1. What are the major growth drivers for the Tire Mold Market market?

Factors such as are projected to boost the Tire Mold Market market expansion.

+1 2315155523

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

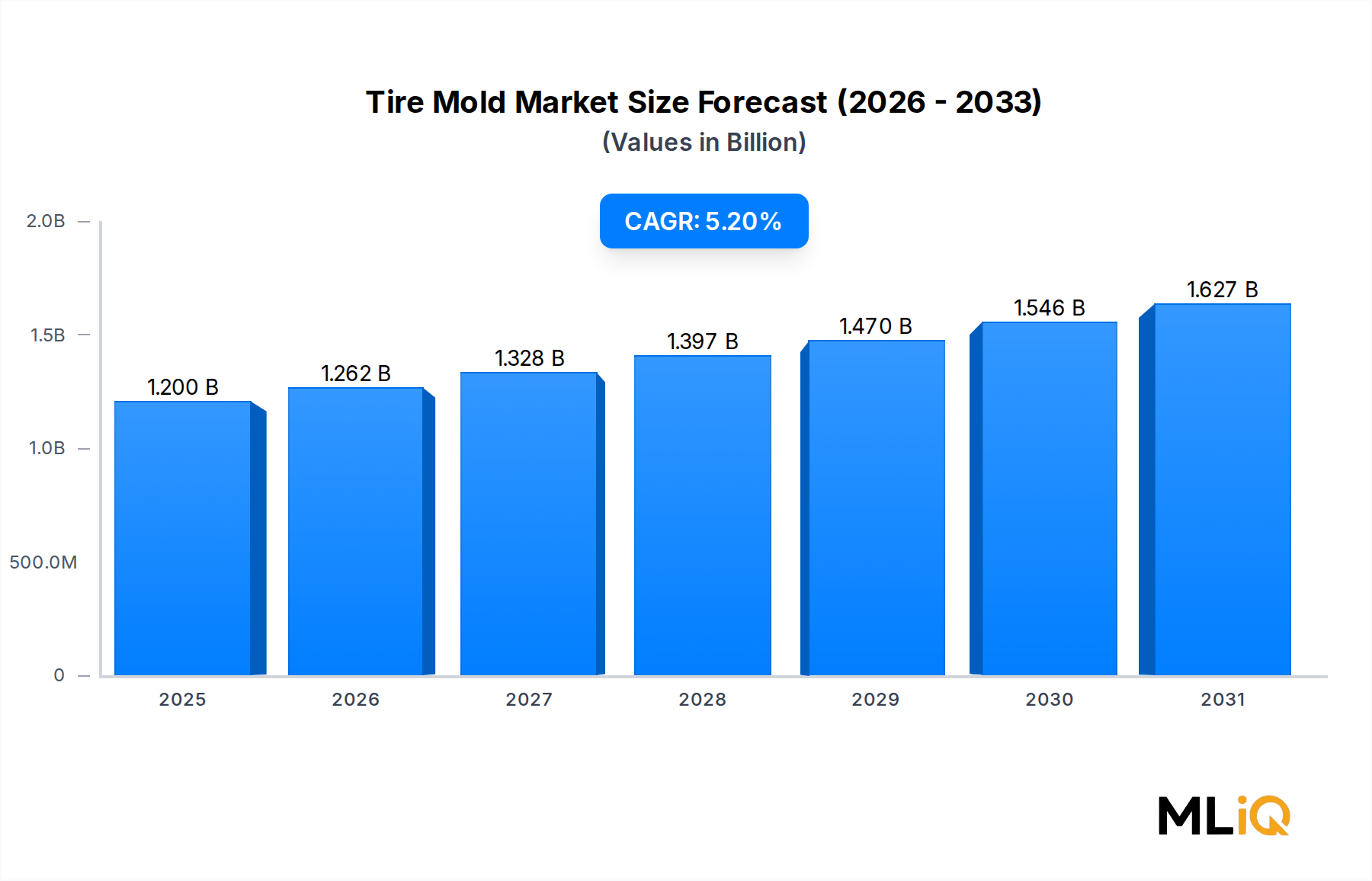

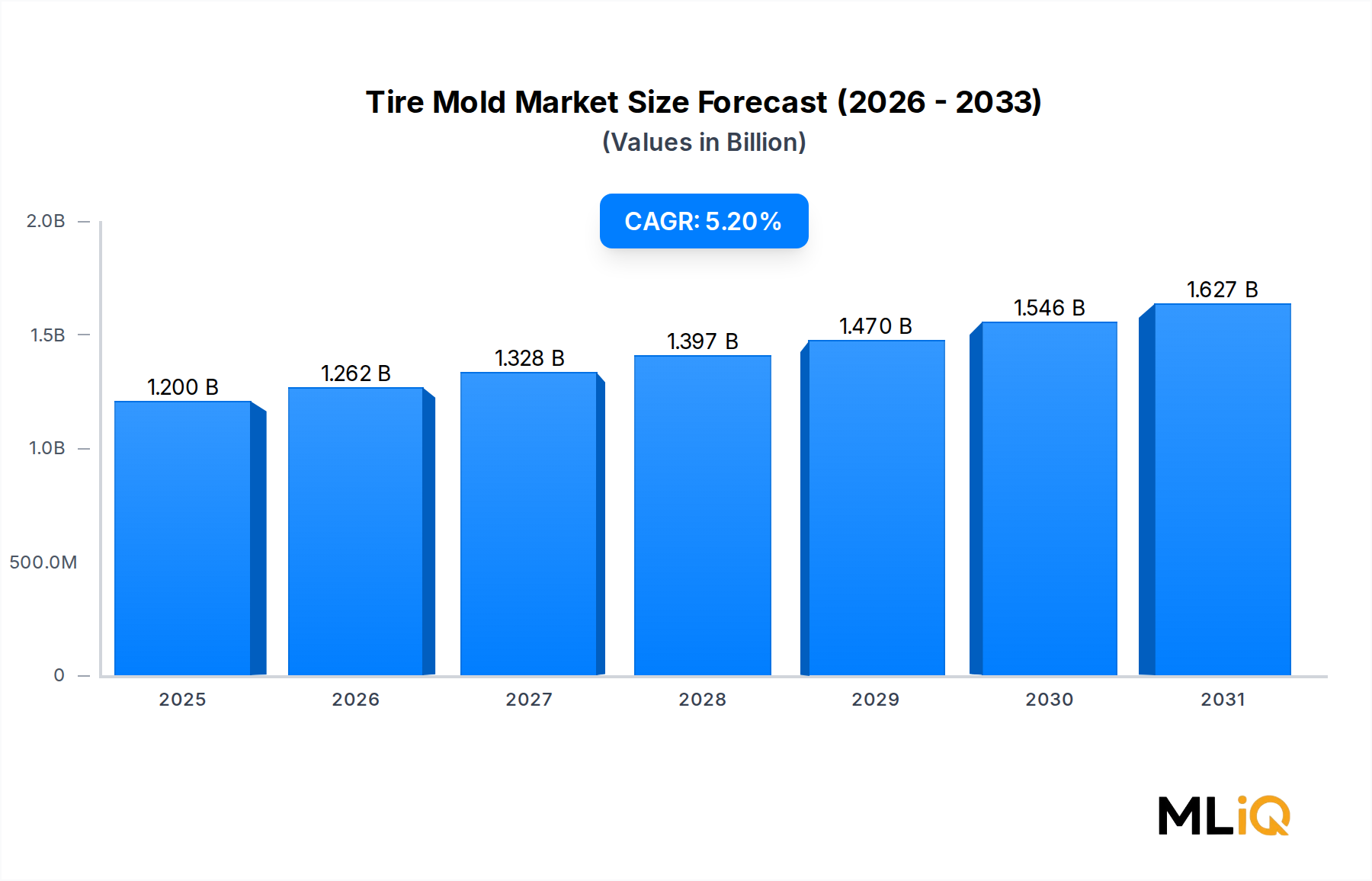

The global tire mold market was valued at $1.2 billion in 2024 and is projected to expand at a compound annual growth rate (CAGR) of 5.2% through 2033, reflecting sustained demand from automotive manufacturing, commercial transportation, and specialty off-road vehicle segments. This market sits at the intersection of precision engineering, materials science, and automotive production scalability, making it a technically intensive and capital-demanding sector.

