Commercial Mortality Insurance Dominance in the Livestock Insurance Market

Among the key product type segments, commercial mortality insurance represents the single largest revenue contributor within the Livestock Insurance Market, consistently accounting for the majority of gross written premiums globally. This segment's dominance is rooted in several structural, financial, and regulatory factors that reinforce its primacy across both developed and emerging market contexts.

Commercial mortality insurance provides indemnification to policyholders — primarily large-scale dairy operators, cattle ranchers, swine producers, and integrated poultry businesses — in the event of the death of a covered animal due to accident, illness, or humane slaughter necessitated by disease. The per-head insured value for commercial livestock is substantially higher than that of subsistence animals, generating larger average premiums and making the commercial segment inherently more attractive to insurers from a unit economics perspective.

In North America, commercial mortality products underwritten by carriers such as Nationwide, The Hartford, and Farm Bureau Financial Services are embedded within broader farm package policies, enabling cross-selling efficiencies and reducing customer acquisition costs. These integrated offerings bundle property, liability, and livestock mortality coverage into a single policy, driving higher retention rates and improving loss ratio predictability through portfolio diversification.

In Europe, Lloyd's syndicates and specialist agricultural insurers have developed bespoke commercial mortality products for high-value equine and bovine animals, where per-head insured values can reach tens of thousands of dollars. The sophistication of these products — including surgical and veterinary fee riders — adds premium density without proportionally increasing claims frequency, enhancing underwriting profitability.

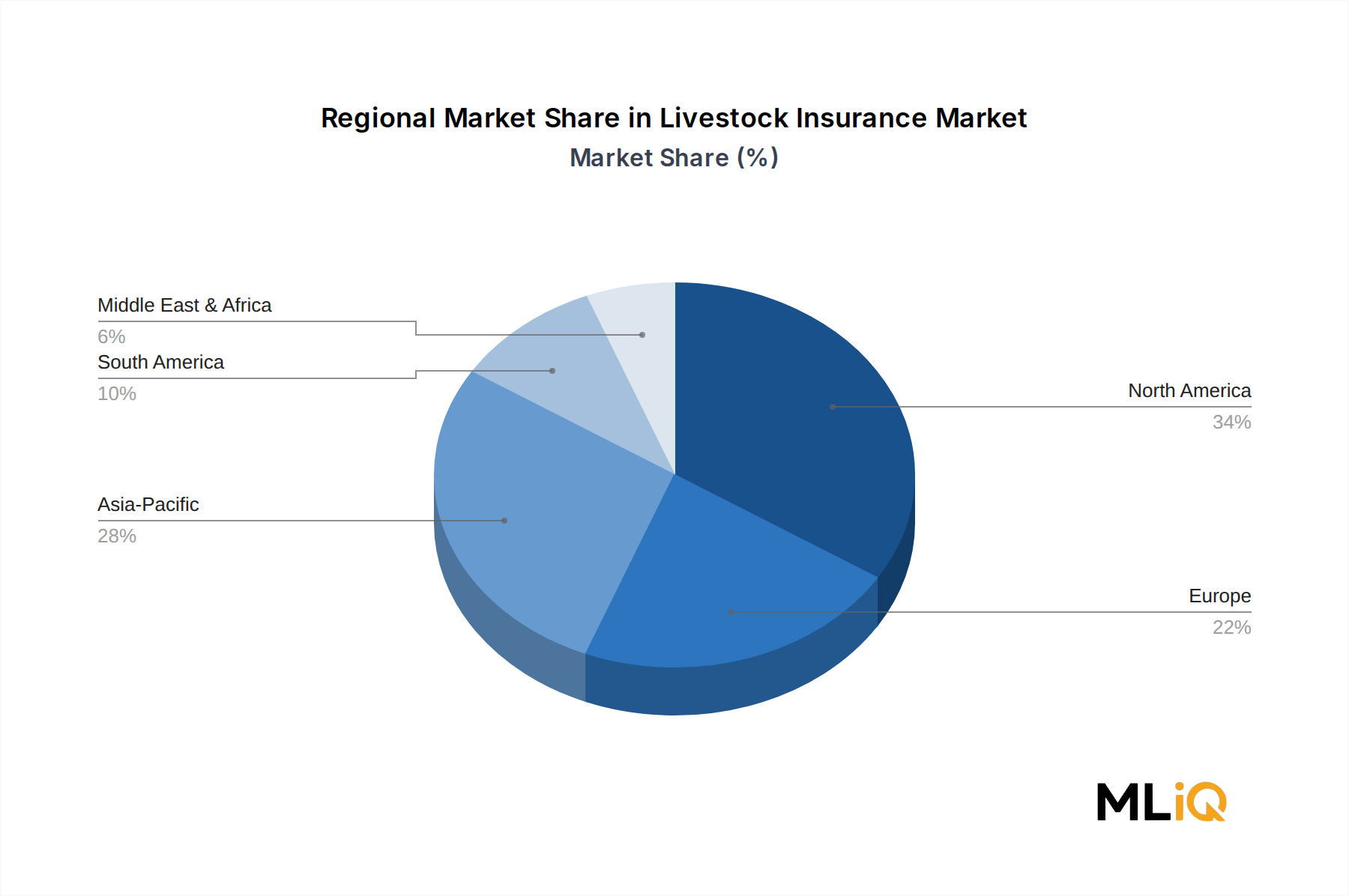

Asia Pacific, led by China and India, presents a more nuanced picture. While government-subsidized schemes in these countries often target smallholder and non-commercial segments, the rapid commercialization of livestock production — particularly in China's swine and poultry sectors — is generating a fast-growing commercial mortality insurance segment. China's hog sector, the world's largest by headcount, experienced significant disruption from African Swine Fever between 2018 and 2021, a period that dramatically raised awareness of mortality risk among commercial producers and accelerated insurance uptake.

Key players dominating the commercial mortality segment include Liberty Mutual, AXA XL, ICICI Lombard General Insurance Company Limited, and HDFC ERGO, each of which has invested in proprietary actuarial models calibrated to regional disease prevalence data, mortality curves by species, and macroeconomic livestock price cycles. The sophistication of these models represents a meaningful competitive moat, as accurate pricing is critical to avoiding adverse selection.

The commercial mortality segment's share is currently consolidating rather than expanding as a proportion of total market premiums, as the non-commercial and index-based segments grow faster off a lower base. Nevertheless, in absolute dollar terms, commercial mortality premiums are projected to continue growing at approximately 7.2% CAGR through 2033, supported by rising livestock asset values, more stringent lending requirements from agricultural banks, and the gradual adoption of electronic livestock identification systems that reduce moral hazard and facilitate claims verification. The transition from paper-based to digital policy administration — increasingly driven by Farm Management Software Market platforms that integrate insurance data with herd management records — is further reducing operational costs and improving the commercial mortality segment's scalability.