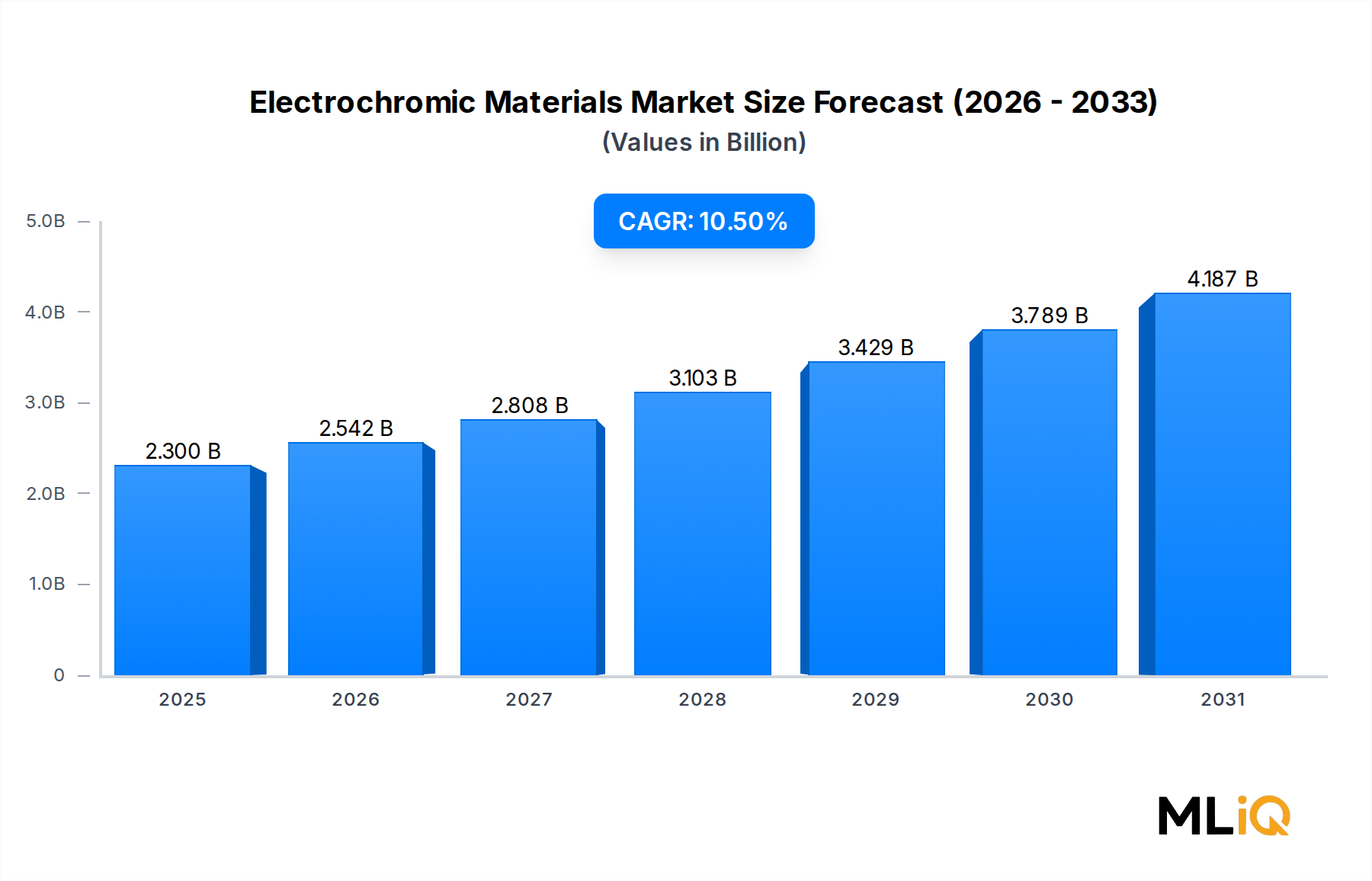

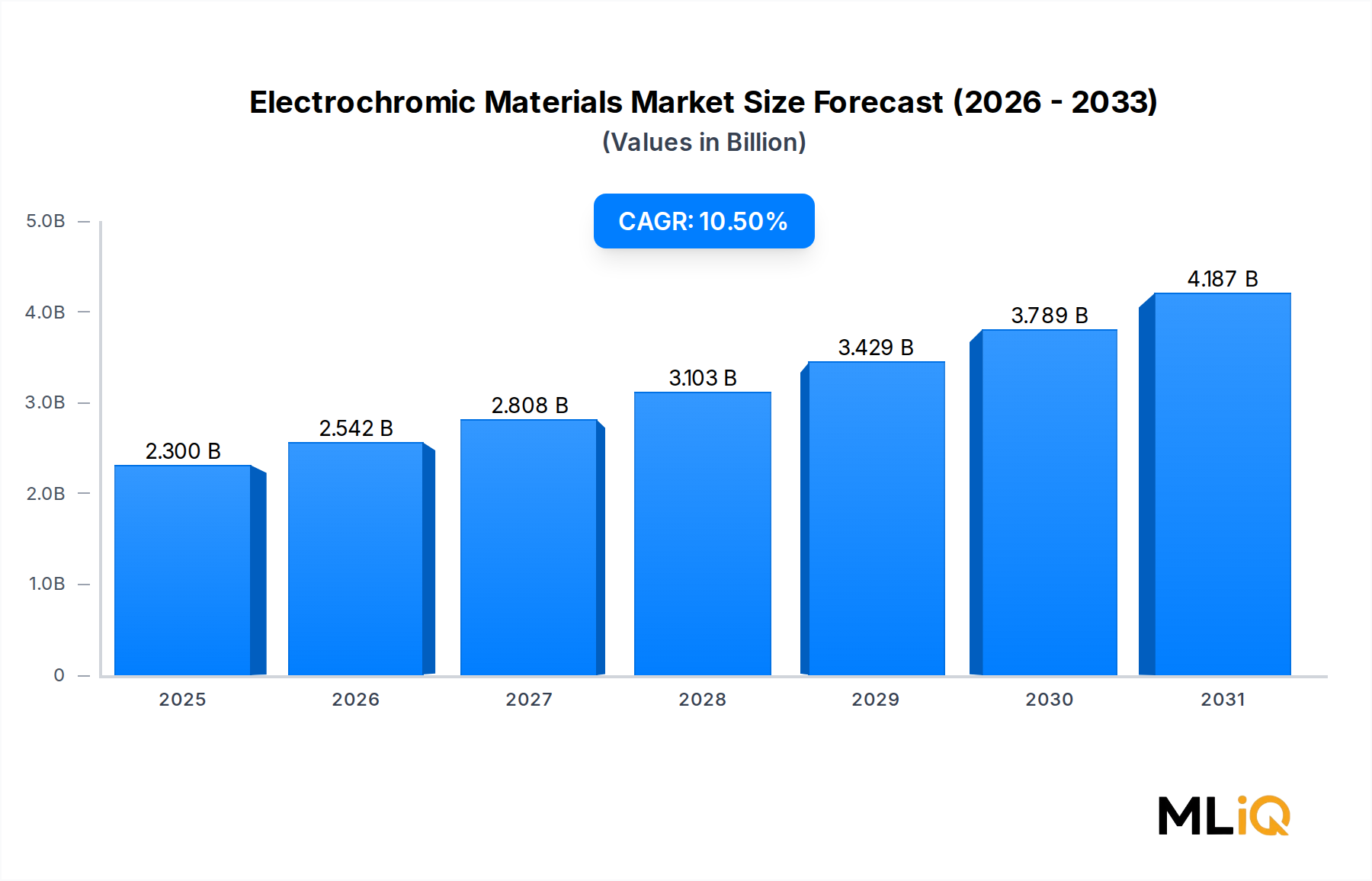

The global Electrochromic Materials Market is valued at $2.3 billion in 2025, reflecting a robust expansion trajectory underpinned by accelerating demand from architecture, automotive, aerospace, and consumer electronics sectors. The market is projected to grow at a compound annual growth rate (CAGR) of 10.5% through the forecast period, driven by the convergence of smart building regulations, electrification of transportation, and rising defense budgets—particularly from the United States government.

Electrochromic materials are substances that reversibly change their optical properties—transmittance, reflectance, or absorbance—when subjected to an applied voltage. This functional characteristic positions them as foundational enablers of dynamic glazing, adaptive optics, and energy-efficient architectural envelopes. As global building codes increasingly mandate lower energy consumption per square meter, electrochromic glass and coatings have transitioned from premium novelties to near-mainstream specification items in commercial construction.