Key demand drivers include the rapid proliferation of electric vehicles (EVs), which require performance-optimized tire geometries to compensate for higher torque output and vehicle weight. As global EV penetration accelerates past 15% of new car sales across major markets in 2024, tire OEMs are investing in next-generation mold tooling capable of producing tires with lower rolling resistance profiles and enhanced load ratings. This directly fuels replacement and capacity-expansion orders for tire mold manufacturers.

Macroeconomic tailwinds supporting the market include growing vehicle parc sizes in Asia Pacific and South America, infrastructure buildout stimulating demand for off-the-road (OTR) tires in mining and construction, and fleet expansion in logistics and e-commerce driving truck and bus radial (TBR) tire production. China remains the world's largest tire producer, accounting for roughly 60% of global tire output, which concentrates a substantial portion of mold procurement activity in Asia Pacific.

On the supply side, the market benefits from ongoing investments in automated manufacturing processes, high-precision CNC engraving, and electro-discharge machining (EDM) that reduce lead times and improve mold dimensional accuracy. These technological improvements reduce per-unit costs over mold lifecycle, incentivizing tire manufacturers to source advanced tooling rather than maintain legacy mold inventories.

Looking ahead to 2033, the market is expected to surpass $1.9 billion in valuation, driven by mold replacement cycles—typically 3 to 7 years depending on tire type and production volume—combined with greenfield tire plant investments in Southeast Asia, India, and Eastern Europe. The transition toward sustainable tire compounds, including silica-based and bio-sourced rubber formulations, also demands updated mold surface treatments and venting configurations, creating a recurring upgrade cycle that sustains revenue momentum well beyond initial equipment procurement.

In summary, the tire mold market is entering a period of technology-led differentiation, where manufacturers capable of delivering intelligent, precision-engineered mold solutions at competitive lead times will command premium margins and long-term customer retention.

Within the tire mold market, segmented molds represent the dominant product type by revenue share, accounting for an estimated 65% to 70% of total market value as of 2024. This structural dominance is rooted in the technical superiority of segmented molds for high-volume radial tire production, which constitutes the majority of global tire output across passenger car, truck, and specialty segments.

Segmented molds—also referred to as sector molds—consist of multiple interlocking segments that open radially during the tire curing cycle, allowing precise tread pattern transfer and enabling complex sipe geometries, asymmetric tread designs, and multi-radius shoulder profiles that two-piece molds cannot economically replicate. The mechanical precision required to maintain dimensional consistency across thousands of cure cycles positions segmented molds as the tooling of choice for premium and performance tire applications, where tread pattern fidelity directly influences tire classification and regulatory compliance.

From a manufacturing standpoint, segmented molds facilitate higher throughput by enabling rapid tire extraction without manual repositioning, which reduces cure press downtime and improves overall equipment effectiveness (OEE) on high-speed production lines. Major tire manufacturers operating facilities with cure press utilization targets above 85% consistently prefer segmented tooling to meet production scheduling requirements.

Key players driving revenue in this segment include Himile Mechanical Science & Technology (Shandong) Co., Ltd., which has established a commanding position in China and expanded internationally through precision CNC mold manufacturing capabilities and a broad customer base spanning Tier 1 global tire brands. Greatoo Intelligent Equipment Inc. similarly leverages integration across the tire equipment value chain to offer segmented molds as part of bundled intelligent manufacturing solutions. Herbert Maschinen- und Anlagenbau GmbH & Co. KG brings European precision engineering standards to high-specification segmented mold contracts, serving customers with demanding tolerances in performance and motorsport tire categories.

