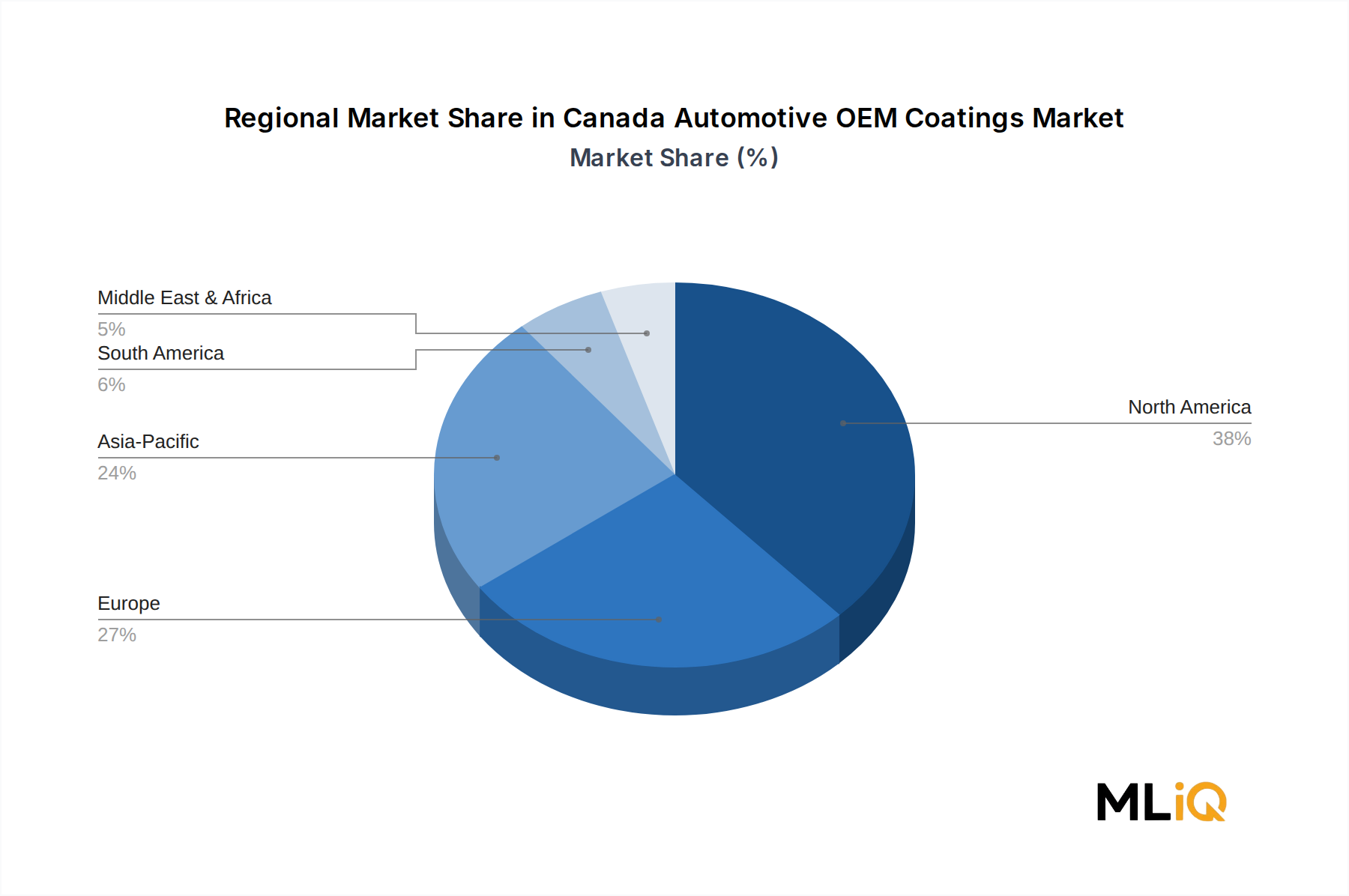

The Canada Automotive OEM Coatings Market exhibits pronounced geographic concentration, with demand patterns closely mirroring the distribution of automotive manufacturing activity across North America and globally.

North America (Dominant Region): Canada sits within the broader North American automotive manufacturing ecosystem, which collectively represents the most mature and highest-revenue region for OEM coatings. The United States commands the largest share of North American OEM coatings consumption, given its significantly larger vehicle production base. Canada's contribution is concentrated in Ontario — home to assembly plants operated by Stellantis, General Motors, Toyota, and Honda — and to a lesser extent Quebec and British Columbia. The North American region as a whole is characterized by high adoption of water-borne and low-VOC coating technologies, driven by EPA and Environment Canada regulatory frameworks. Regional CAGR for North America is estimated at approximately 3.8–4.2%, consistent with the Canadian market's reported growth rate.

Europe (Technology Leader): Europe remains the global benchmark for OEM coatings innovation, particularly in waterborne and powder coating technology. Germany, France, and the United Kingdom account for the majority of European OEM coatings demand. While European CAGR is somewhat constrained by flat vehicle production volumes — particularly in internal combustion engine (ICE) segments — the region's early adoption of EV platforms is generating demand for new coating system architectures. European CAGR is estimated at 3.5–4.0%.

Asia Pacific (Fastest-Growing Region): Asia Pacific, led by China, India, Japan, and South Korea, represents the fastest-growing regional market for automotive OEM coatings globally, with an estimated CAGR in the range of 5.5–6.5%. China's massive EV production ramp, India's expanding passenger car market, and Southeast Asia's growing commercial vehicle assembly base are the primary demand engines. The Industrial Coatings Market in Asia Pacific is expanding in parallel, reflecting broader manufacturing sector growth.

South America (Emerging Market): Brazil and Argentina anchor South American OEM coatings demand, supported by domestic vehicle production and export-oriented manufacturing. Regional CAGR is estimated at 3.0–3.5%, constrained by macroeconomic volatility and currency risk, though the long-term structural demand for coatings remains positive.

Middle East and Africa (Nascent but Developing): This region accounts for a relatively modest share of global OEM coatings consumption but is growing as localized vehicle assembly and aftermarket activity expands. Turkey and South Africa are the primary market anchors. Regional CAGR is estimated at 4.0–4.5%, driven by infrastructure investment and rising vehicle ownership rates.