1. What are the major growth drivers for the Organic Baby Food Market market?

Factors such as are projected to boost the Organic Baby Food Market market expansion.

Organic Baby Food Market

Organic Baby Food Market

Market Lens IQ is a global market intelligence and strategic consulting firm delivering advanced syndicated research reports, customized industry analysis, competitive intelligence, and data-driven advisory solutions to organizations across international markets. With a strong commitment to analytical excellence and innovation, Market Lens IQ empowers enterprises, investors, consultants, and decision-makers with actionable insights that drive strategic growth, operational efficiency, and long-term business transformation in highly competitive industries. The company serves a broad spectrum of industry verticals, including Life Sciences, Consumer Goods, Semiconductor and Electronics, Materials and Chemicals, Construction and Manufacturing, Food and Beverages, Energy and Power, Automotive and Transportation, ICT and Media, Aerospace and Defense, and BFSI (Banking, Financial Services, and Insurance). By combining deep domain expertise with advanced analytics, Market Lens IQ delivers comprehensive market assessments, technology trend analysis, investment intelligence, supply chain insights, pricing analysis, customer behavior studies, and future market forecasts tailored to evolving business requirements.

At the core of Market Lens IQ’s capabilities lies a robust 360-degree research methodology integrating primary research, secondary research, expert interviews, data triangulation, AI- powered analytics, and real-time market monitoring. Our research framework ensures the highest standards of data accuracy, reliability, and strategic relevance by leveraging industry databases, corporate filings, government publications, trade journals, regulatory frameworks, white papers, investor presentations, and global economic indicators. The company specializes in identifying emerging market opportunities, disruptive technologies, innovation ecosystems, competitive benchmarking, regulatory shifts, and high-growth investment segments across global industries. Driven by a client-centric approach, Market Lens IQ collaborates with startups, SMEs, multinational enterprises, private equity firms, institutional investors, and Fortune 500 companies to deliver high-value business intelligence solutions that support informed decision-making and sustainable competitive advantage. Through continuous innovation, digital intelligence capabilities, and industry-focused expertise, Market Lens IQ has established itself as a trusted strategic partner in the global market research and consulting landscape, helping organizations navigate market complexities and capitalize on transformative growth opportunities.