The segmented mold segment's market share is consolidating rather than expanding proportionally, as two-piece molds retain relevance for bias-ply tire production in developing markets and for certain agricultural and industrial tire categories where tread design complexity is lower. However, the absolute revenue contribution of segmented molds continues to grow in line with overall market expansion, and the increasing design complexity of modern tires—driven by EV-specific performance requirements and regulation-mandated wet grip and noise standards—structurally reinforces segmented mold dominance.

Investments in automated mold assembly verification, laser engraving for sipe accuracy, and aluminum alloy mold bodies (which reduce thermal mass and improve cure uniformity) are predominantly concentrated in the segmented mold sub-segment, further widening the technology gap relative to two-piece alternatives. Manufacturers that can deliver segmented molds with vent wire precision below 0.1 mm and surface roughness Ra below 0.8 μm command a significant pricing premium and benefit from tighter customer retention due to the high switching costs associated with qualifying new mold suppliers for large-volume production lines.

The tire mold market is propelled by a defined set of quantifiable drivers while navigating structural constraints that moderate near-term growth velocity.

Driver 1 — Global Tire Production Volume Growth: Global tire production is projected to reach approximately 3.5 billion units annually by 2027, up from roughly 3.0 billion units in 2023, according to industry trade association estimates. Each percentage point increase in tire production volume translates directly into incremental mold procurement, both for new capacity and as replacement of worn tooling on existing cure presses.

Driver 2 — Electric Vehicle Fleet Expansion: EV-specific tires require modified tread compounds and construction architectures to address higher instantaneous torque and reduced acoustic noise requirements. Tire manufacturers have indicated capital expenditure allocations of 15% to 20% of mold budgets specifically for EV-compatible tooling upgrades in 2024 and 2025, creating an accelerated replacement cycle within the existing installed base.

Driver 3 — Greenfield Tire Plant Investments in Asia Pacific and India: India's tire industry capital expenditure exceeded $1.5 billion cumulatively between 2021 and 2024, with multiple new greenfield plants requiring complete mold tooling packages. This represents a high-value, front-loaded procurement wave for mold suppliers with regional manufacturing or supply chain presence.

Constraint 1 — Raw Material Cost Volatility: Mold manufacturing is heavily dependent on tool steel and aluminum alloys. Tool Steel Market pricing fluctuated by 18% to 22% between 2021 and 2023 due to energy cost shocks in European steel production and supply chain disruptions, compressing mold manufacturer margins and elongating project budgets for tire plant procurement teams.

Constraint 2 — Long Qualification Cycles: New mold supplier qualification by Tier 1 tire manufacturers typically requires 12 to 18 months of validation trials, limiting the speed at which new entrants or existing suppliers can capture incremental market share, even when capacity expansions are underway.

Constraint 3 — Skilled Labor Scarcity: High-precision mold engraving and EDM operations require specialized technicians whose supply is constrained globally, with estimated shortfalls of 20% to 30% of required workforce in key manufacturing hubs as of 2024, creating bottlenecks in production capacity scaling.

The competitive landscape of the tire mold market is moderately consolidated at the premium tier, with Chinese manufacturers dominating volume segments and European and Japanese firms retaining competitive advantage in high-specification applications.

QINGDAO YUANTONG MACHINERY CO., LTD.: A major Chinese tire mold manufacturer with diversified capabilities across segmented and two-piece mold types, serving both domestic and export markets with competitive lead times and cost structures.

HERBERT MASCHINEN- UND ANLAGENBAU GMBH & CO. KG: A German precision engineering firm specializing in high-specification tire mold machinery and tooling solutions, with strong positioning in European OEM and motorsport tire manufacturing supply chains.

