The Polyamides Industry Market is propelled by a convergence of structural demand drivers and tempered by a distinct set of supply-side and macroeconomic constraints. A rigorous, data-anchored analysis of these forces is essential for accurate market navigation.

Demand from the automotive sector, which accounts for an estimated 30–35% of total polyamide consumption globally, is being amplified by vehicle electrification. The International Energy Agency reported that global BEV sales exceeded 10 million units in 2022 and continued to grow sharply thereafter, with each BEV platform incorporating approximately 15–25% more high-performance thermoplastic content than a comparable internal combustion engine vehicle. This structural uplift directly benefits the Polyamides Industry Market.

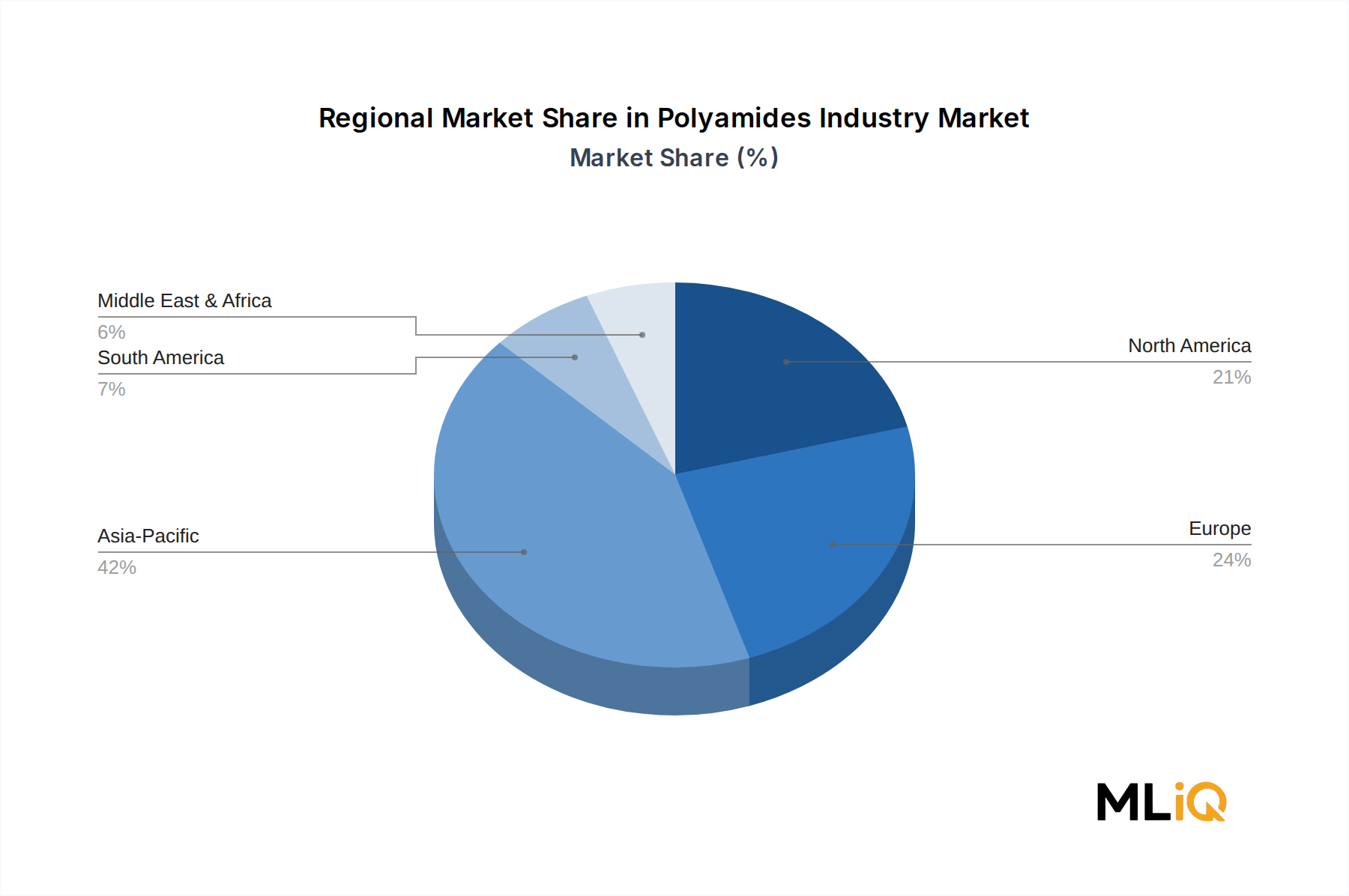

Electrical and electronics applications represent the second-largest demand engine. The rollout of 5G infrastructure globally, combined with the proliferation of data centers and industrial IoT devices, is driving demand for flame-retardant PA46 and polyphthalamide grades used in connectors, sockets, circuit breakers, and relay housings. Asia Pacific's electronics manufacturing ecosystem, concentrated in China, South Korea, Japan, and ASEAN nations, is the primary volume absorber of these grades.

On the sustainability and regulatory driver front, the European Union's End-of-Life Vehicle Directive and upcoming Eco-design Regulation are compelling automotive OEMs to incorporate measurable percentages of recycled or bio-based polymer content, creating a pull effect for products like LANXESS's Durethan ECO, which integrates recycled glass fiber into its PA6 matrix.

Constraints include raw material price volatility, specifically for caprolactam (the primary monomer for PA6) and hexamethylenediamine/adipic acid (for PA66), which are petrochemical derivatives subject to crude oil and benzene price cycles. Supply chain disruptions in 2021–2022 exposed the vulnerability of just-in-time polyamide supply chains, prompting buyers to seek dual-sourcing strategies and producers to invest in backward integration.

Additionally, intensifying competition from alternative engineering polymers, including polyphenylene sulfide (PPS), polyetherimide (PEI), and liquid crystal polymers (LCP), exerts substitution pressure on polyamides in the highest-temperature automotive and electronics applications.