Dominance of Automatic Non-Woven Fabric Making Machines in the Non-Woven Fabric Making Machine Market

Within the Non-Woven Fabric Making Machine Market, the automatic segment has established itself as the unambiguous revenue leader, commanding the largest share of global machine sales by value. This dominance is not incidental — it is the product of structural forces reshaping manufacturing economics worldwide, and it shows every sign of consolidating further over the forecast period.

Automatic non-woven fabric making machines offer a compelling value proposition relative to their semi-automatic counterparts: substantially higher production throughput, lower per-unit labor costs, superior fabric consistency, and compatibility with digital process control systems. As end-user industries — particularly healthcare and hygiene — impose increasingly stringent quality and traceability requirements, the precision and repeatability offered by fully automated platforms become non-negotiable. A single high-speed automatic spunbond line, for example, can produce output volumes that would require multiple semi-automatic installations to match, fundamentally altering the cost-per-meter calculus.

The healthcare sector's outsized influence on this segment cannot be overstated. The global surge in demand for surgical masks, gowns, drapes, wound care products, and adult incontinence items — all of which rely on precision-manufactured non-woven substrates — has driven procurement officers toward high-capacity automatic systems. Regulatory compliance frameworks in the United States (FDA), Europe (CE/MDR), and increasingly across Asia Pacific jurisdictions further mandate production environments where process documentation and consistency are machine-enforced rather than operator-dependent.

In the automotive end-use segment, which is among the fastest-growing application verticals for non-wovens, automatic machines producing needle-punched and spunlaid materials for headliners, trunk liners, underbody shields, and cabin air filtration components are preferred for their ability to maintain dimensional tolerances at high line speeds. Major Tier 1 automotive suppliers globally have been expanding their in-house non-woven production capabilities, directly benefiting automatic machine suppliers.

From a competitive standpoint, leading machine manufacturers including KP Tech Machine (India) Pvt. Ltd., Dong Yang AoLong Nonwoven Equipment Co., Ltd., and Wenzhou Allwell Machinery Share Co., Ltd are all investing their primary R&D budgets in the automatic segment. Product roadmaps emphasize energy efficiency, servo-driven mechanical systems, touchscreen HMI interfaces, and IoT-enabled remote monitoring — features that are feasible only within fully automated machine architectures.

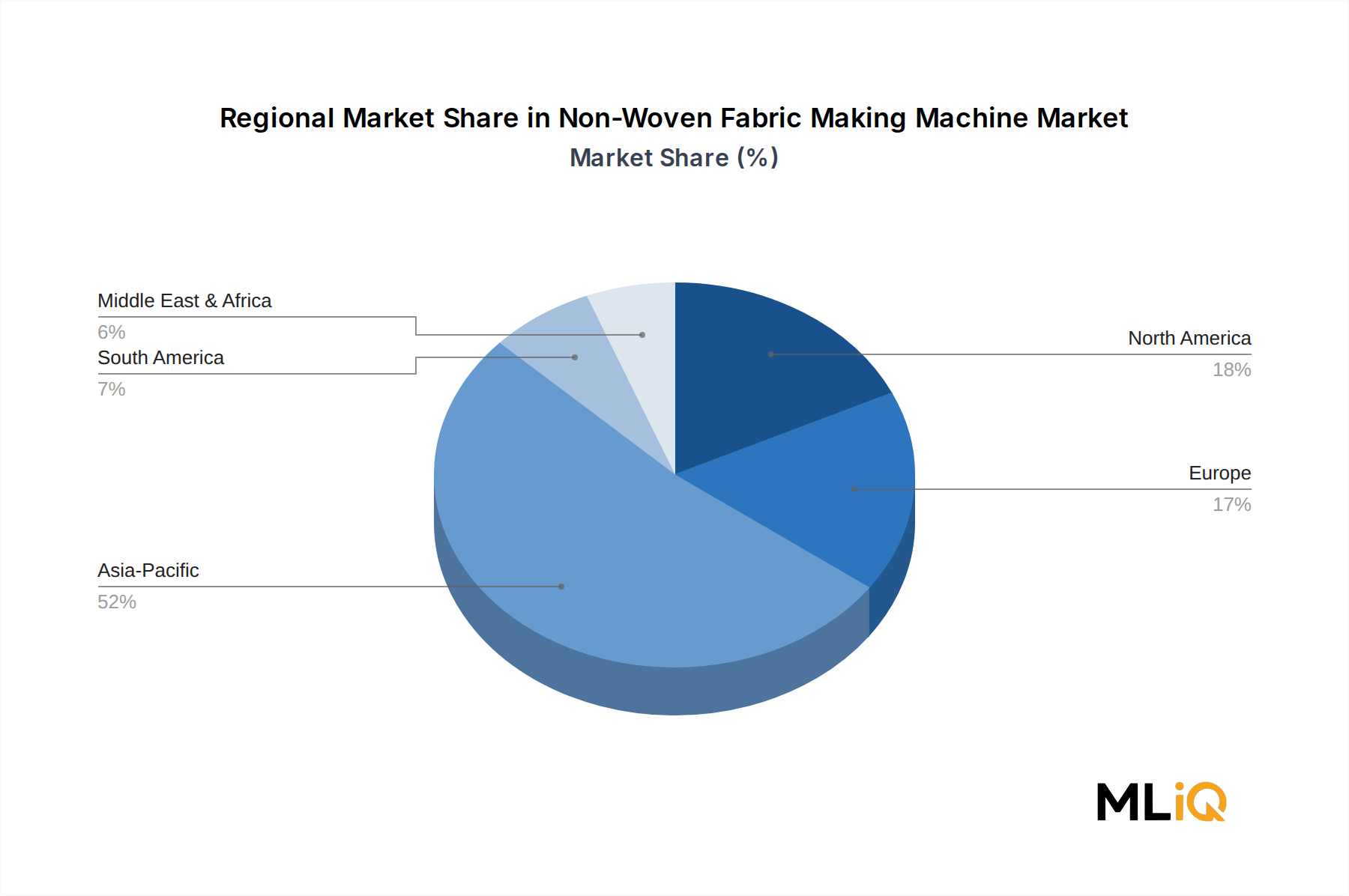

Geographically, the automatic segment's dominance is most pronounced in China, Germany, and the United States, where industrial scale, capital availability, and export orientation all favor high-throughput automated installations. In contrast, semi-automatic machines retain a meaningful market position in price-sensitive developing markets — particularly in sub-Saharan Africa, South Asia, and parts of Southeast Asia — where lower capital expenditure thresholds and simpler operating requirements remain important selection criteria.

Nevertheless, even in these developing markets, the trajectory is unmistakably toward automation. Government-backed industrialization programs, foreign direct investment inflows, and technology transfer agreements are progressively introducing automatic machine capabilities into markets previously dominated by semi-automatic configurations. The automatic segment's revenue share is therefore expected to widen meaningfully over the forecast period, reinforcing its structural leadership position within the broader Non-Woven Fabric Making Machine Market.