+1 2315155523

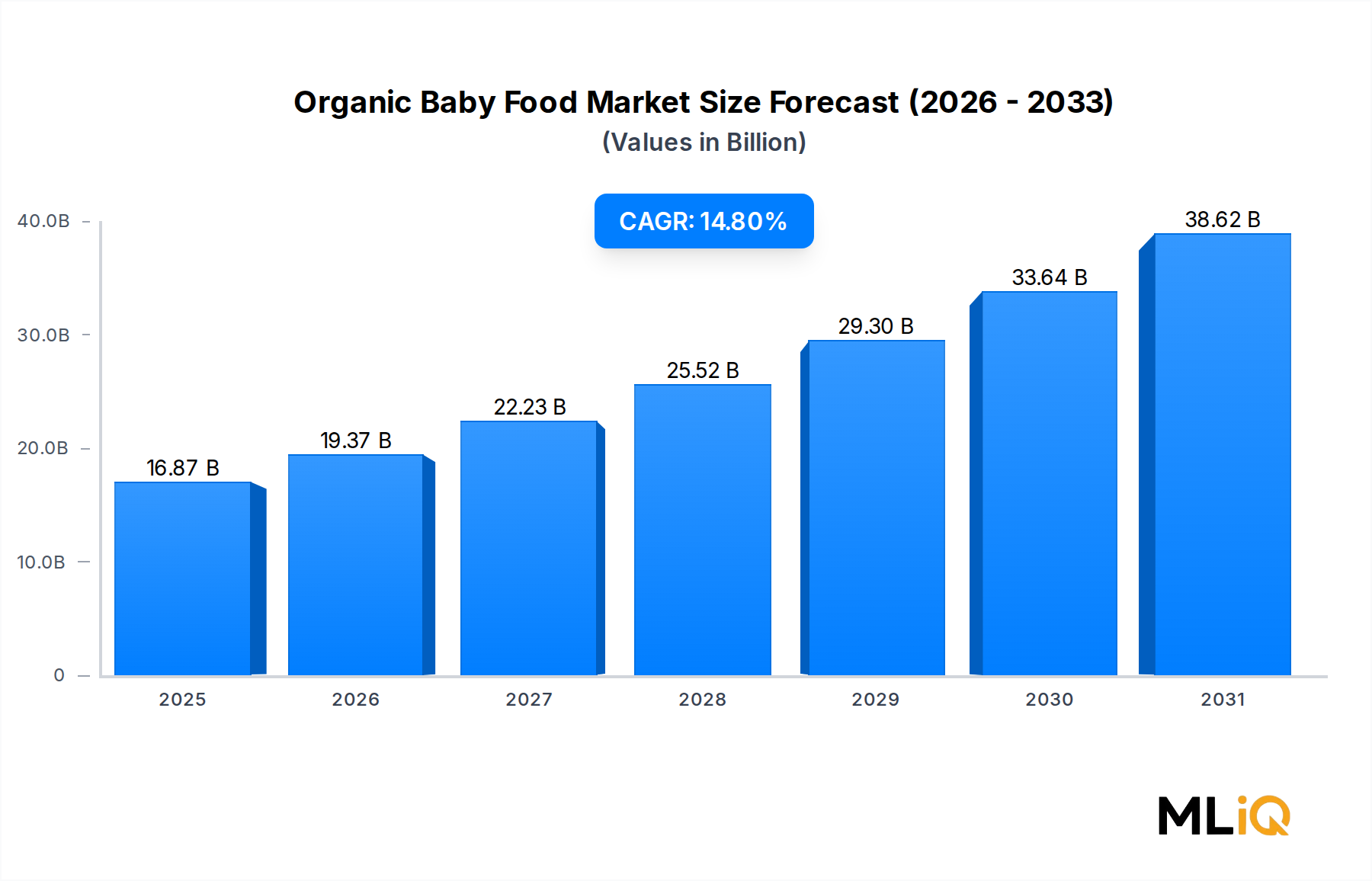

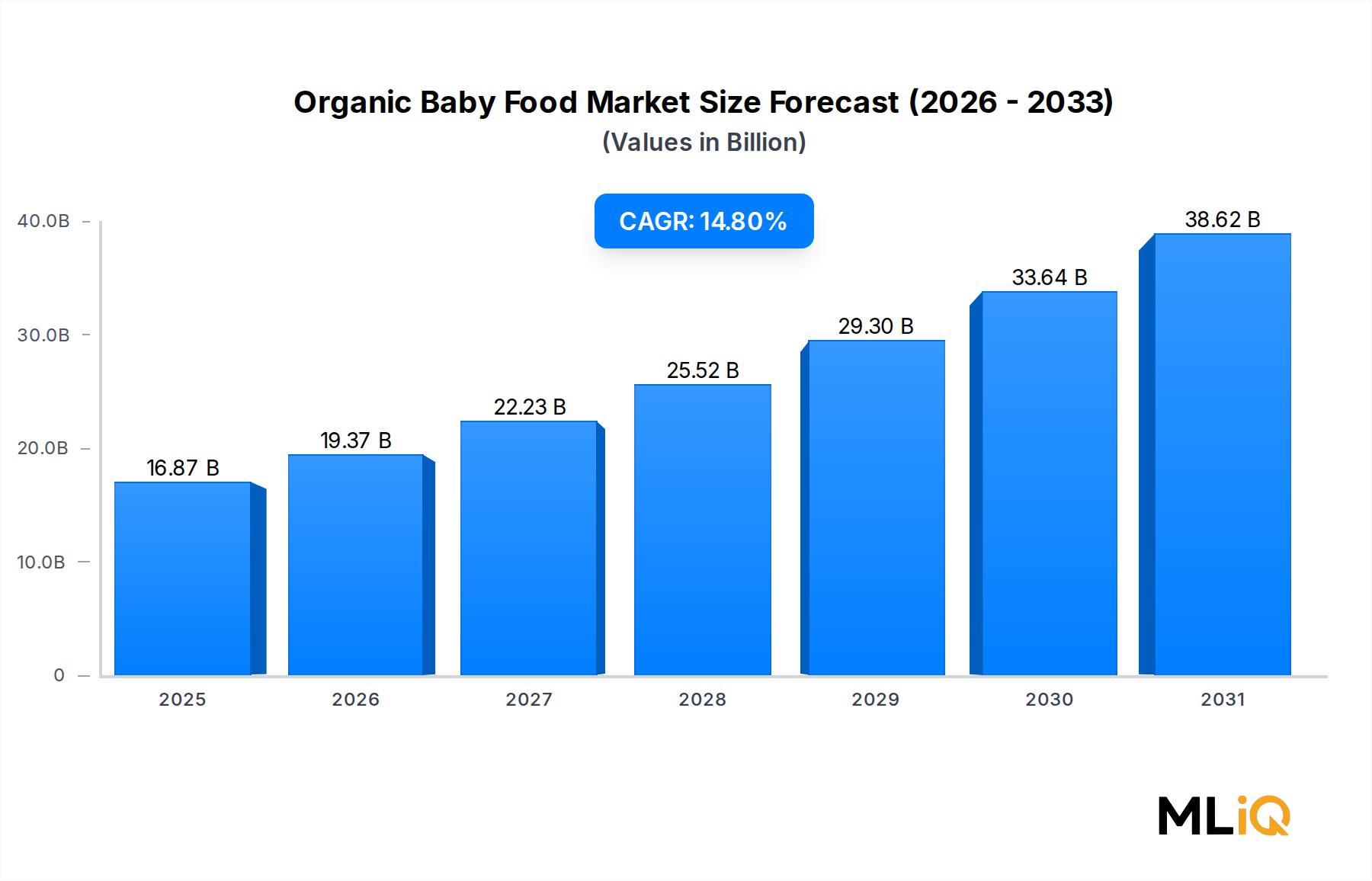

The global Organic Baby Food Market is poised for exceptional expansion over the forecast period 2025–2033, underpinned by a confluence of shifting parental priorities, rising disposable incomes, and an accelerating global pivot toward clean-label nutrition. The market was valued at $16.87 billion as of the base assessment period and is projected to advance at a compound annual growth rate (CAGR) of 14.8% through 2033, making it one of the fastest-growing segments within the broader food and beverages industry.

Core demand drivers include heightened awareness among millennial and Gen Z parents regarding the long-term health consequences of synthetic pesticides, artificial additives, and genetically modified organisms in early-stage nutrition. Pediatric research consistently linking early dietary exposure to developmental outcomes has translated directly into purchasing behavior, with organic certifications functioning as proxies for product safety and quality. This behavioral shift is reinforced by rapid urbanization, higher maternal workforce participation, and the growing availability of premium retail channels both online and offline.

Macro tailwinds further amplify structural demand. Governments across North America, the European Union, and the Asia Pacific region have introduced stricter regulations governing permissible residue levels in foods intended for infants and toddlers, which has created a regulatory incentive for manufacturers to reformulate using certified organic ingredients. Simultaneously, the proliferation of e-commerce platforms has dissolved geographic barriers, enabling premium organic baby food brands to penetrate markets in second- and third-tier cities across emerging economies.