A-Z GMBH: A European mold technology company offering customized tire mold solutions with emphasis on precision dimensional control and surface quality for performance tire applications.

ANHUI WIDE WAY MOULD CO., LTD.: A Chinese mold manufacturer with an expanding international footprint, leveraging cost-competitive manufacturing and growing capabilities in aluminum alloy segmented mold production.

ANHUI MCGILLMOULD CO., LTD.: Specializes in rubber mold technology with a product portfolio spanning passenger car and commercial vehicle tire mold segments, supported by modern CNC machining infrastructure.

GREATOO INTELLIGENT EQUIPMENT INC.: A vertically integrated Chinese equipment manufacturer combining tire mold production with intelligent vulcanization press systems, enabling bundled solution sales to large-scale tire plant customers.

MK TECHNOLOGY CORP.: A technology-focused mold manufacturer with expertise in precision sipe blade integration and advanced venting solutions for next-generation tread designs.

KING MACHINE: Offers comprehensive tire mold and tire building equipment solutions, with a commercial strategy targeting mid-tier tire manufacturers in emerging markets seeking cost-effective tooling packages.

SHINKO MOLD INDUSTRIAL CO., LTD.: A Japanese precision mold manufacturer recognized for exacting quality standards in passenger car radial tire molds, maintaining long-term supply relationships with leading Japanese and South Korean tire OEMs.

HIMILE MECHANICAL SCIENCE & TECHNOLOGY (SHANDONG) CO., LTD.: One of the largest global tire mold manufacturers by revenue, with extensive capacity in segmented mold production, a diversified global client base, and active investment in intelligent mold manufacturing technologies.

Q1 2023: Himile Mechanical Science & Technology expanded its Shandong manufacturing campus by 35,000 square meters, increasing annual segmented mold production capacity by an estimated 20% to address growing order backlogs from Asian and European tire manufacturers investing in EV tire tooling.

Q2 2023: Greatoo Intelligent Equipment Inc. announced a strategic partnership with a major Chinese tire group to co-develop intelligent cure mold systems incorporating embedded temperature sensing for real-time cure cycle optimization, marking a significant step toward digitally connected mold tooling.

Q3 2023: European Union regulatory updates to tire labeling standards (EU Regulation 2020/740 enforcement expansion) prompted accelerated mold replacement orders from manufacturers needing to update tread designs to achieve higher wet grip and fuel efficiency classifications.

Q4 2023: India's Apollo Tyres confirmed a new greenfield plant in Andhra Pradesh requiring a complete mold tooling package valued in excess of $50 million, attracting competitive bids from both Chinese and European mold suppliers.

Q1 2024: Anhui Wide Way Mould Co. secured export contracts to Southeast Asian tire manufacturers, with deliveries scheduled across 2024 and 2025, reflecting the geographic expansion of Chinese mold suppliers beyond their domestic base.

Q3 2024: MK Technology Corp. launched a new generation of laser-engraved sipe blade integration systems capable of achieving positional accuracy of ±0.05 mm, setting a new benchmark for premium passenger car tire mold specifications.