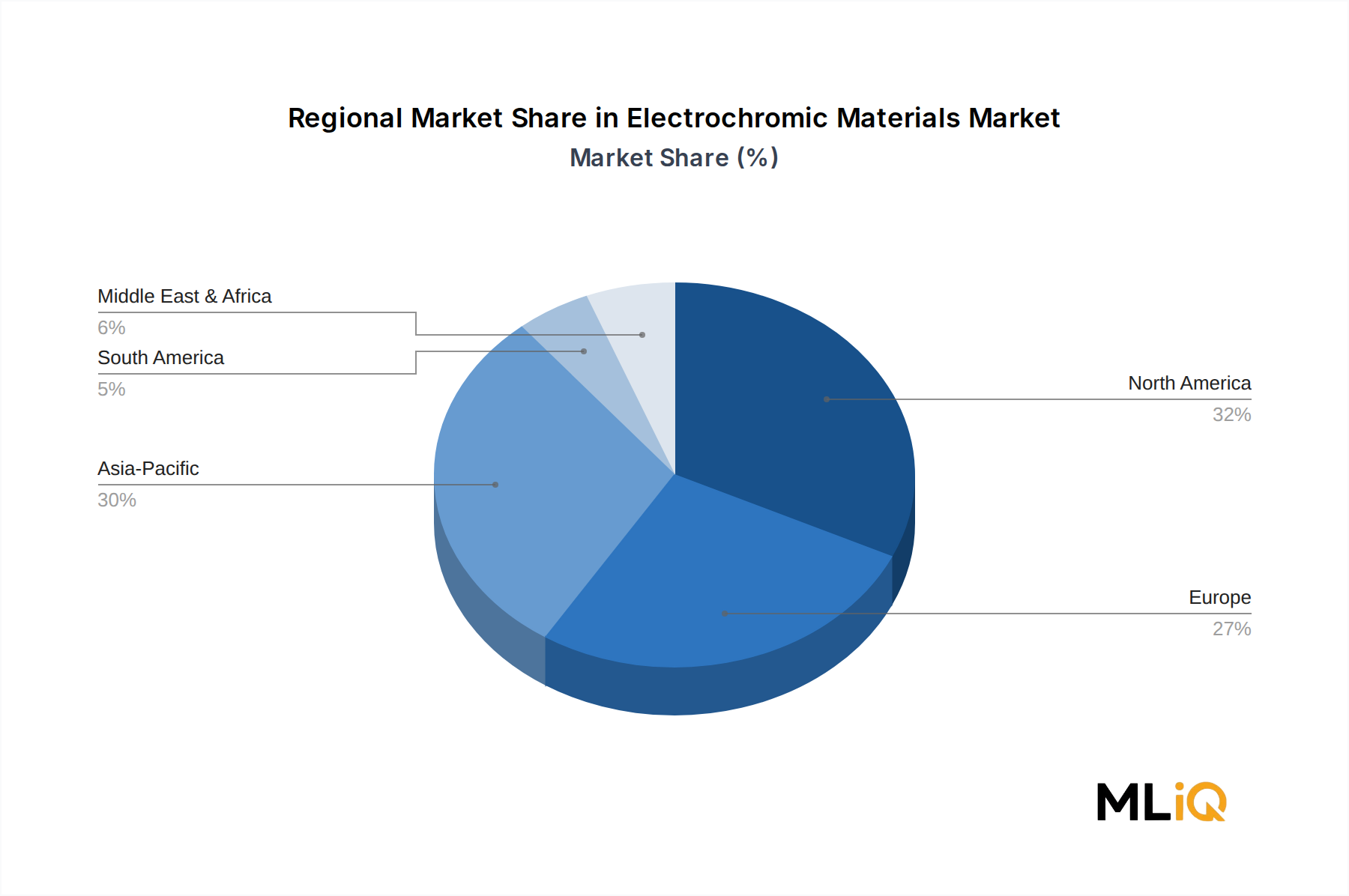

A critical macro tailwind is the intensifying focus on green building certification systems such as LEED, BREEAM, and WELL. Buildings that deploy electrochromic window systems can reduce HVAC loads by up to 30%, a figure that resonates strongly with institutional real estate developers and corporate occupiers managing net-zero commitments. This demand signal is particularly robust in North America and Western Europe, where carbon disclosure regulations are raising the cost of non-compliance.

On the consumer electronics front, wearable devices, smart eyewear, and display technologies have begun integrating thin-film electrochromic layers to achieve privacy filtering, glare reduction, and ambient light adjustment. The miniaturization of electrochromic devices and the development of flexible polymer substrates are unlocking entirely new application vectors, including foldable displays and adaptive lens systems.

In the automotive sector, the penetration of electrochromic rear-view mirrors—which now appear in mid-range as well as luxury vehicles—has established a durable, high-volume revenue stream for market participants. Auto-dimming mirror adoption rates in passenger vehicles have surpassed 40% in North American and European OEM platforms as of 2024, signaling that this sub-segment has crossed the commercialization threshold and is now scaling rapidly.

The aerospace and defense vertical represents a higher-margin, lower-volume opportunity. Government procurement programs in the United States, France, and the United Kingdom are incorporating electrochromic canopy glazing and adaptive cockpit visors into next-generation aircraft platforms, providing long-duration contracts with high barriers to competitive displacement.

Looking forward, the market's trajectory will be shaped by the cost reduction curves of vacuum deposition and sol-gel processing, the availability of critical raw materials such as tungsten trioxide and iridium oxide, and the pace of regulatory mandates requiring dynamic solar control in commercial buildings. Analysts expect the market to surpass $6.0 billion by the end of the decade, with Asia Pacific emerging as the fastest-growing region due to accelerating urbanization and expanding manufacturing capacity in China, South Korea, and India.