From a product perspective, infant milk formula continues to be the highest-revenue sub-segment, while prepared and dried baby food formats are gaining rapid traction as parents seek convenient yet nutritious feeding solutions. The distribution landscape is also evolving, with digital channels capturing an increasing share of total retail volume, driven by subscription-based delivery models and algorithmically personalized product recommendations.

Looking forward, the market is expected to see intensified merger and acquisition activity as multinational food conglomerates seek to acquire agile, certification-rich startups. Innovation in fortification — particularly with prebiotics, DHA, and iron — will become a key battleground for differentiation. Private-label organic offerings from large retail chains represent a nascent but growing competitive threat to branded players. Overall, the Organic Baby Food Market's trajectory reflects a structural, rather than cyclical, elevation in consumer standards for infant nutrition, positioning it as a durable growth engine within the global food and beverages landscape through the end of the decade.

Among all product sub-segments within the Organic Baby Food Market, infant milk formula commands the single largest revenue share, a position driven by biological necessity, physician endorsement, and the comparatively high per-unit price point of certified organic formulations. While prepared baby food and dried baby food formats serve older infants and toddlers transitioning to solid foods, infant milk formula addresses the nutritional requirements of the 0–12-month age cohort — a stage during which no dietary substitution is feasible without medical risk, creating inelastic demand that insulates this sub-segment from broader economic fluctuations.

