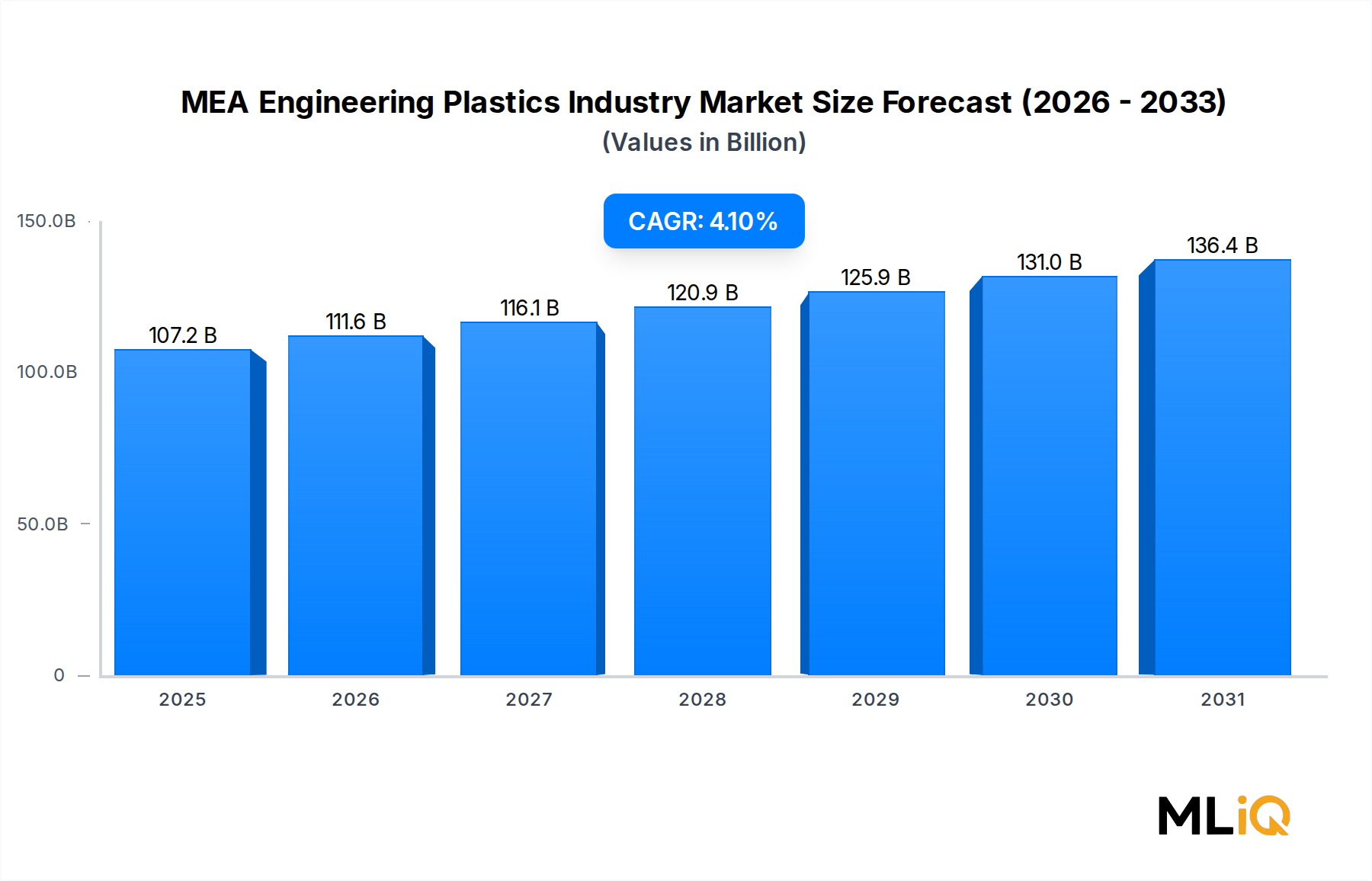

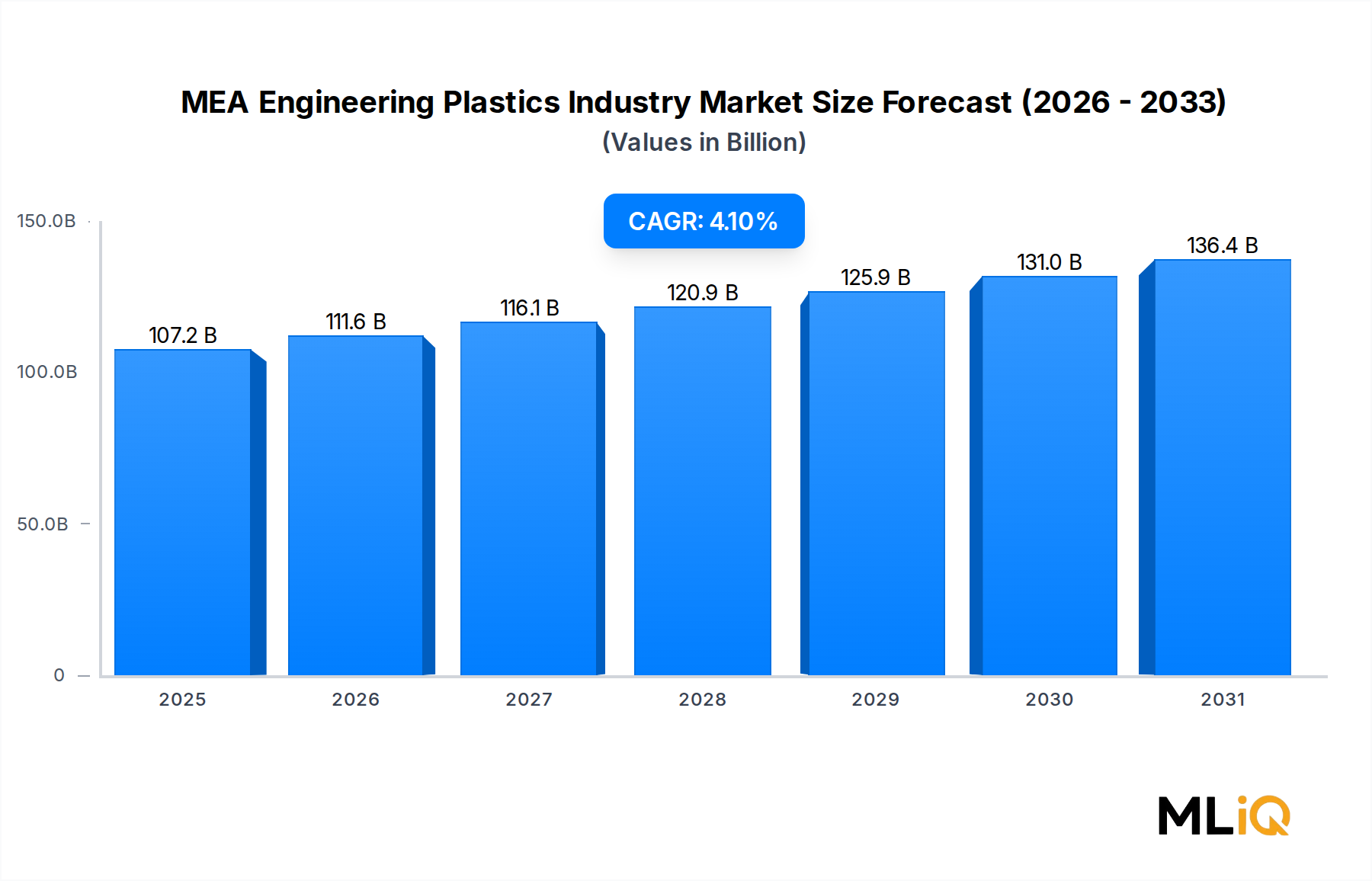

Der Markt für technische Kunststoffe in der MEA-Region (Naher Osten und Afrika) wird im Basisjahr 2025 auf 107,17 Milliarden USD (ca. 99,7 Milliarden €) geschätzt und soll im Prognosezeitraum mit einer durchschnittlichen jährlichen Wachstumsrate (CAGR) von 4,1% expandieren. Diese Entwicklung spiegelt ein Zusammentreffen von strukturellen Nachfrageverschiebungen, Industrialisierungsnotwendigkeiten im gesamten Nahen Osten und Afrika sowie die beschleunigte Substitution konventioneller Materialien wie Metalle, Glas und Keramik durch hochleistungsfähige polymere Alternativen wider.

Technische Kunststoffe nehmen aufgrund ihrer überlegenen mechanischen Festigkeit, thermischen Stabilität, chemischen Beständigkeit und ihres geringen Gewichts eine kritische Position in modernen industriellen Lieferketten ein. Diese Eigenschaften haben sie in der Automobil- und Transportindustrie, der Elektro- und Elektronikindustrie, dem Bauwesen, der Medizintechnik und dem Maschinenbau unverzichtbar gemacht – alles Sektoren, die in der MEA-Region eine rasche Kapazitätserweiterung erfahren.

