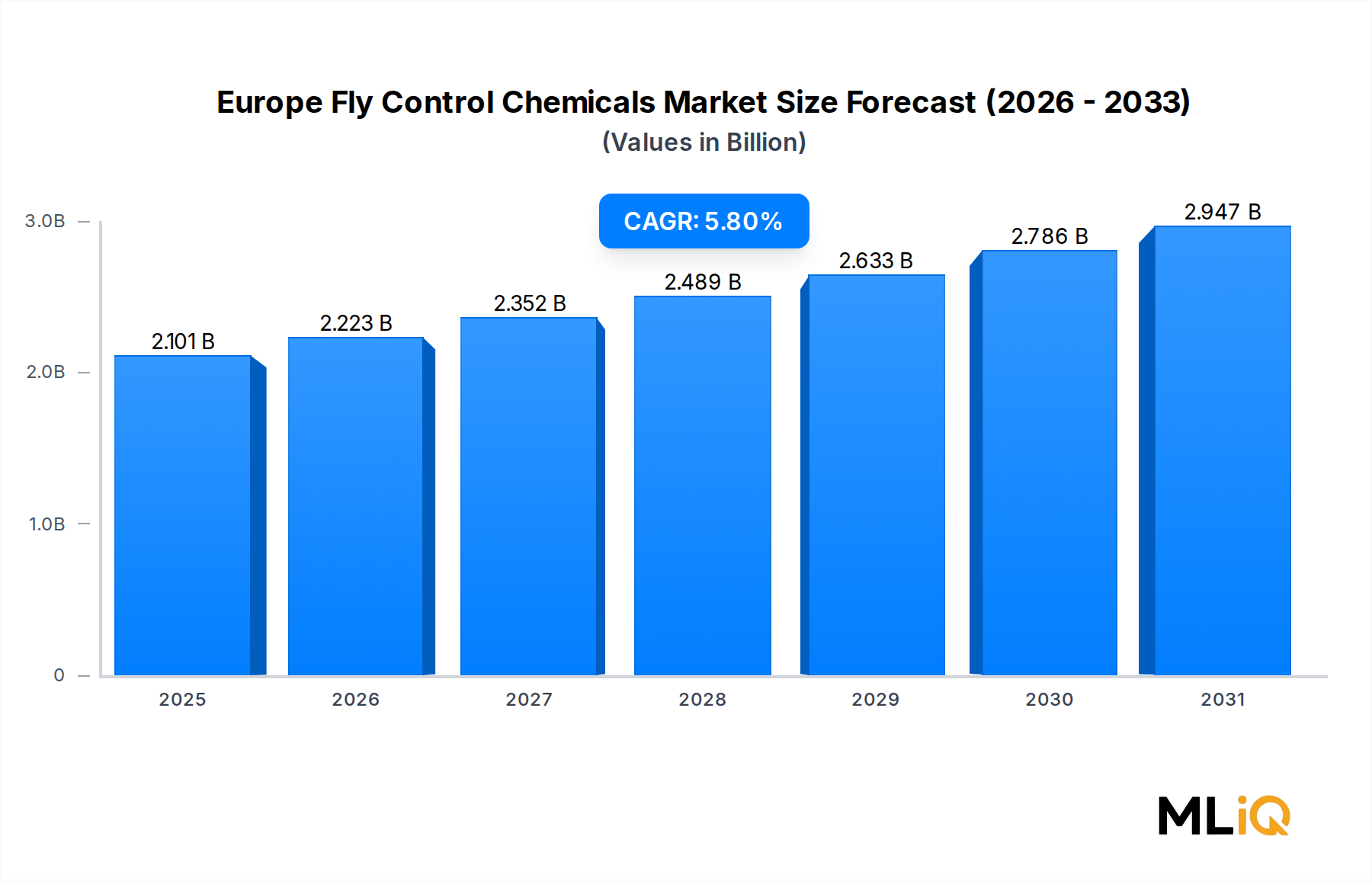

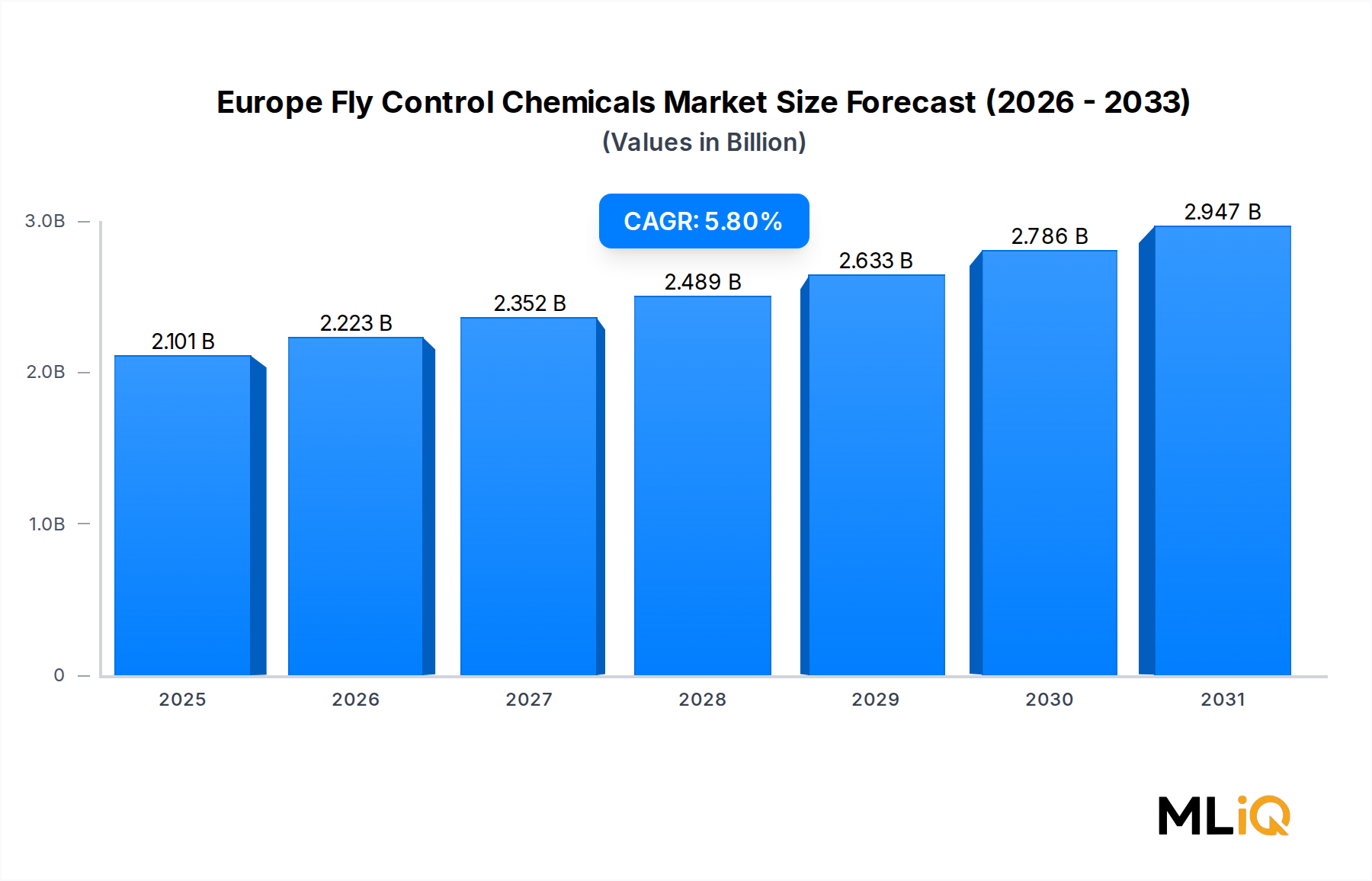

The Europe Fly Control Chemicals Market is valued at $2,101.48 million and is projected to expand at a compound annual growth rate of 5.8% through the forecast period of 2025 to 2033. This sustained growth trajectory is underpinned by intensifying public health mandates across European Union member states, growing awareness of vector-borne disease prevention, and elevated demand from agriculture, food processing, and waste management sectors. Fly control chemicals encompass a diverse portfolio of active ingredients and formulations—including larvicides, adulticides, organophosphorus compounds, pyrethroids, neonicotinoids, and insect growth regulators—deployed across residential, commercial, and industrial environments.

A critical macro tailwind is the tightening of European food safety and hygiene regulations, particularly those enforced by EFSA (European Food Safety Authority) and national veterinary agencies, which mandate stringent pest control protocols in food-handling facilities. The EU's Farm to Fork Strategy, a core element of the European Green Deal, simultaneously introduces pressure to reduce synthetic chemical dependency, driving parallel innovation in biological and integrated pest management formulations.