Organic infant milk formula commands a significant price premium over conventional counterparts, typically ranging between 30% and 60% above standard formula products depending on the market. This premium is justified in consumer perception through certification logos (USDA Organic, EU Organic, Australian Certified Organic), the exclusion of synthetic growth hormones in source dairy herds, and the absence of corn syrup solids and carrageenan — ingredients that have attracted increasing regulatory and media scrutiny. The willingness of higher-income demographic segments to absorb this premium underpins disproportionately high revenue contributions relative to volume share.

Key players operating most aggressively within this sub-segment include HiPP, which has maintained a decades-long reputation for biodynamic and certified organic dairy sourcing across its European supply chain, and Nestlé S.A., which has introduced organic formula lines under multiple regional brand identities to capture demand across both mature and emerging markets. Danone's Nutricia and Aptamil organic variants have also achieved considerable retail penetration across the European Union and Asia Pacific markets, leveraging an established cold chain infrastructure and long-standing relationships with pediatric healthcare systems.

Abbot Laboratories participates in the premium formula segment through its Similac Organic line, which has benefited from sustained brand trust among North American consumers and from co-marketing arrangements with hospital networks. The competitive intensity within infant milk formula is further amplified by the entry of digitally native brands such as Amara Organics, which have leveraged direct-to-consumer subscription models to reduce customer acquisition costs and secure recurring revenue streams.

From a share evolution standpoint, organic infant milk formula's dominance is consolidating rather than merely stable. As birth rates in high-income countries moderate, manufacturers are pursuing two parallel strategies: first, deepening penetration in existing markets through product premiumization (adding organic DHA, A2 protein variants, and probiotic strains); and second, expanding distribution into Asia Pacific markets — particularly China — where the 2008 melamine contamination scandal created a durable structural preference among Chinese parents for imported or internationally certified formula products.

Regulatory heterogeneity across jurisdictions remains a complicating factor. The European Union's stringent Delegated Regulation (EU) 2016/127 establishes compositional requirements for infant formula that effectively raise the bar for organic certification compliance, functioning as a de facto quality filter that benefits established players with robust regulatory affairs capabilities. In contrast, emerging markets maintain less prescriptive frameworks, creating both opportunity and risk for brands seeking rapid geographic expansion. Overall, the infant milk formula sub-segment is expected to retain its revenue leadership throughout the forecast period, with its share of total Organic Baby Food Market revenue projected to remain above 40% through 2033.

Several quantifiable forces are simultaneously accelerating and moderating growth trajectories within the Organic Baby Food Market.

On the demand side, rising health consciousness among millennial parents is the primary accelerant. Survey data from multiple consumer research firms indicate that more than 65% of millennial parents in North America and Western Europe actively consult product labels for organic certification before purchasing baby food, compared to fewer than 30% of Gen X parents in the same geographies a decade prior. This behavioral inflection has catalyzed new product development cycles and elevated shelf-space negotiations in favor of organic SKUs.

E-commerce channel expansion has served as a critical distribution driver. Online grocery penetration rates for baby food products increased sharply following 2020, with digital channels now accounting for an estimated 22–28% of total organic baby food sales in mature markets. Subscription-box models have proven particularly effective, generating higher average order values and repeat purchase rates than single-transaction retail formats.

Government subsidy programs and organic farming incentive schemes across the European Union — notably under the Common Agricultural Policy — have expanded the supply base of certified organic dairy and produce, partially relieving input cost pressures on manufacturers and enabling more competitive retail pricing without eroding margin structures.

However, substantive constraints moderate the growth curve. Supply chain fragility for certified organic ingredients remains a structural bottleneck. Organic certification timelines of 3 years for farmland conversion create inelastic short-term supply responses to demand spikes, contributing to periodic ingredient shortages and elevated commodity prices. The sourcing of organic dairy is particularly vulnerable to weather-driven pasture yield variability.

Additionally, affordability remains a barrier to mass-market penetration in lower-middle-income countries. With organic baby food commanding premiums of 30–60% above conventional alternatives, price sensitivity effectively restricts the addressable market in economies where per-capita household food expenditure remains constrained. Regulatory fragmentation across regions further increases compliance costs, creating market entry friction for smaller manufacturers seeking multi-regional distribution.