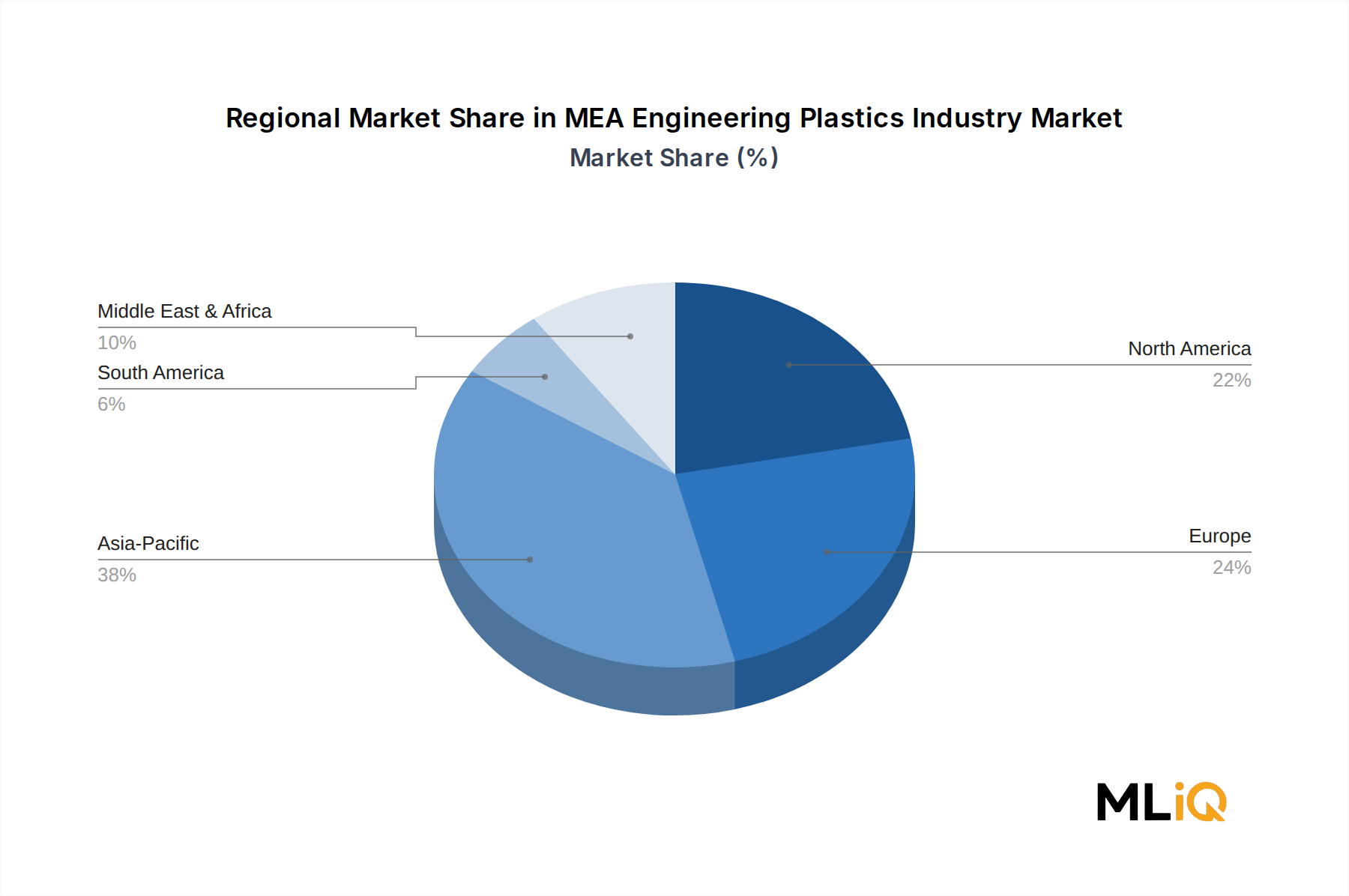

Das Marktwachstum wird durch die steigende Kaufkraft in den GCC-Wirtschaften, den nordafrikanischen Fertigungskorridoren und den industriellen Zentren in Subsahara-Afrika untermauert. Von der Regierung unterstützte Diversifizierungsprogramme – insbesondere Saudi Vision 2030, die Industriestrategie der VAE und die nationale Fertigungsagenda Ägyptens – lenken erhebliche Investitionen in nachgelagerte Verarbeitungsindustrien, die stark auf technische Kunststoffe angewiesen sind. Diese makroökonomischen Rückenwinde werden voraussichtlich die Nachfragedynamik bis weit in die zweite Hälfte des Jahrzehnts aufrechterhalten.

Fluorpolymere, Polycarbonate, Polyamide und PET-Harze bleiben die dominierenden Volumenlieferanten, während Spezialsorten wie PEEK und Flüssigkristallpolymere (LCP) in hochwertigen Endverbraucher-Nischen an Bedeutung gewinnen. Das Segment Elektro und Elektronik entwickelt sich zu einem besonders dynamischen Nachfragezentrum, angetrieben durch den Ausbau der 5G-Infrastruktur, Investitionen in intelligente Netze und die Erweiterung der Unterhaltungselektronikfertigung in der Türkei und Südafrika.

