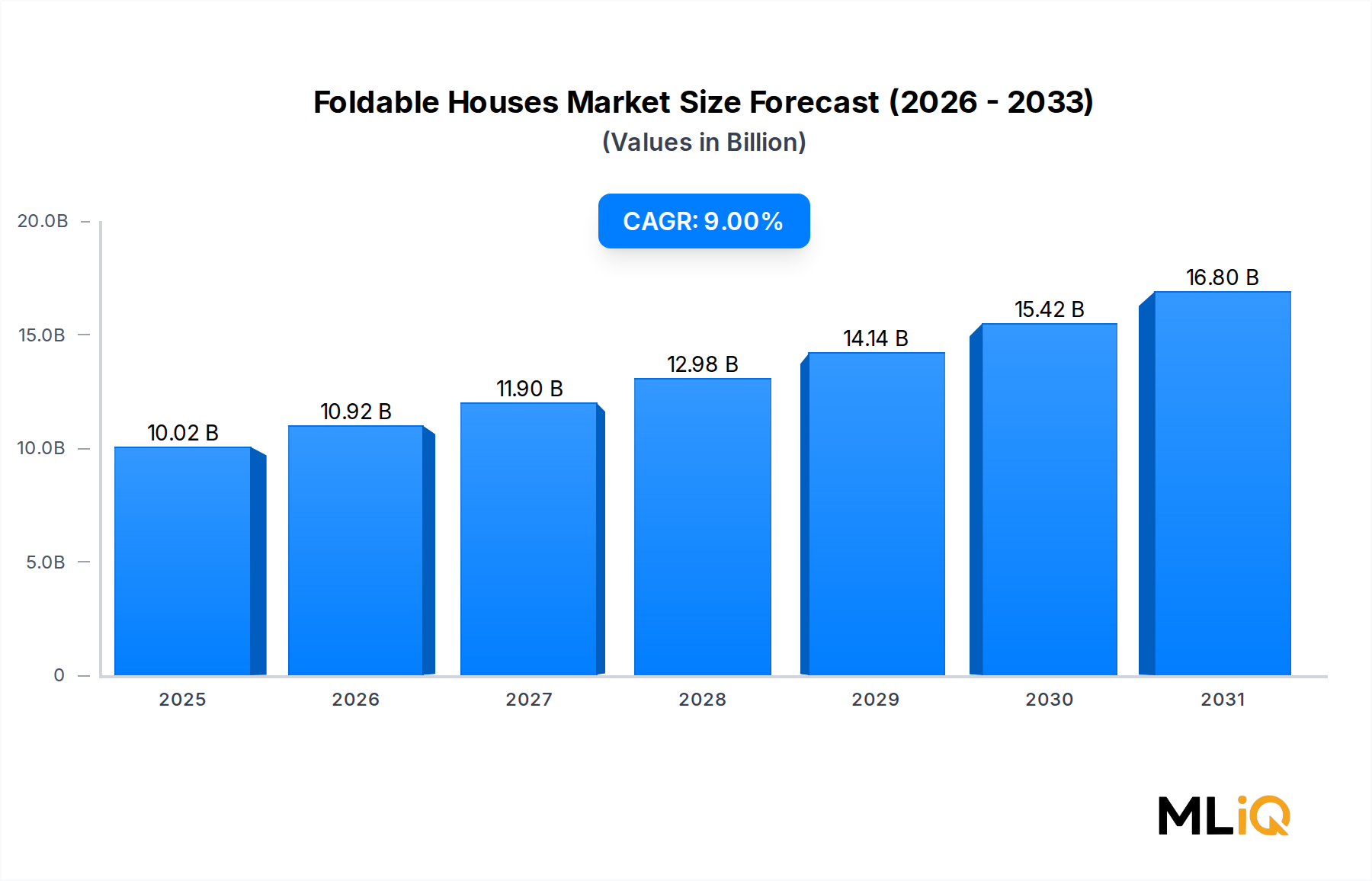

Single-Section Construction Type Dominance in the Foldable Houses Market

Within the Foldable Houses Market, segmentation by construction type reveals a clear market leader: the single-section format. Single-section foldable houses — units delivered and deployed as a singular, self-contained folded module — command the majority revenue share and continue to consolidate their position relative to multi-section alternatives. Understanding why this segment leads requires examining operational, logistical, and end-user behavioral dimensions simultaneously.

The primary driver of single-section dominance is deployment simplicity. A single-section unit requires no on-site module joining, reducing skilled labor requirements and installation time to a minimum. In contexts where labor scarcity is acute — such as post-disaster zones, remote resource-extraction sites, or rapidly urbanizing peri-urban corridors — this characteristic translates directly into procurement preference. Governments and NGOs executing emergency housing programs consistently favor single-section units precisely because their speed-to-occupancy can be measured in hours rather than days.

From a manufacturing economics standpoint, single-section designs benefit from higher production line throughput. Factory floor configurations optimized for a standardized folding geometry allow batch-production efficiencies that multi-section units, requiring more complex sub-assembly coordination, cannot replicate. This cost advantage cascades through to end-user pricing, enabling single-section foldable homes to compete more aggressively with traditional manufactured housing in the sub-$50,000 retail price bracket.

Key companies operating with particular intensity in the single-section segment include Boxabl Inc., whose Casita product is engineered around a single-module fold-out concept targeting the U.S. and European markets, and A-FOLD Houses, which specializes in rapid-deploy single units for both residential and commercial transitional applications. Guangzhou Moneybox Steel Structure Engineering Co., Ltd and Hebei Weizhengheng Modular House Technology Co., Ltd. leverage China's integrated steel supply chains to produce high-volume single-section units for export markets across Southeast Asia, Africa, and the Middle East.

In terms of architectural configuration, single-section foldable homes are available in both slope roof and flat roof variants, though flat roof configurations are disproportionately common in the single-section segment due to their lower mechanical complexity during the fold-out sequence. Slope roof single-section units, while aesthetically superior for permanent residential applications, involve more elaborate hinge engineering and are therefore priced at a premium.

The end-user composition for single-section units skews heavily toward single-family occupancy, consistent with the units' typical floor area range of 25–80 square meters. This positions them squarely within the affordable starter-home and workforce housing categories that are experiencing the strongest governmental and institutional tailwinds globally.

Looking at share trajectory, single-section units are not merely dominant today — they are consolidating further. As manufacturing scale increases and unit economics improve, the price gap between single and multi-section configurations is widening in favor of single-section, reinforcing purchaser preference. The segment is expected to maintain a revenue share premium throughout the 2025–2033 forecast window, particularly as disaster-relief and workforce housing procurement programs scale globally.

Multi-section foldable homes, by contrast, are carving a distinct niche in permanent residential and multi-family applications where greater floor area and architectural customization justify the additional logistical complexity. This bifurcation is creating a structurally healthy dual-track market where the two construction types serve genuinely differentiated demand pools rather than competing head-to-head.