The competitive landscape of the Organic Baby Food Market is characterized by a blend of multinational food conglomerates, purpose-built organic specialists, and emerging direct-to-consumer challengers. The following profiles outline the strategic positioning of leading participants:

Amara Organics: A digitally native brand that pioneered the "just-add-breastmilk-or-formula" powder format, enabling premium ingredient profiles without the shelf-life compromises of conventional pouches. The company competes primarily through its direct-to-consumer e-commerce channel and a subscription loyalty program.

Baby Gourmet Foods Inc.: A Canadian organic baby food specialist known for its fruit and vegetable puree pouches, with distribution spanning North American retail chains. The company has built brand equity on transparent sourcing and non-GMO ingredient certification.

Plum Organics: A California-based brand operating under the Campbell Soup Company umbrella, offering an extensive portfolio of organic purees, snacks, and toddler meals. Its retail footprint spans major supermarket and hypermarket chains across North America.

North Castle Partners, LLC.: A private equity firm that has historically invested in health-and-wellness consumer brands, providing strategic capital and operational expertise to emerging organic baby food companies seeking scale-up resources.

Hero Group: A Swiss food conglomerate with a significant presence in the organic baby food segment through its Organix and Semper brands, distributed prominently across European retail channels with growing Asia Pacific visibility.

Nestlé S.A.: The world's largest food company by revenue, maintaining an extensive organic baby food and infant formula portfolio marketed under regional brand identities. Nestlé leverages its global cold chain infrastructure and regulatory expertise to compete across both premium and mid-tier price points.

Abbott Laboratories: A healthcare-focused multinational that competes in organic infant formula through its Similac Organic line, benefiting from co-marketing relationships with pediatric clinical networks and pharmacy distribution channels.

Danone: A French multinational with dedicated early-life nutrition divisions (Nutricia, Aptamil) that have incorporated organic product lines. Danone's research-backed positioning and clinical credibility confer differentiation advantages in physician-recommended purchase contexts.

The Hain Celestial Group: A diversified natural and organic food conglomerate with brands such as Earth's Best Organic, one of the longest-established organic baby food franchises in the United States. The group competes through broad retail distribution and a deep heritage in the organic food segment.

HiPP: A German family-owned manufacturer widely regarded as a global benchmark for organic and biodynamic baby food standards. HiPP's vertically integrated supply chain, spanning its own certified organic farms, confers both quality assurance and supply security advantages rarely matched by competitors.

January 2024: HiPP announced an expansion of its biodynamic milk sourcing program, adding 12 new certified partner farms across Bavaria and Austria to address growing European demand for ultra-premium infant formula, with production capacity slated to increase by 18% by Q3 2025.

March 2024: Danone received regulatory approval from China's National Medical Products Administration for three new organic infant formula SKUs under its Aptamil brand, enabling expanded distribution across mainland China's 600+ city tier-1 and tier-2 retail networks.

June 2024: Plum Organics launched a new line of fortified organic toddler snacks containing clinically validated prebiotic fiber levels, targeting the 12–36 month age cohort and responding directly to pediatric guidance emphasizing early gut microbiome development.

September 2024: Abbott Laboratories completed a reformulation of its Similac Organic product line, removing all palm olein oil from the ingredient matrix in response to parental advocacy group petitions and emerging clinical literature questioning its digestive tolerability.

November 2024: Amara Organics secured a Series B funding round of $22 million, led by a consortium of impact investors, to accelerate its direct-to-consumer platform expansion into the United Kingdom and Germany markets.

February 2025: The European Commission published updated maximum residue limits under Regulation (EC) No 396/2005, tightening pesticide thresholds in processed foods intended for infants by an average of 40%, effectively mandating reformulation across multiple conventional and near-organic product lines.

