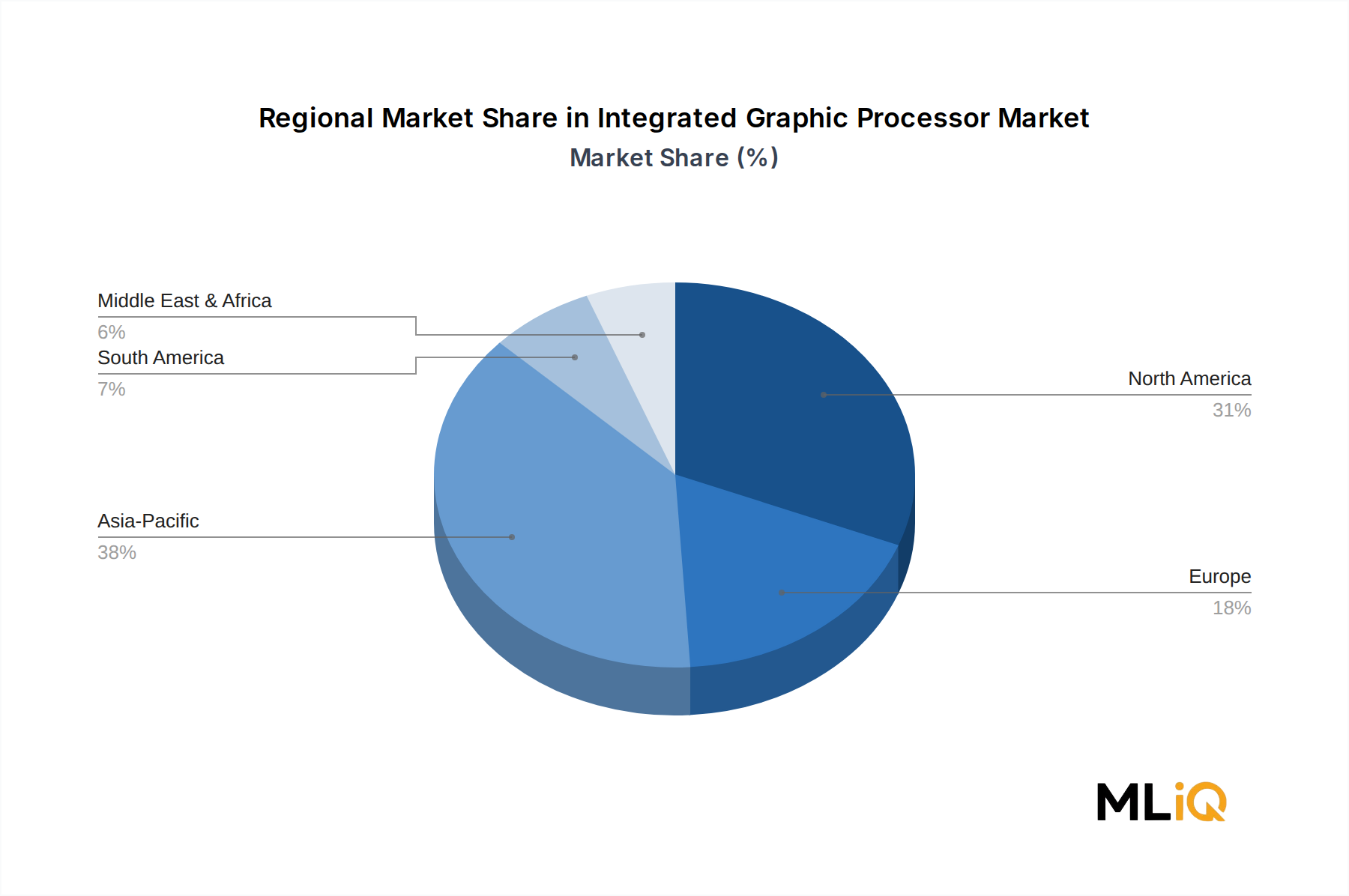

The Integrated Graphic Processor Market exhibits meaningfully differentiated regional growth profiles, driven by distinct end-market compositions, infrastructure investment cycles, and policy environments.

Asia Pacific is both the largest revenue contributor and the fastest-growing region within the Integrated Graphic Processor Market. China, Japan, South Korea, and India collectively drive the majority of iGPU-bearing SoC fabrication, system assembly, and end consumption. China's domestic semiconductor ambitions, supported by state-directed investment programs, are stimulating local iGPU IP development and foundry capacity expansion. India's rapidly growing consumer electronics and smartphone market, combined with government-backed semiconductor incentive schemes, positions it as a high-growth demand pocket. The Asia Pacific region is expected to sustain a CAGR meaningfully above the global average, potentially exceeding 32% through 2033, anchored by AI device proliferation and automotive electronics growth across ASEAN markets.

North America represents the most technologically mature regional market, with the United States serving as the global epicenter of iGPU architecture development. Intel, AMD, and NVIDIA all conduct primary GPU IP research and development in the United States, while hyperscale cloud operators headquartered domestically represent a structurally significant procurement channel. North America's iGPU market is characterized by higher average selling prices, premium system configurations, and above-average AI PC adoption rates. Revenue share for North America is estimated in the range of 28–32% of global total in 2024.

Europe demonstrates a more measured but structurally sound growth profile, with Germany, the United Kingdom, and France leading regional demand through automotive semiconductor procurement, industrial automation, and enterprise computing refresh cycles. The European Chips Act is catalyzing investment in local semiconductor design and manufacturing, which may incrementally reduce import dependence on Asian foundry capacity over the forecast horizon. Europe's iGPU CAGR is estimated at approximately 24–26% through 2033.

The Middle East and Africa region is in an early growth phase, with demand concentrated in GCC nations investing heavily in smart city infrastructure, AI-enabled surveillance systems, and consumer electronics retail expansion. South Africa and Turkey represent secondary demand centers with growing technology adoption. Overall regional revenue contribution remains modest but is expected to accelerate as broadband penetration and device ownership rates rise.

South America, led by Brazil and Argentina, reflects a price-sensitive consumer base where integrated graphics adoption is driven primarily by cost-optimized laptops and educational computing programs, with growth constrained by macroeconomic volatility and currency risk.