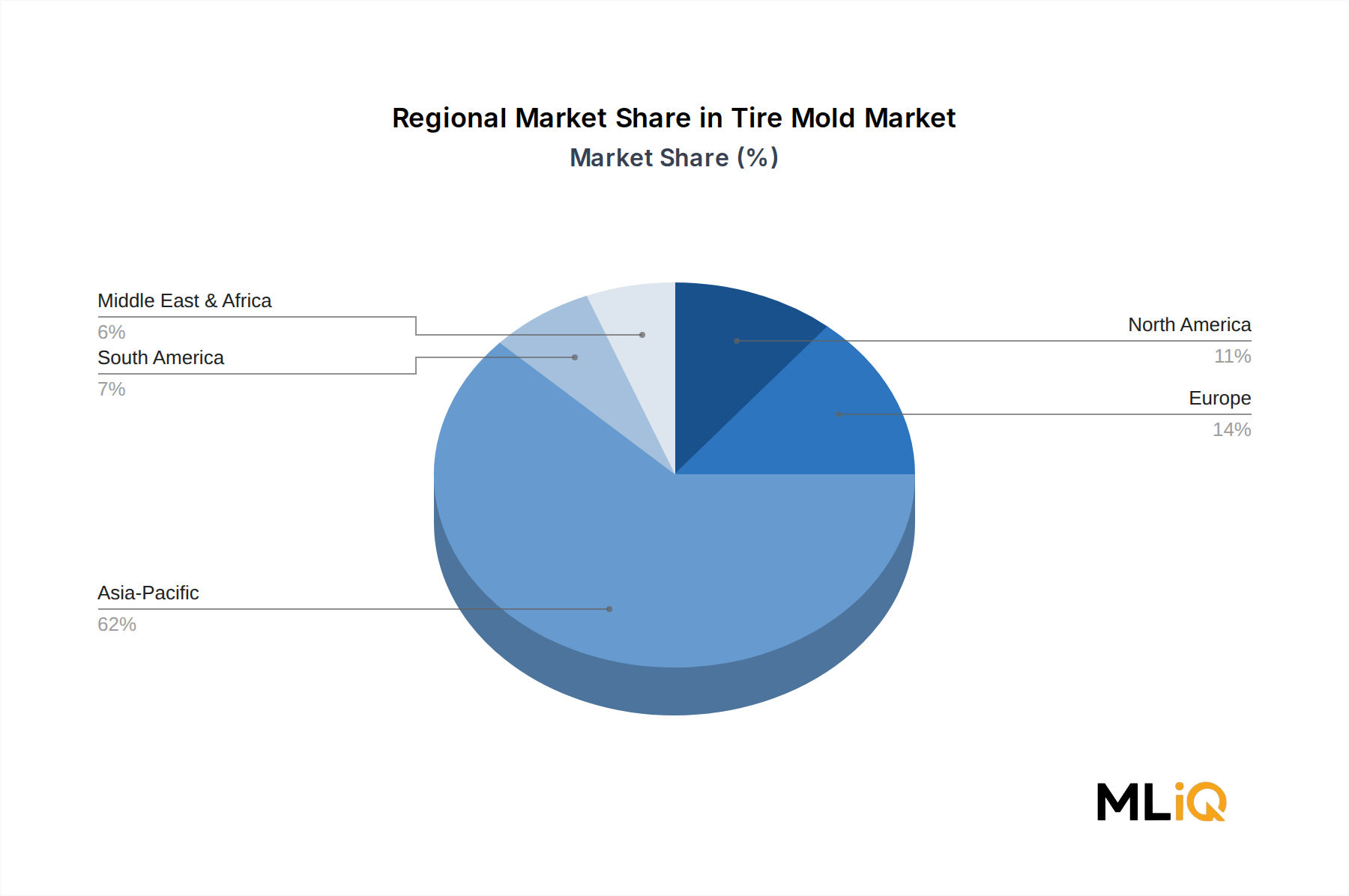

The tire mold market exhibits pronounced regional concentration, with Asia Pacific dominating both production and consumption while North America and Europe represent high-value mature segments.

Asia Pacific leads the global tire mold market with an estimated revenue share of 58% to 62% in 2024, underpinned by China's position as the world's largest tire manufacturing hub. China alone hosts over 400 tire manufacturers, generating substantial recurring mold procurement demand. The region is projected to grow at a CAGR of 6.1% through 2033, driven by India's accelerating vehicle production, ASEAN greenfield tire plant investments, and South Korea's and Japan's sustained demand for high-precision molds from premium tire OEMs. India's tire market is among the fastest-growing sub-regional markets, supported by government-backed automotive production incentives and rising two-wheeler and commercial vehicle sales.