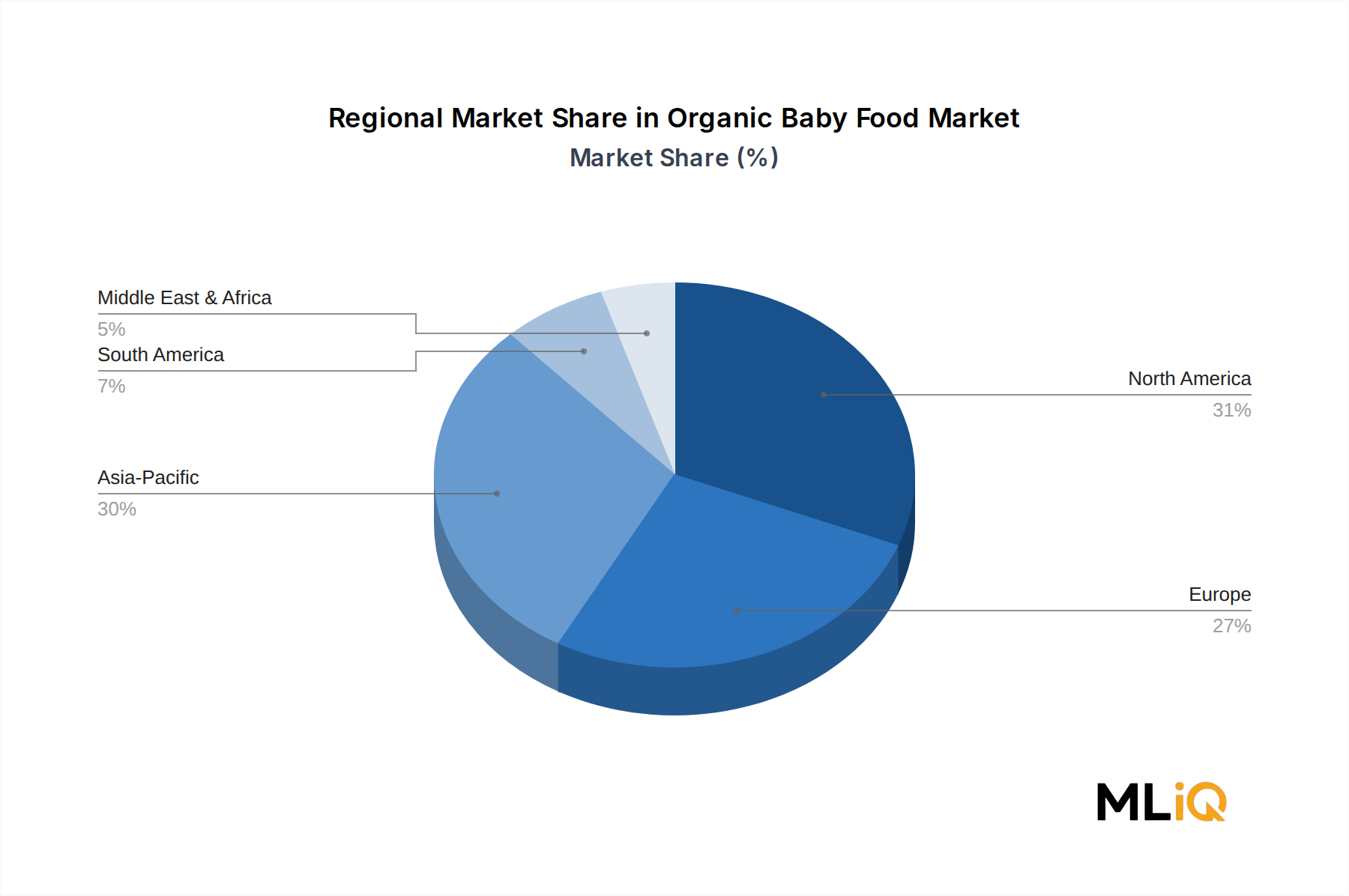

Geographic demand distribution across the Organic Baby Food Market reflects a complex interplay of income levels, cultural feeding practices, regulatory environments, and e-commerce infrastructure maturity.

North America remains the most mature and highest-revenue regional market, accounting for an estimated 34–37% of total global revenue. The United States drives the majority of this share, underpinned by USDA Organic certification's strong consumer recognition, a well-developed natural food retail channel (including Whole Foods Market and Target's premium grocery sections), and a robust e-commerce infrastructure. The North American market is projected to grow at a CAGR of approximately 12.5% through 2033, reflecting a moderating but still robust expansion pace consistent with market maturity.

