Vibrating Feeder Dominance in the Automatic Feeding Machine Market

Among the five primary feeding mechanism types — vibrating feeders, rotating wheel feeders, linear belt feeders, hopper systems, and tube feeders — the vibrating feeder segment commands the largest revenue share within the Automatic Feeding Machine Market. This dominance is attributable to a convergence of mechanical versatility, operational reliability, and favorable economics that collectively make vibrating feeders the default specification choice across the widest range of animal husbandry environments.

Vibrating feeders operate on the principle of controlled oscillation, using electromagnetic or electromechanical drive units to propel granular or pelletized feed materials along a trough or pan at precisely calibrated rates. This mechanism is inherently well-suited to the physical characteristics of most commercial animal feeds — which are particulate, moisture-sensitive, and subject to bridging in gravity-fed systems — making vibrating feeders mechanically superior to rotating or belt alternatives in many deployment contexts.

From a market share perspective, the vibrating feeder segment benefits from its established manufacturing base. Major producers have refined trough geometries, drive frequencies, and amplitude control systems over decades, yielding products with mean time between failure (MTBF) figures exceeding 20,000 operating hours in field conditions. This reliability profile is particularly valued by large-scale poultry integrators and swine confinement operators, where unplanned downtime directly translates to feed interruption events with measurable welfare and production yield consequences.

Key players active within this segment include global materials handling specialists such as Schenck Process, Eriez Manufacturing, and General Kinematics, alongside dedicated agri-tech manufacturers who have adapted industrial vibrating feeder architectures for livestock applications. These companies are increasingly differentiating on the basis of smart control integration — embedding variable-frequency drives, load cell feedback loops, and wireless connectivity into legacy feeder platforms.

The segment's revenue share is not merely stable but is consolidating further. Capital expenditure cycles in large-scale poultry and swine operations — which collectively represent the majority of end-use demand — have historically favored vibrating feeder procurement due to their lower maintenance cost per kilogram of feed dispensed relative to belt and tube alternatives. As farm scale increases through consolidation in North America and Europe, the per-unit economics of vibrating feeders improve, reinforcing their procurement preference.

Nevertheless, the segment faces incremental competition from hopper-integrated systems that combine gravity dispensing with vibration-assisted flow control, effectively capturing some of the volume advantage associated with standalone vibrating feeders. Manufacturers are responding by offering modular configurations that allow hopper attachments to be factory-integrated with vibrating trough assemblies, preserving segment boundaries while expanding addressable application scope.

Sustainability considerations are also shaping segment dynamics. The latest generation of electromagnetic vibrating feeders consumes 30–40% less electrical energy than older mechanical eccentric-drive designs, positioning them favorably against tightening energy efficiency regulations in the European Union and aligning with corporate sustainability commitments among multinational protein producers. This energy efficiency narrative is becoming a primary commercial argument in the sales cycle, particularly for facilities subject to carbon accounting requirements.

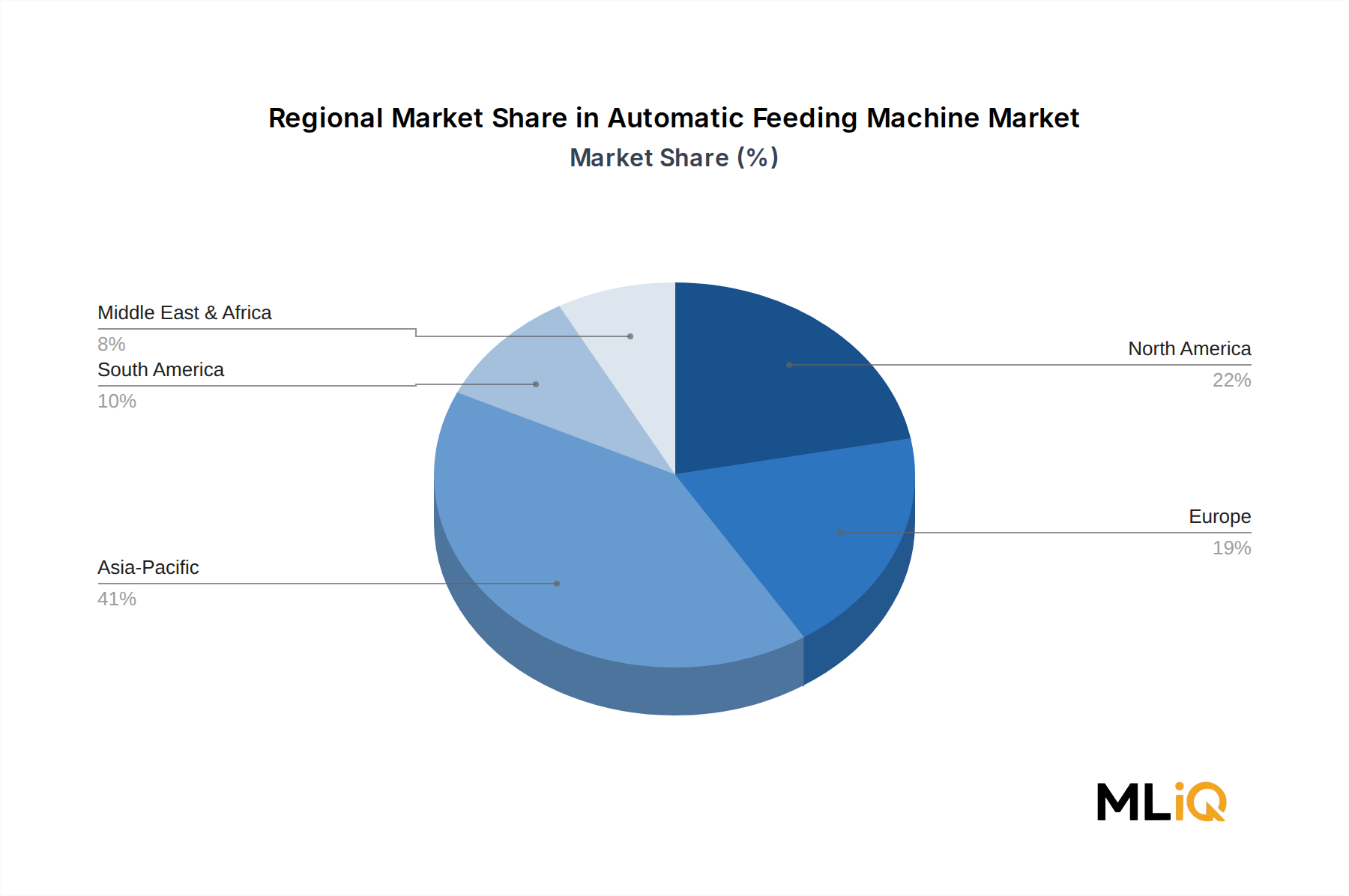

In terms of geographic concentration, the vibrating feeder sub-segment mirrors the broader market's regional distribution, with Asia Pacific accounting for the largest share of unit volume driven by China's massive swine sector, while North America and Europe lead in per-unit value terms due to higher automation specification levels and integration of advanced sensor packages.