Demand from the waste treatment and municipal sanitation sectors represents a structurally growing end-use channel, as fly populations around mechanical biological treatment plants and anaerobic digestion facilities require systematic chemical suppression programs. Rising urbanization across Germany, France, the United Kingdom, and Benelux countries has enlarged the footprint of commercial and institutional pest control contracts, sustaining a robust pipeline of recurring chemical demand.

From an active ingredient perspective, organophosphorus compounds and pyrethroid-based formulations collectively account for the majority of market revenue, though insect growth regulators are capturing incremental share due to their targeted mode of action and lower ecotoxicological profiles. The neonicotinoid sub-segment faces regulatory headwinds under EU Regulation 1107/2009, creating market redistribution toward alternative chemistries.

On the supply side, the market benefits from a well-established European agrochemical manufacturing base, with notable production clusters in Germany, Switzerland, and the Netherlands. However, raw material import dependency—particularly for synthetic pyrethroids and certain organophosphate precursors sourced from Asia—introduces price volatility risks that manufacturers are addressing through dual-sourcing and forward contracting strategies.

Looking ahead to 2033, the market is anticipated to register strong absolute dollar gains, with digital pest monitoring integration, microencapsulation delivery technologies, and bio-rational chemistry acting as the primary innovation vectors reshaping competitive dynamics.