North America accounts for approximately 14% to 16% of global tire mold market revenue, with the United States anchoring demand through its large domestic tire manufacturing base and reshoring initiatives that are bringing new tire plant investments to states such as Tennessee, South Carolina, and Georgia. The region grows at a CAGR of approximately 4.3%, with EV-specific tire mold upgrades representing the primary incremental demand vector. Mexico contributes modestly but is gaining relevance as automotive supply chains regionalize under USMCA frameworks.

Europe represents roughly 16% to 18% of global market revenue, characterized by high unit values rather than volume. German, French, and Italian tire manufacturers source premium molds domestically or from specialized European suppliers, prioritizing dimensional precision and surface quality over cost. Regional CAGR is estimated at 4.0% to 4.5%, with growth moderated by mature vehicle production volumes but supported by EV tire design transitions and sustainability-driven tread compound changes requiring updated tooling.

Middle East & Africa and South America collectively account for the remaining 6% to 8% of market revenue but represent above-average growth trajectories. South America's CAGR is estimated at 5.5%, driven by Brazil's recovering automotive sector and Argentina's commercial vehicle production. The Middle East & Africa region is an emerging growth pocket, supported by construction and mining activity driving OTR tire demand, though market infrastructure for local mold sourcing remains underdeveloped, creating import dependency.

Investment activity in the tire mold market has intensified over the 2022–2024 period, reflecting both organic capacity expansion by incumbent manufacturers and strategic consolidation as tire OEMs seek to secure supply chain resilience for tooling critical to production continuity.

The most significant capital flows have concentrated in the intelligent mold and digitally integrated tooling sub-segment. Greatoo Intelligent Equipment Inc. and Himile Mechanical Science & Technology have each disclosed capital expenditure programs exceeding $30 million across 2022 to 2024 for CNC infrastructure upgrades, robotic assembly lines, and R&D facilities targeting smart mold technology development. These investments signal a strategic pivot from commodity mold supply toward value-added intelligent tooling solutions that justify premium pricing.

M&A activity has been moderate but strategically significant. Several Chinese mold manufacturers have acquired smaller regional competitors to consolidate capacity and absorb specialized technical talent, particularly in EDM and laser engraving operations. European players have maintained independence but pursued joint development agreements with tire manufacturers to co-invest in proprietary mold technologies aligned with EV and sustainable tire roadmaps.

Venture and private equity interest has emerged in adjacent digital manufacturing platforms that serve tire mold producers, including mold lifecycle management software, AI-driven defect detection systems for mold inspection, and digital twin simulation tools for mold design validation. These technology layers are attracting funding from industrial automation investors recognizing the recurring software revenue potential layered atop the traditional capital equipment business model.

The sub-segment attracting the most strategic capital is EV-compatible segmented mold tooling, where design complexity and material requirements justify development investments that smaller players cannot absorb, creating a structural barrier that favors well-capitalized incumbents. The Tire Manufacturing Equipment Market and Rubber Molding Market are closely tracked by investors as proxy indicators for mold procurement cycles, given their direct upstream and downstream linkages to mold demand.

Technological innovation in the tire mold market is advancing along three primary vectors: intelligent mold systems, advanced materials, and

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.2% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Tire Mold Market market expansion.

Key companies in the market include QINGDAO YUANTONG MACHINERY CO., LTD., HERBERT MASCHINEN- UND ANLAGENBAU GMBH & CO. KG, A-Z GMBH, ANHUI WIDE WAY MOULD CO., LTD., ANHUI MCGILLMOULD CO., LTD., GREATOO INTELLIGENT EQUIPMENT INC., MK TECHNOLOGY CORP., KING MACHINE, SHINKO MOLD INDUSTRIAL CO., LTD., HIMILE MECHANICAL SCIENCE & TECHNOLOGY (SHANDONG) CO., LTD..

The market segments include Product Type, APPLICATION, TRUCK BUS RADIAL TIRES, OFF-THE-ROAD TIRES.

The market size is estimated to be USD 1.2 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3690, USD 5820, and USD 9870 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Tire Mold Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Tire Mold Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.