Europe represents the second-largest regional market, with Germany, the United Kingdom, and France serving as the primary revenue centers. European consumers exhibit among the highest per-capita organic baby food expenditure globally, driven by established organic farming culture, strong regulatory frameworks (EU Organic Regulation), and high retailer own-label organic ranges. The European market is projected to grow at a CAGR of approximately 11.8% over the forecast period, with Nordic countries and the Benelux region showing above-average premium product adoption rates.

Asia Pacific is unambiguously the fastest-growing regional market, projected to expand at a CAGR of 18.2–19.5% through 2033. China is the primary growth engine, where import-oriented purchasing behavior — born from domestic food safety concerns — has elevated demand for certified international organic formula and puree products. India represents a high-potential secondary growth market, where rising urban middle-class incomes and increasing awareness of clean-label nutrition are driving early-stage market development. Japan and South Korea exhibit more mature organic baby food adoption curves, with premiumization and functional ingredient fortification serving as the primary competitive differentiators.

Latin America is an emerging growth frontier, with Brazil and Argentina leading regional demand. Infrastructure constraints in cold chain logistics and import certification complexity moderate the pace of expansion, but urbanization trends and growing e-commerce penetration are gradually addressing these barriers. The region is projected to grow at a CAGR of approximately 13.2%.

Middle East and Africa represent the smallest absolute revenue base but contain pockets of high-growth potential — particularly in GCC countries (Saudi Arabia, UAE), where premium consumer spending and a high proportion of expatriate populations with international dietary preferences create viable demand for imported organic baby food brands.

The supply chain architecture of the Organic Baby Food Market is structurally more complex and cost-intensive than that of conventional baby food manufacturing, owing to the certification requirements, shorter ingredient shelf lives, and geographic concentration of certified organic agricultural inputs.

Organic dairy — the foundational raw material for infant milk formula — is sourced predominantly from certified farms in Europe (Germany, Netherlands, Denmark) and the United States. Price volatility in organic dairy is driven by pasture yield variability, feed cost fluctuations (particularly organic soy and alfalfa), and herd health dynamics. Organic whole milk powder prices increased by approximately 23% between 2021 and 2023 due to drought-related pasture stress across key European sourcing regions, compressing margins for formula manufacturers during this period.

Organic fruit and vegetable purees — the core inputs for prepared baby food — are heavily dependent on certified orchards and farms in Spain, Italy, Chile, and the United States. Seasonal variability, pest management constraints inherent to organic cultivation, and land conversion timelines (a mandatory 3-year pesticide-free transition period before organic certification is granted) create chronic supply inelasticity. Manufacturers have increasingly responded by entering long-term offtake agreements with farming cooperatives, partially insulating themselves from spot market price swings.

Packaging inputs also represent a critical supply chain node. The Organic Food and Beverages Market broadly is shifting toward BPA-free, recyclable, and compostable packaging formats under regulatory and consumer pressure, increasing demand for specialty packaging substrates including bio-based flexible films and recycled-content rigid containers. These materials carry cost premiums of 15–40% above conventional equivalents and are sourced from a narrower supplier base, introducing concentration risk.

Logistics disruptions — most acutely experienced during **

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.8% from 2020-2034 |

| Segmentation |

|

Our rigorous research methodology combines multi-layered approaches with comprehensive quality assurance, ensuring precision, accuracy, and reliability in every market analysis.

Comprehensive validation mechanisms ensuring market intelligence accuracy, reliability, and adherence to international standards.

500+ data sources cross-validated

200+ industry specialists validation

NAICS, SIC, ISIC, TRBC standards

Continuous market tracking updates

Factors such as are projected to boost the Organic Baby Food Market market expansion.

Key companies in the market include Amara Organics, Baby Gourmet Foods Inc., Plum organics, North Castle Partners, LLC., Hero Group, Nestlé S.A., Abbott laboratories, Danone, The Hein celestial group, HiPP.

The market segments include Product, Distribution Channel.

The market size is estimated to be USD 16.87 billion as of 2022.

N/A

N/A

N/A

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3200, USD 4065, and USD 6809 respectively.

The market size is provided in terms of value, measured in billion and volume, measured in .

Yes, the market keyword associated with the report is "Organic Baby Food Market," which aids in identifying and referencing the specific market segment covered.

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

To stay informed about further developments, trends, and reports in the Organic Baby Food Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.