Auf der Angebotsseite vertiefen globale Akteure, darunter BASF SE, Covestro AG, SABIC, DuPont und Solvay, ihre regionale Präsenz durch Kapazitätsinvestitionen, Joint Ventures und Vertriebspartnerschaften, die auf die MEA-Marktspezifikationen zugeschnitten sind. Die native Positionierung von SABIC innerhalb des Golf-Kooperationsrates verschafft dem Unternehmen einen strukturellen Rohstoffvorteil, den globale Wettbewerber strategisch nutzen müssen.

Die Rohstoffpreisvolatilität – insbesondere bei Benzol-, Propylen- und Adipinsäurederivaten – stellt ein anhaltendes Margenrisiko dar. Die Produzenten setzen jedoch zunehmend auf langfristige Abnahmeverträge und Rückwärtsintegrationsstrategien, um sich von den Schwankungen der Rohstoffpreise abzuschirmen.

Mit Blick auf die Zukunft wird erwartet, dass der MEA-Markt für technische Kunststoffe von der Intensivierung der lokalen Automobilkomponentenfertigung, erhöhten Ausgaben für die Gesundheitsinfrastruktur und einer wachsenden Nachfrage im Verpackungssektor, die mit dem E-Commerce-Wachstum verbunden ist, profitieren wird. Die Widerstandsfähigkeit des Marktes und seine diversifizierte Endverbraucherbasis positionieren ihn für ein stetiges, sich verstärkendes Wachstum im Prognosezeitraum.